Accumulator

Enhancing Monthly Dollar Cost Averaging (DCA) for Long-Term Index Investors

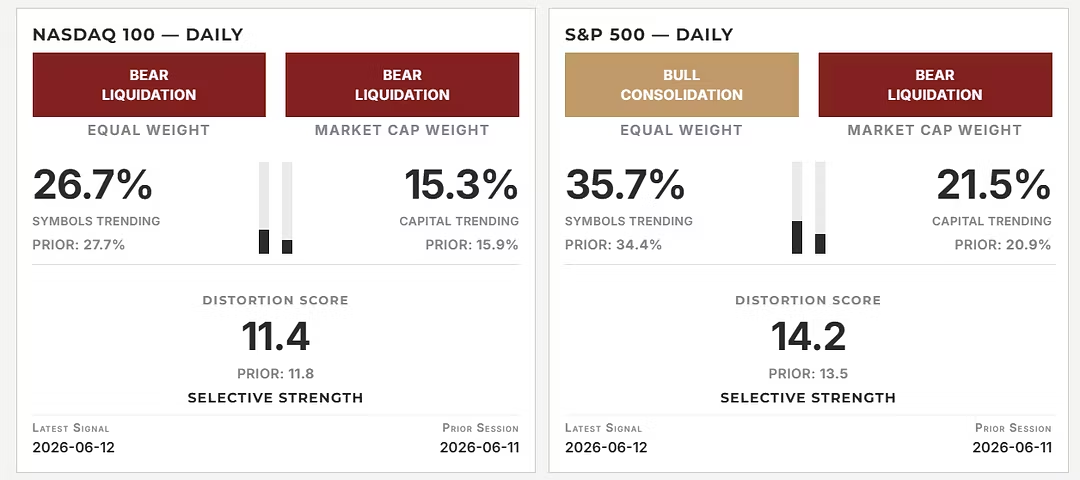

A mathematical optimization protocol engineered for disciplined capital compounders allocating monthly liquidity to the S&P 500 or Nasdaq-100. Rather than deploying capital on blind monthly Dollar Cost Averaging (DCA) calendar schedules into euphoric overextensions, the engine maps internal index participation to systematically size and time capital deployment.

Un-deployed capital is insulated within an interest-bearing short-duration Treasury vehicle inside your own brokerage account. When market breadth indicates rare structural discount windows or euphoric overextensions, the engine coordinates an asymmetric allocation protocol—shifting systematically between a 'Strike' posture during market washouts and a 'Throttle' posture during structural overextensions.

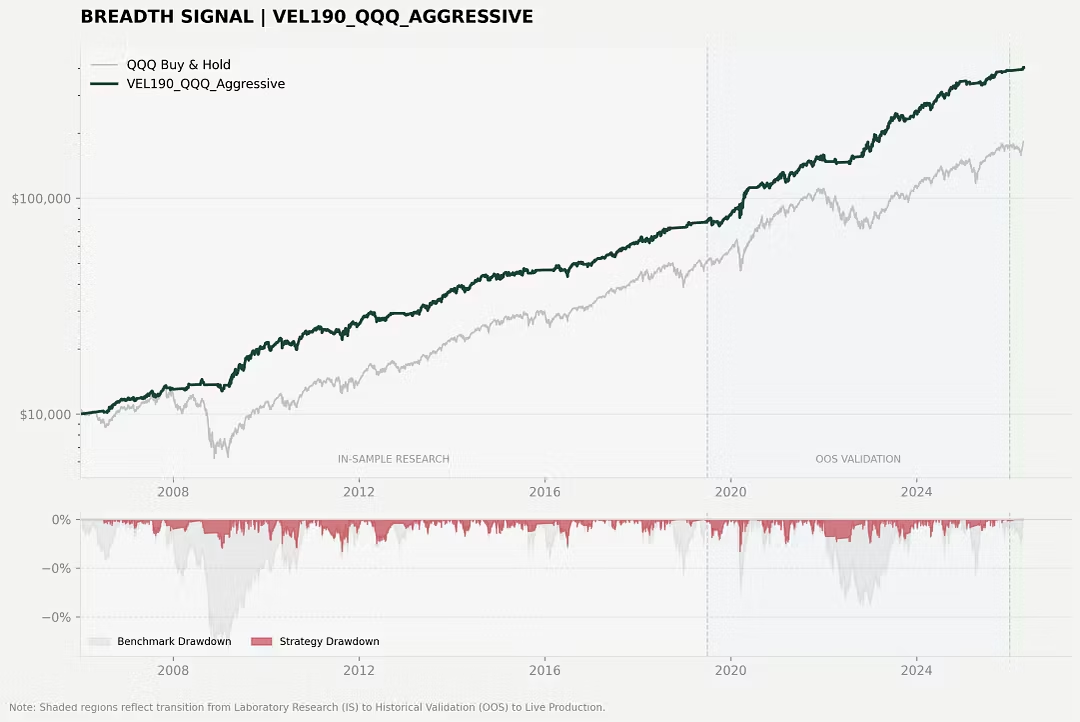

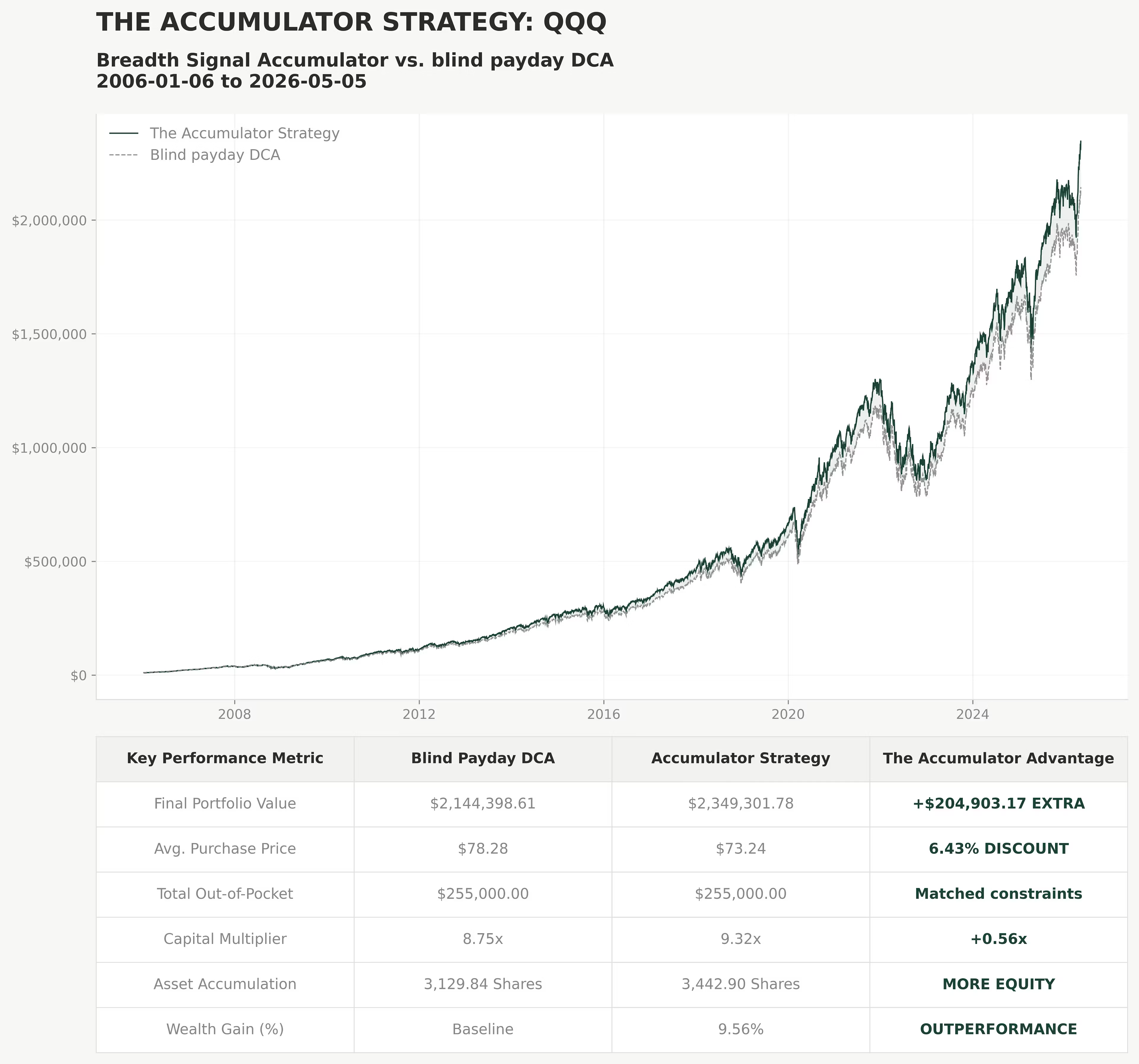

Historical audits spanning Jan 01, 2006, to May 06, 2026, demonstrate an audited 6.43% Strategic Purchase Discount on the Nasdaq-100, resulting in a +$204,903.17 final equity delta over static monthly buying on matching principal constraints.

Pure mathematics. Zero speculation.