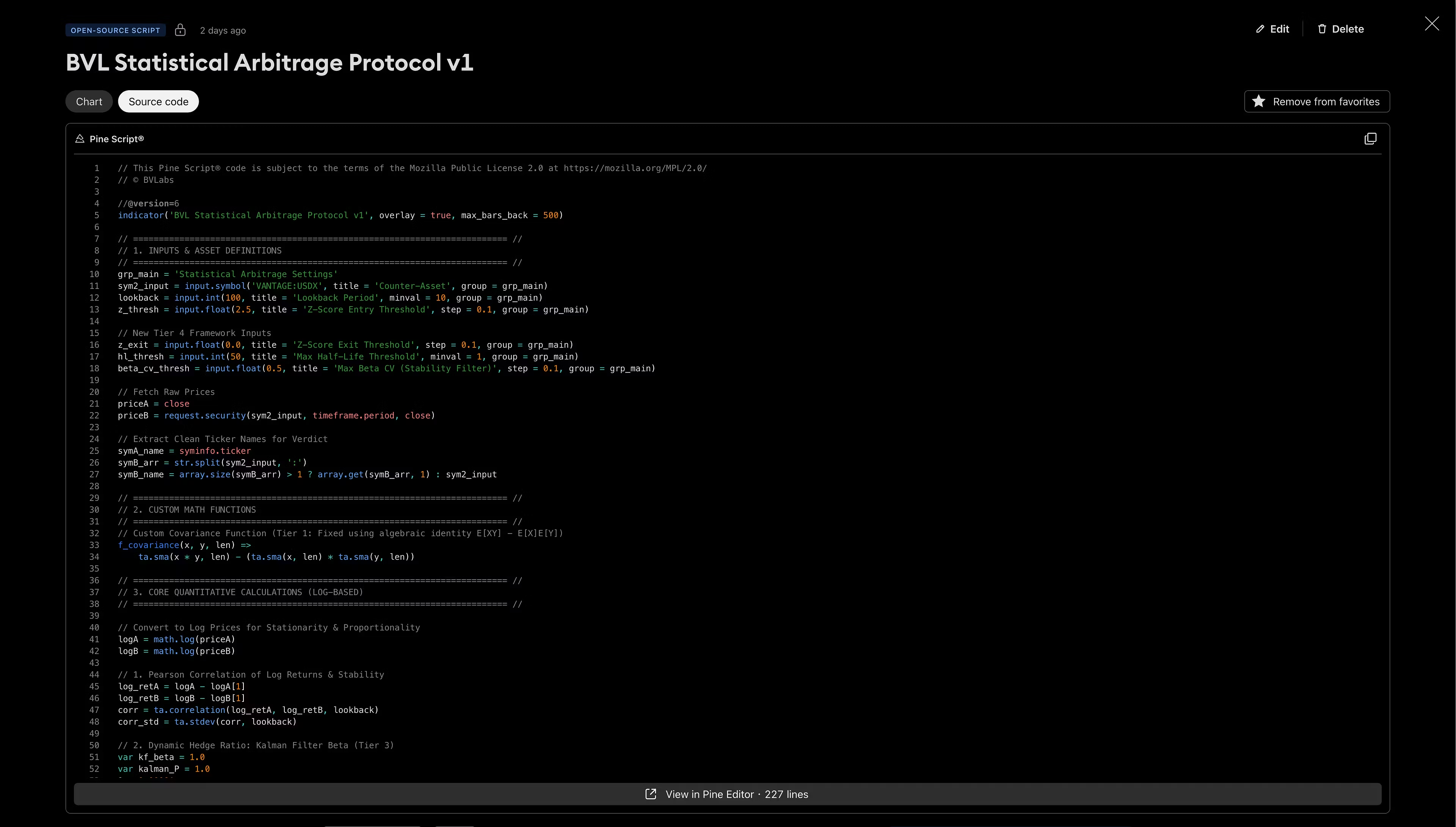

BVL Statistical Arbitrage Protocol

Turn market chaos into mathematical certainty

Stop relying on static ratios and lagging indicators. The BVL Statistical Arbitrage Protocol is a high-performance quant engine engineered to extract market-neutral alpha from pairs and baskets using advanced time-series analysis and adaptive mathematical models.

Elite Quantitative Architecture:

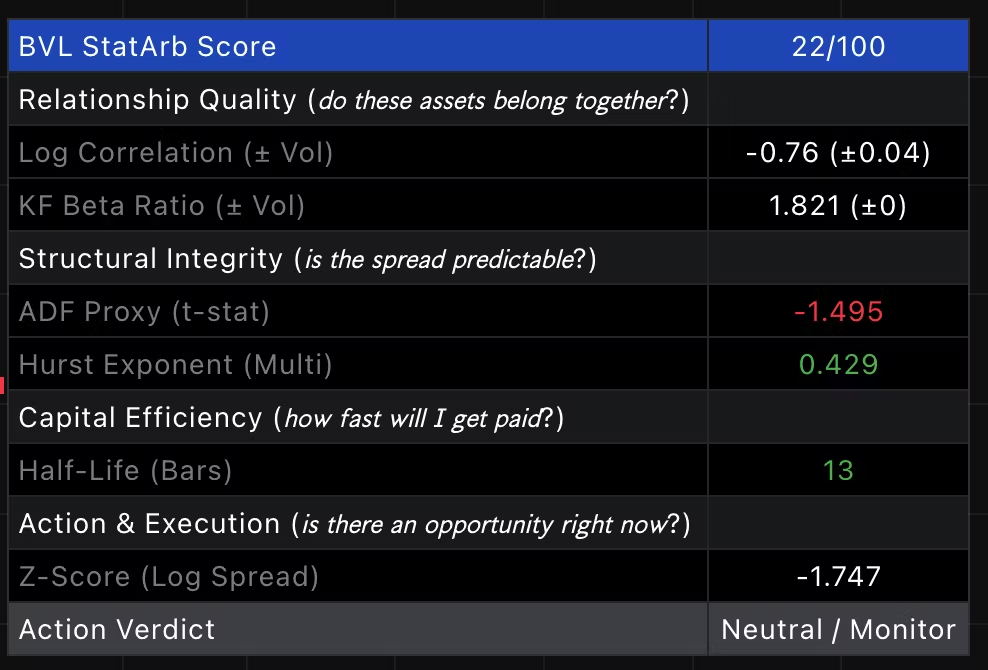

Dynamic Hedge Ratio (Kalman Filter): Replaces rigid, static beta with an adaptive state-space model that tracks time-varying relationships in real time, keeping your legs perfectly balanced.

Ornstein-Uhlenbeck (OU) Half-Life: Quantifies the exact speed of mean reversion, automatically calculating how long a divergence will take to decay so you can optimize holding periods.

Hurst & ADF Proxies: Built-in validation filters that instantly separate genuine, cointegrated stationary spreads (ADF) from random walks and structural regimes shifts (Hurst).

Multi-Factor Composite Scoring: Blends Z-score velocity, cointegration strength, and structural momentum into a single, cohesive statistical matrix.

Exact Action Verdicts: Eliminates execution hesitation by outputting definitive, machine-like triggers (Buy X / Sell Y / Regime Shift Alert) on your chart.

Trade with institutional precision. Let the math do the hunting.

TradingView 👇

https://www.tradingview.com/script/3lYGCYKr-BVL-Statistical-Arbitrage-Protocol-v1

- 1 month ago