BVL StatArb | BTCUSD - DXY

Trade the divergence. Capture the convergence.

A quantitative statistical arbitrage system built to exploit inefficiencies between BTCUSD and the U.S. Dollar Index (DXY).

The algorithm continuously tracks the inverse macro relationship between Bitcoin and USD liquidity conditions, identifying periods where price deviates from statistically expected behavior and targeting high-probability mean reversion or re-acceleration phases driven by risk-on/risk-off flows and dollar strength cycles.

✅ Fully systematic execution

✅ No discretionary trading

✅ Statistically validated methodology

✅ Real-time alerts & automation ready

✅ Built for institutional-style quantitative traders

Designed around Bitcoin’s sensitivity to global liquidity and USD strength regimes, this model translates macro divergence into structured, rules-based trading signals across volatility cycles.

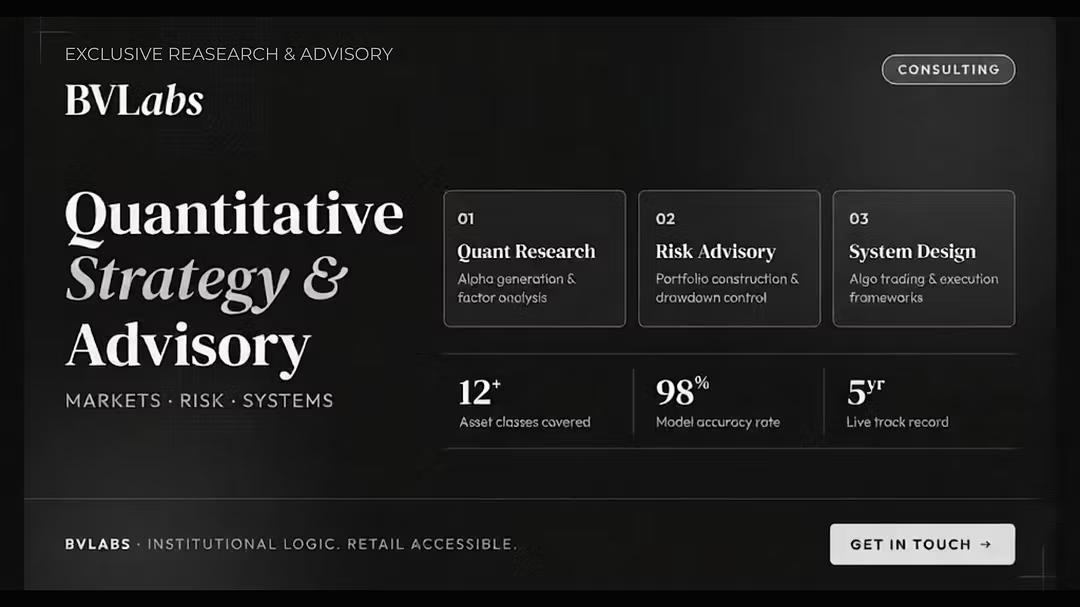

Institutional Edge. Built for Retail.

TradingView 👇

https://www.tradingview.com/script/AfGMJmlK-BVL-StatArb-BTCUSD-DXY

🤝 Earn 30% Recurring Commission: https://whop.com/bvlabs/affiliates

- 15 days ago

where I’m from, we say ‘hii imeenda’.. the accuracy and consistency is on another level🚀🚀

- 15 days ago

Joining BVLabs has probably turned out to be the best decision I ever made in my trading. BVLabs has been a different experience.

- 15 days ago

I've bounced around a ton of trading communities over the last couple of years, and most of them end up being unreliable longterm. BVLabs stood out because everything is backed by data. I book their consulting sessions from time to time and it has easily made the membership worthwhile for me.

- 15 days ago

The XAUUSD-DXY Node is an absolute cheat code for trading gold!