Stripe Connect works - until it doesn't. This guide breaks down the top alternatives for platforms and marketplaces: comparing fees, payout capabilities, and global reach.

Key takeaways

- Platforms should avoid single-provider dependency because compliance events or policy changes can freeze funds at critical moments.

- Multi-provider payment orchestration with automatic retry can recover declined transactions and lift revenue by up to 6%.

- Stripe Connect's layered fee structure and payout network gaps become increasingly costly as platforms scale internationally.

Stripe Connect is the default starting point for most platforms and marketplaces. The documentation is thorough, the developer experience is polished, and the ecosystem is vast.

But default choices have a way of becoming expensive habits. As platforms scale, expand internationally, or build more complex payment flows, the gaps in Stripe Connect - pricing at volume, payout flexibility, geographic coverage, and support - start to matter.

This guide maps out where Stripe Connect works well, where it doesn't, and which alternatives are worth considering: full replacements, payout specialists, and merchant of record platforms.

What Stripe Connect does well

Built on top of Stripe's payments infrastructure, Stripe Connect gives platforms the core building blocks: seller and sub-merchant onboarding, fund routing, and payouts to connected accounts. It supports different payment flow models depending on how much control a platform wants over money movement.

The appeal is the depth of the offering. Stripe Connect offers progressive onboarding that gets sub-merchants transacting quickly, global reach across 46+ countries, automatic currency conversion, and an extensive library of payment and payout methods. Platforms also get pricing tools and margin reporting to understand and monetize their payment flows, plus built-in tax reporting to reduce compliance overhead.

The developer experience is polished, and a large ecosystem of integrations mean most platforms can get up and running quickly without a dedicated payments team.

Why Stripe Connect isn't always the answer

Stripe Connect is a strong default, but default choices don't always hold up under pressure.

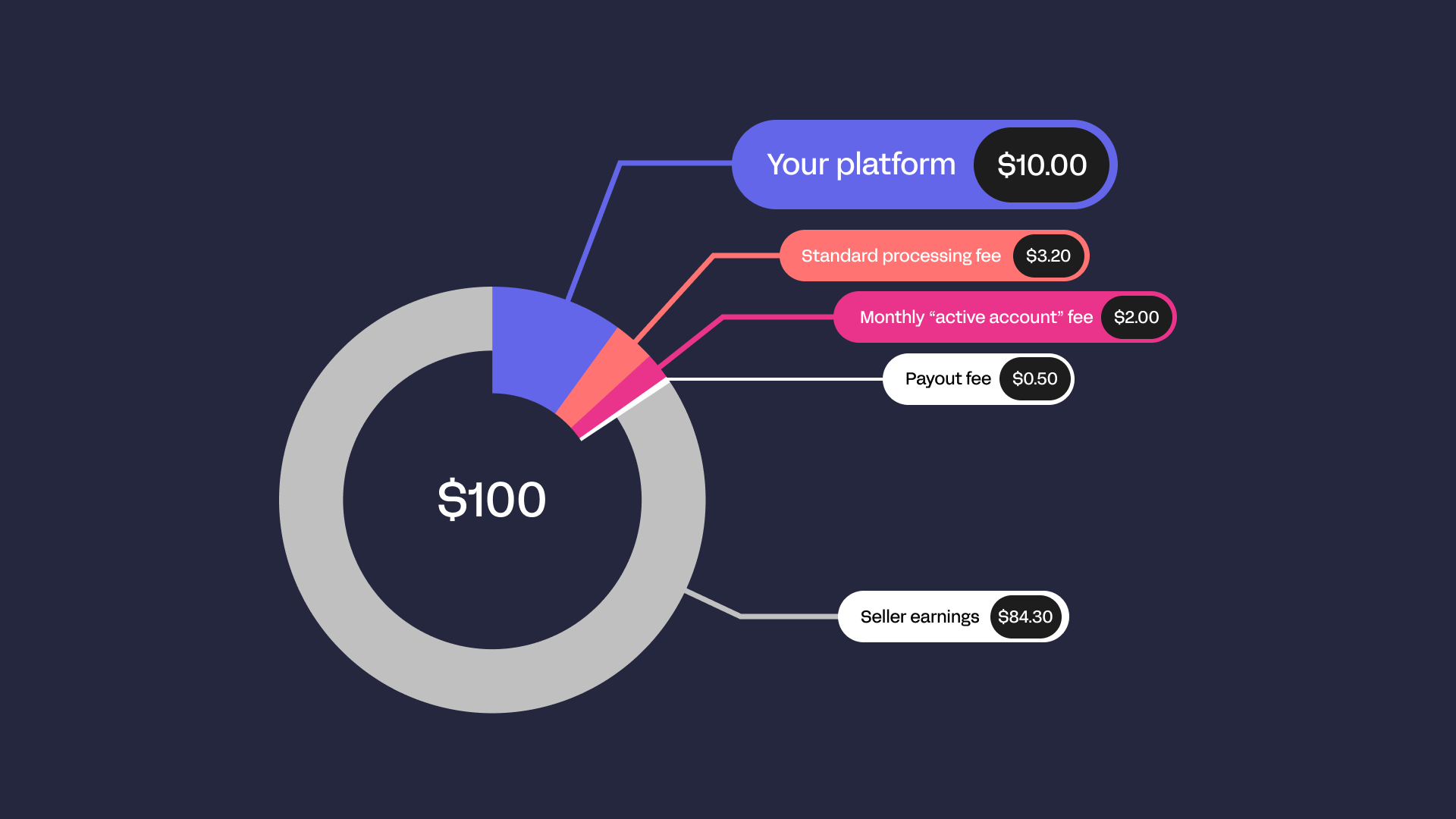

The first issue is fee complexity. Stripe Connect layers multiple charges on top of one another: processing fees, Connect account fees, instant payout fees, FX conversion fees, and dispute counter fees. In the early stages, this is manageable. But as transaction volume grows, the gap between what you expect to pay and what you actually pay tends to widen.

The second is geographic coverage. If your platform pays out to creators, sellers, or service providers in high-growth markets, you likely already know that Stripe's payout network has gaps - gaps that tend to show up in exactly the markets you're trying to expand into, forcing manual exception management that defeats the operational value of managed payments infrastructure.

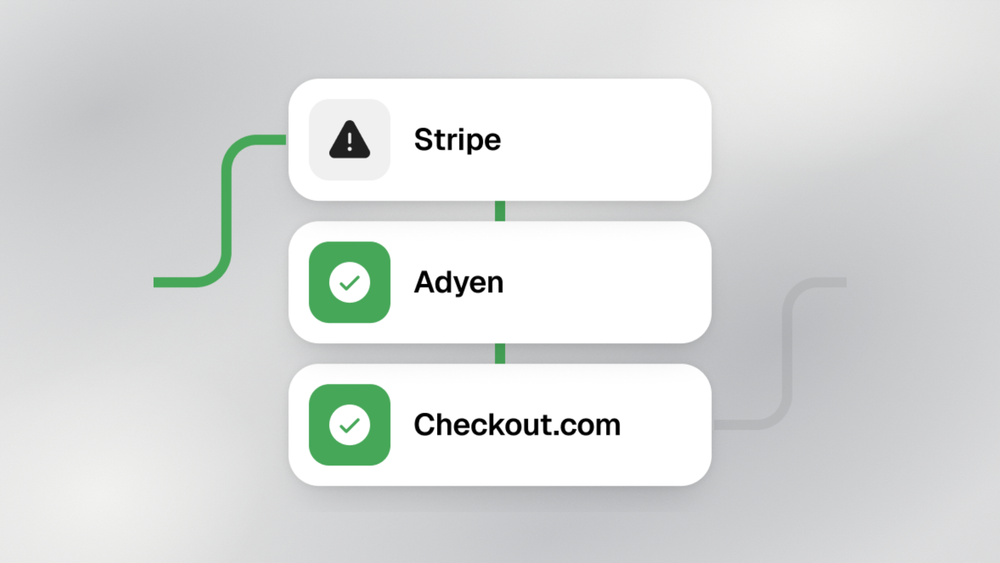

Then, there's vendor dependence. Running your entire payment stack through a single provider creates a concentration risk that's easy to underestimate until something goes wrong.

The Flipcause case is a great example. When the nonprofit fundraising platform filed for Chapter 11 in December 2025, Stripe - which had frozen approximately $2.2 million in funds following a California Attorney General enforcement action - became a central obstacle in creditors' ability to access those funds. Yes, Stripe's position was legally defensible, but the case shows that when one provider controls both processing and fund access, a compliance event, risk review, or platform-level dispute can lock funds at precisely the moment a business needs them most.

I asked Maddie Cohen, Head of Trust at Whop, about the true risk of single-PSP dependency during acquisition or policy change periods. Here's what she had to say:

"Different processors are beholden to different rules, and maybe that's prohibited or restricted merchants or maybe that's other policy or other processes. Whenever an individual PSP or payment or payout provider shifts their policies as a result of being acquired or anything else, you are at the mercy of of any of those changes."

For entreprise-level platforms, the question isn't whether Stripe Connect works, because it usually does. The question is whether the pricing, geographic coverage, and single-provider dependency are the right trade-offs for where the business is going.

The top Stripe Connect alternatives

The alternatives in this guide address specific gaps: cost at volume, global payee coverage, compliance complexity, or the need for multi-provider resilience. Not every option serves both platforms and marketplaces, each entry notes which use case it's built for.

Full Stripe Connect replacements

These are full-stack platforms with end-to-end pay-ins, payouts, and compliance under a single integration.

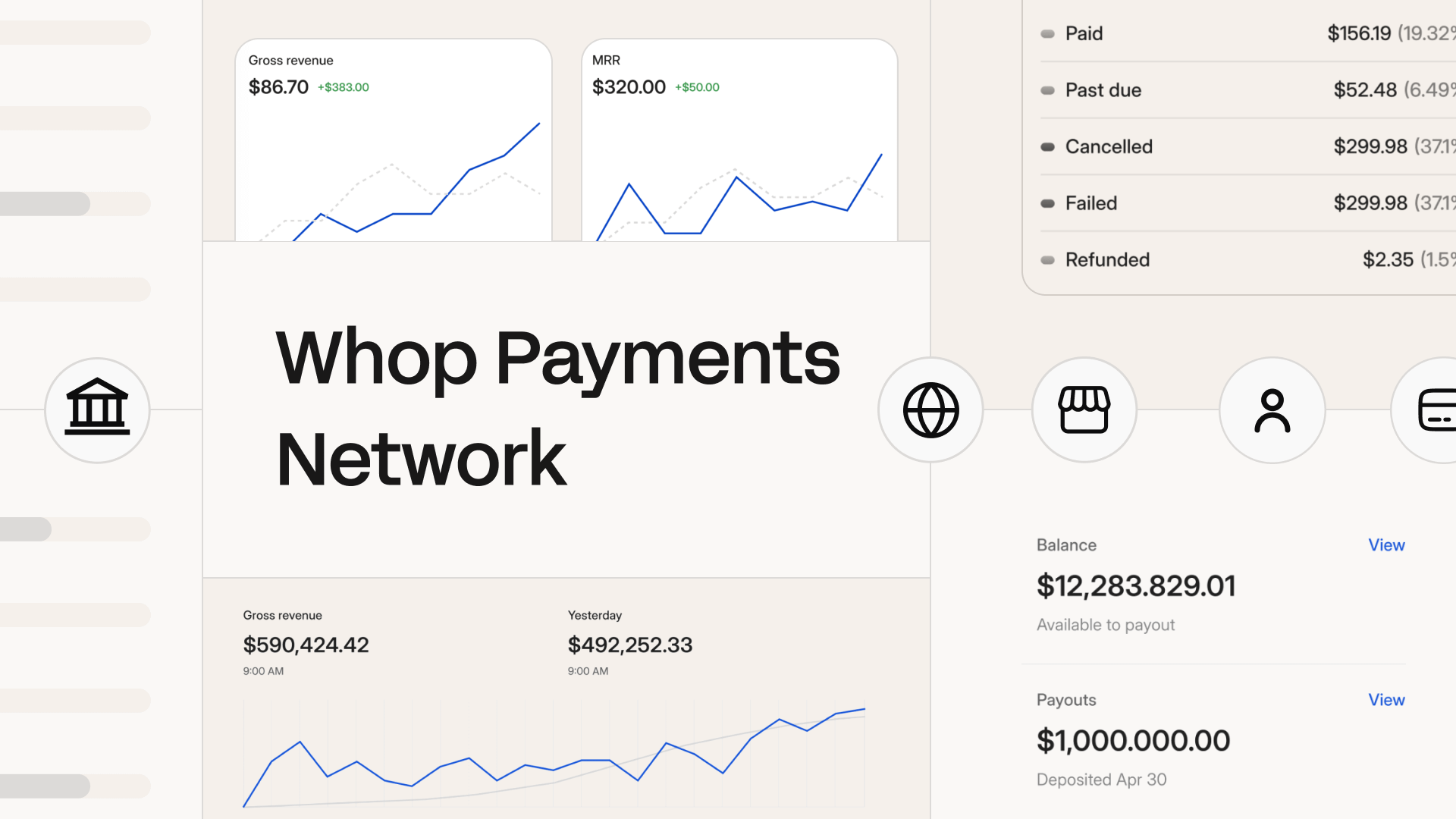

Whop Payments Network

Best for: platforms and marketplaces

If you're looking for a Stripe Connect alternative that solves the vendor dependence problem at its root, Whop Payments Network is worth your attention.

Where Stripe routes everything through a single processor, Whop Payments Network runs multi-provider orchestration with automatic retry on decline - meaning if one processor declines a transaction, it's automatically rerouted through another. Whop cites a revenue lift of up to 6% from this alone.

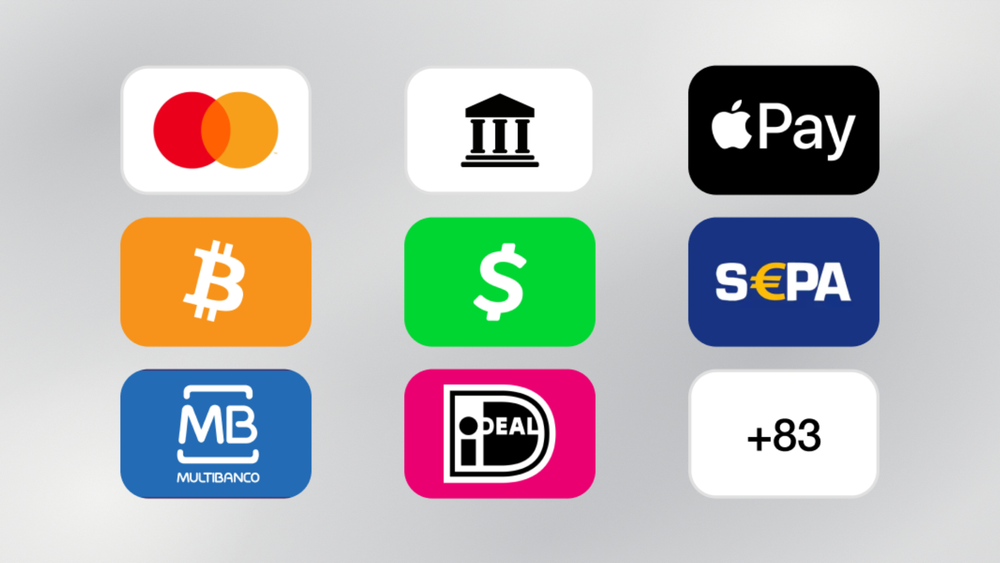

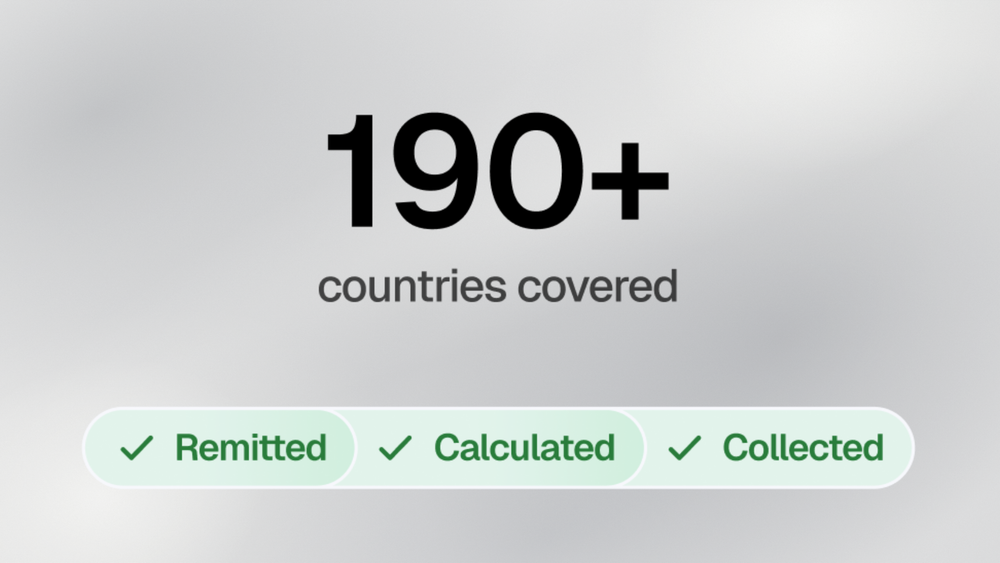

The infrastructure covers the full stack: pay-ins, payouts, embedded payments and checkout, ML-based fraud protection, automated billing and retry, and tax calculation and remittance: all under one integration. You get 100+ payment methods including iDEAL, Bancontact, and SEPA; 135+ currencies; 10 BNPL providers including Klarna, Afterpay, and Splitit; and coverage across 195 countries and territories.

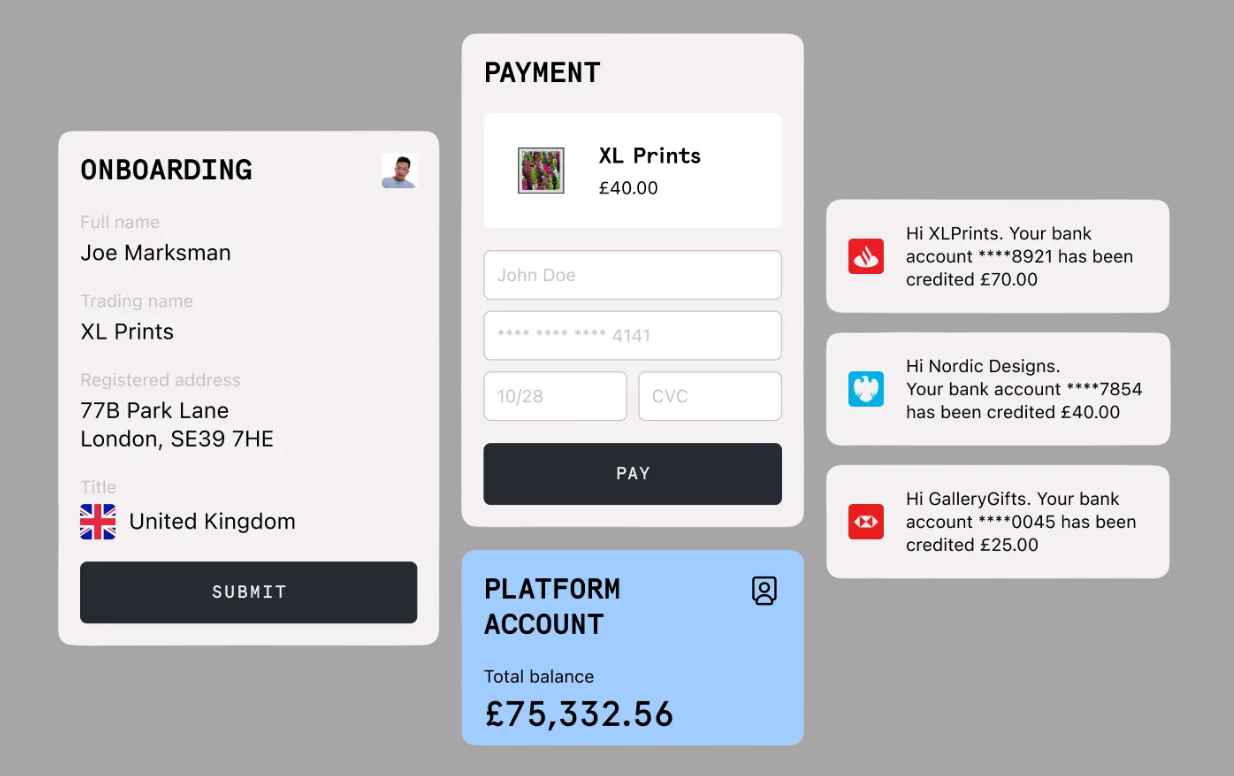

For platforms specifically, the connected accounts model lets you enroll sub-merchants with hosted KYC onboarding, collect payments via direct charges or post-capture transfers, and manage payouts per connected account. Payout options are broad: next-day ACH, Instant RTP, crypto, Venmo, bank wire, and international local bank transfers.

Pricing is transparent. Cards are 2.7% + $0.30 domestic, +1.5% international, +1% for currency conversion. ACH is 1.5% capped at $5. Optional modules - orchestration, automated billing, tax remittance, affiliate processing - carry additional fees, all published on the pricing page. Enterprise pricing is available on request.

Support is 24/7 across phone, chat, and email, with 99.999% uptime. If something goes wrong, you're not waiting days for a ticket response.

Whop Payments Network is used by 27,000+ businesses across coaching, SaaS, gig economy platforms, marketplaces, telehealth, events, and class action settlements.

"Whop has been super great in helping us automate all payouts on our referral platform for micro1. The integration was seamless and the team is always available to help with anything that pops up." — Ali Ansari, Founder of Micro1

Adyen for Platforms

Best for: platforms

If you need deep acquiring infrastructure, Adyen for Platforms is a great option.

Used by eBay, Oracle, Wix, and Lightspeed, it gives platforms everything needed to onboard seller and service providers, process payments online, in-person, through mobile channels, and manage fund flows and payouts - all under one integration.

Seller onboarding supports 33+ countries in 23 languages, with real-time identity verification and KYC, AML, MATCH list, and PCI/PSD2 compliance built in. Pricing uses an interchange++ model: no monthly fees, but rates are enterprise-negotiated, and there are high-volume minimums that make it unsuitable for earlier-stage platforms.

The trade-off is access. Adyen for Platforms is not self-serve - onboarding requires direct engagement with their sales team, and the level of integration complexity assumes that you have a dedicated payments engineering resource.

For platforms that qualify and have the team to support it, it's a good option. For those that don't, the barrier to entry is difficult to overcome.

Pros

- Best-in-class acquiring infrastructure - direct relationships with card networks deliver some of the highest authorization rates available

- Interchange++ pricing is cost-efficient at high volume compared to flat-rate models

- Full compliance stack managed by Adyen: KYC, AML, MATCH, PCI, PSD2

- Omnichannel - online, in-person, and mobile under one integration

- Trusted by some of the world's largest marketplaces, so the reliability track record is well-established

Cons

- Not self-serve - getting started requires a sales conversation and enterprise contracting

- High-volume minimums make it inaccessible for early or mid-stage platforms

- Integration complexity assumes a dedicated payments engineering team

- Limited geographic availability for Adyen for Platforms specifically: 33+ countries currently, with notable gaps in Latin America, most of Africa, and parts of APAC

- Pricing is opaque until you're in a sales process - difficult to model costs before committing

- Less suited to platforms whose primary challenge is payout diversity rather than payment acceptance

Checkout.com (Integrated Platforms)

Best for: platforms and marketplaces

Checkout.com's Integrated Platforms product is built for marketplaces and payment facilitators that need precise control over how money moves through their platform.

The standout feature is how it handles split payments: rather than splitting funds only at the point of capture (as many providers do), Checkout.com lets you configure splits at any stage of the transaction - authorization, capture, or even refund - and apply fixed, variable, or compound commission models per seller.

Sub-entity onboarding is automated with built-in KYC/KYB, and sellers get real-time 24/7 payouts directly to their bank accounts. Local acquiring across 45+ countries and 150+ processing currencies gives it strong coverage in Europe, MENA, and APAC.

Pricing follows an interchange++ model, negotiated at the enterprise level. Like Adyen, there's no self-serve path in.

Pros

- Granular split payment configuration than most alternatives - configurable at every stage of the transaction lifecycle

- Strong direct acquiring footprint in Europe, MENA, and APAC

- Automated KYC/KYB reduces onboarding friction for sub-entities at scale

- Real-time 24/7 payouts to seller bank accounts, not batched or delayed

- PCI-DSS Level 1 Vault for secure credential storage

Cons

- Less established in the US - not the right choice if North America is your primary market

- Enterprise-only, sales-led onboarding, no self-serve access

- Pricing requires a sales process to model accurately

- Less brand recognition among sub-merchants than Stripe, which can affect seller trust during onboarding

Mollie (Connect for Platforms)

Best for: platforms (split payments require their separate Marketplaces product)

For European platforms, Mollie Connect is one of the most accessible full-stack Stripe Connect alternatives available. Using an OAuth-based model, it lets you process payments on behalf of connected customer accounts, charge application fees per transaction, and handle balance transfers between organisations within your platform - all under one integration with hosted KYC onboarding for new customers.

The payment method coverage is Mollie's strongest differentiator over Stripe Connect. With 35+ global and local payment methods - including iDEAL, Bancontact, Klarna, Cartes Bancaires, Przelewy24, Swish, Apple Pay, Google Pay, and PayPal - Mollie covers the European local payment landscape thoroughly.

Clients using Connect for Platforms include Mazda, Q-Park, Otrium, and DPG Media. Mirakl connector integration is available for platforms using Mirakl's marketplace management infrastructure. Pricing is pay-per-transaction with no setup fees.

One important distinction: split payments - where funds are routed between multiple sellers in a single transaction - are available in Mollie's separate Connect for Marketplaces product, not Connect for Platforms. If multi-party fund splits are core to your model, you'll need to evaluate which Mollie product applies to your use case.

Pros

- Excellent European local payment method coverage

- Low-code integration

- Hosted, co-branded seller onboarding with fully managed KYC

- Pending GoCardless integration will add bank debit to the stack

- Pay-per-transaction pricing, no setup fees

Cons

- Europe-only - not suitable for platforms with a US-primary or emerging-market seller base

- GoCardless acquisition introduces near-term roadmap uncertainty: product priorities may shift during integration

- Chargeback liability sits with the marketplace platform, not the connected seller

Rainforest

Best for: platforms

Rainforest is the most direct answer to a specific problem: you're a vertical SaaS platform, you're currently processing payments through Stripe Connect, the economics don't work at your volume, and you don't want to spend months building a PayFac from scratch.

Unlike most PayFac-as-a-Service providers, which started as merchant acquirers and retrofitted platform features, Rainforest was built from the ground up exclusively for vertical SaaS.

This difference shows up in underwriting: rather than applying a generic risk model to your merchants, Rainforest builds a vertical-specific model per platform - which means higher merchant approval rates in industries like healthcare, logistics, and professional services that generic providers routinely flag as higher risk.

The compliance and risk stack - merchant onboarding and KYC, fraud monitoring, PCI compliance, chargeback management - is fully managed by Rainforest. Your team carries none of it. Integration uses pre-built white-labelled low-code components with a full sandbox and real-time API logs. Most platforms are processing within days.

Pricing uses a buy-rate interchange++ model with no monthly fees, no minimums, and no revenue split. You set your own sell price and keep the margin.

Pros

- Purpose-built for vertical SaaS, not retrofitted from a merchant-facing product

- Vertical-specific underwriting per platform improves merchant approval rates in underserved industries (healthcare, logistics, professional services)

- Full compliance and risk stack managed by Rainforest - KYC, fraud monitoring, PCI, chargebacks

- Transparent buy-rate interchange++ pricing — no monthly fees, no minimums, no revenue split

Cons

- Best suited to vertical SaaS platforms, not two-sided marketplaces - no split payments or multi-party fund routing

- US-focused: Canada expansion underway but not yet complete

Payout specialists

These payout tools handle the disbursement side of your payments stack. They don't process inbound payments from buyers - they sit downstream of your PSP and specialize in getting money out to sellers, creators, contractors, and service providers.

If your primary pain point with Stripe Connect is the payout side - coverage, cost, compliance, or volume - this is where to look.

Payoneer

Best for: platforms and marketplaces

If your platform pays out to a large network of freelancers, creators, or marketplace sellers - particularly outside the US and Europe - Payoneer has infrastructure that few others can match. Direct integrations with leading platforms including Airbnb, Upwork, and Fiverr mean many of your payees likely already have a Payoneer account.

Payoneer supports payouts to 190+ countries in 70 currencies, with receiving accounts in USD, EUR, GBP, and other major currencies that function like local bank accounts. For platforms, mass payout tools and a REST API allow programmatic disbursements at scale.

The 2025 fee changes are the most important thing to model before committing. Payoneer-to-Payoneer transfers under $400 now carry a flat $4 fee; transfers above $400 carry 1%. Combined with currency conversion markups of 0.5–3.5% depending on the method, the total cost of ownership has increased for platforms whose payees hold Payoneer accounts.

Pros

- 190+ countries, 70 currencies - strong emerging market coverage

- Payoneer prepaid Mastercard gives payees in underbanked markets immediate access to funds

- Established, regulated financial institution with strong brand recognition among freelancers and international sellers

- API available for programmatic mass payouts; batch upload for non-technical teams

Cons

- 2025 fee increases have materially raised the total cost of ownership, and previously free P2P transfers now carry a 1% fee

- Currency conversion markup of 0.5–3.5% is not the most competitive in the market

- Customer support is frequently cited as slow and difficult to escalate

- UI feels dated compared to newer alternatives

- Not developer-first: less suited to platforms that want to embed payouts natively into their product experience

PayPal / Hyperwallet (Enterprise Payouts)

Best for: platforms and marketplaces

PayPal acquired Hyperwallet in 2018 specifically to serve marketplace and platform payout needs, and the combined product - now branded as PayPal Enterprise Payouts - is one of the broadest-reach payout solutions available.

The most important aspect here is scale: access to PayPal's 400M+ active consumer accounts and 99M Venmo users means that for platforms whose payees already hold PayPal wallets, disbursement is near-instant and frictionless.

The infrastructure covers payouts in 50+ currencies across 200+ markets via multiple transfer methods - bank deposit, prepaid card, PayPal wallet, Venmo, check, and more. Batch CSV upload, with a REST API for programmatic workflows. A hosted Pay Portal and embedded finance components mean you can offer a payee-facing experience without building one from scratch.

However, the trade-offs are well-documented. Fee structure is not clear - pricing is volume-negotiated and varies by method, market, and payee type, making it difficult to model costs without going through a sales process. And, user reviews flag a non-intuitive payee onboarding experience, a heavy verification process, and slow enterprise support.

Pros

- 400M+ active PayPal accounts and 99M Venmo users: instant payouts to payees already in the network

- 200+ markets, 50+ currencies

- Batch CSV and REST API available

- Backed by PayPal's regulatory infrastructure and compliance in major markets

Cons

- No clear pricing - no published rate card, all pricing is negotiated

- Payee onboarding and verification process is frequently cited as cumbersome and slow

- Enterprise support response times are a recurring complaint at scale

- PayPal brand on disbursements may feel misaligned for platforms with a distinct brand identity

- Less developer-friendly than API-first alternatives like Trolley or Routable

Trolley

Best for: platforms and marketplaces

Trolley is purpose-built for mass disbursements to large, global payee networks. Where Stripe Connect bundles payouts into its broader platform infrastructure, Trolley treats disbursements as the core product; and the feature depth reflects that.

The platform covers payouts to 210+ countries and territories in 135+ currencies via local and global bank transfers, PayPal, Venmo, and digital wallets. Payee onboarding is white-labelled and self-service, with embedded KYC, bank account validation, and communication tools that platforms can surface directly within their product.

Tax compliance is comprehensive: W-9, W-8, 1099, 1042-S, and DAC7 (EU digital platform reporting, effective 2023) are all automated. Recipient-level risk scoring and watchlist screening identify and block bad actors across the network.

Pros

- Purpose-built for mass disbursements: not a retrofit from a broader payments product

- DAC7 compliance automation

- White-label payee onboarding portal embeds natively into platform product

- 210+ countries and territories, 135+ currencies with broad local rail coverage

- API-first with REST API, JS widget, webhooks, and web dashboard

- No forced inbound payment flow - sits cleanly downstream of any PSP

Cons

- Disbursement-only - does not process inbound payments

- Smaller brand recognition than Tipalti or PayPal/Hyperwallet among enterprise procurement teams

- PayPal integration has known limitations for non-US PayPal accounts

Routable

Best for: platforms

Routable is not purely a payout platform like Trolley, and it's not purely an enterprise AP solution like Tipalti. It sits between the two: an API-first payment infrastructure tool that handles both inbound invoice processing and outbound disbursements, making it well-suited if your platform manages both AP and seller payouts under one system.

The payout infrastructure is strong, with ACH across four speed tiers, international transfers to 220+ countries and territories in 140+ currencies, and automated W-9/W-8 tax form collection. The API is clean and developer-friendly.

Integrations cover QuickBooks, Xero, NetSuite, and Sage Intacct, and the platform includes AI-powered OCR for invoice capture, approval workflows, and reconciliation tooling.

Pros

- API-first with fast integration - suits developer-led platform teams

- Four ACH speed tiers give genuine payout flexibility

- 220+ countries and territories, 140+ currencies for international disbursements

- Handles both AP automation and payout disbursements: useful for platforms managing both

- Strong ERP integrations: QuickBooks, Xero, NetSuite, Sage Intacct

Cons

- Monthly subscription plus per-transaction fees - pricing requires careful modelling at volume

- AP tooling adds complexity for platforms that only need the payout side

Tipalti

Best for: platforms and marketplaces

Tipalti is the enterprise standard for global payables automation. Where Trolley and Routable are developer-first and relatively self-serve, Tipalti is finance-team-led - built for organizations where AP, compliance, and disbursements are managed by a dedicated finance function rather than embedded in the product.

The scope covers 196 countries and territories, 120 currencies, and 50+ payment methods including ACH, wire, PayPal, prepaid card, and check. Tax compliance automation covers W-8/W-9 collection, TIN matching, 1099 and 1042-S filing, VAT, and a KPMG-approved tax engine. Self-billing, multi-entity support, FX hedging, SOC-compliant audit trails, and a supplier self-service portal are all included in higher-tier plans.

For platforms and marketplaces processing high volumes of payments to complex global payee networks - affiliate networks, creator platforms, gig economy operators, advertising marketplaces - Tipalti automates workflows that would otherwise require significant headcount. Clients include Twitch, Roblox, GoPro, and GoDaddy.

But the limitations can be a deal-breaker. Implementation is a big process: expect weeks, not days, and likely a dedicated implementation resource.

Pros

- Enterprise-grade coverage: 196 countries and territories, 120 currencies, 50 payment methods

- SOC-compliant audit trails, important for public companies or those approaching IPO

- Multi-entity and multi-currency support built in

- Supplier self-service portal reduces operational burden

- Trusted by major platforms including Twitch, Roblox, and GoPro

Cons

- Finance-team-led, not developer-first - integration complexity is high

- Significant implementation investment required: weeks to months depending on scope

- Can feel heavyweight for platforms that only need the payout side without full AP automation

- Less suited to platforms that want to embed payouts natively into a product experience

GoCardless

Best for: platforms with a recurring payment collection problem, not a payout problem

Now, a note about GoCardless before diving in: it is not a payout platform in the same sense as the others in this tier. It doesn't disburse funds to sellers or service providers. What it does is give platforms a way to collect recurring payments from customers via bank debit, and open banking across 30+ countries - at a significantly lower cost than card processing.

If your platform's specific pain point with Stripe Connect is the cost of collecting recurring payments from buyers - particularly in Europe or Australia where bank debit adoption is high - GoCardless is worth serious consideration. It is trusted by over 100,000 businesses and has a 97.3% first-attempt collection rate.

The most significant development in 2025 is GoCardless's role in building the UK's commercial Variable Recurring Payments (cVRP) infrastructure. GoCardless co-funded the creation of a new industry VRP scheme operator in May 2025. Commercial VRPs are beginning rollout in early 2026 - starting with charities, government, and FSCS-protected sectors, with ecommerce use cases expected later in the year. VRPs offer the flexibility of one-off payments with the cost-efficiency of Direct Debit, and GoCardless is positioned to be a primary beneficiary.

Pros

- cVRP infrastructure play - well-positioned for the UK's open banking payment evolution

- 350+ integrations with accounting, billing, and CRM tools (Xero, QuickBooks, Zuora, Salesforce)

- Pay-as-you-go pricing with no monthly contract required

- 100,000+ businesses, $130B+ processed annually

Cons

- Not a payout tool - it collects payments from buyers, it doesn't disburse to sellers

- No card payments or digital wallets, bank debit only

- 30+ countries with meaningful gaps outside Europe, UK, US, Australia, Canada

- Mollie acquisition (expected mid-2026) introduces roadmap uncertainty

- Trustpilot score is mixed (2.4/5), though G2 is much stronger (4.6/5), suggesting merchant experience varies significantly from payee experience

Merchant of Record alternatives

MoR platforms become the legal seller of your products, absorbing tax, compliance, fraud, and chargeback liability in exchange for a higher all-in fee. Unlike the above options, these are built primarily for SaaS and digital product businesses - not for routing funds between sellers.

If your problem with Stripe Connect is the complexity of selling software globally rather than managing a multi-sided payments stack, this section is for you. If you're running a marketplace with third-party sellers, this section isn't for you.

Note that some of the above platforms in this guide, including Whop Payments Network, also carry MoR characteristics alongside their platform infrastructure.

Paddle

Paddle is known as the category leader for MoR at scale. It has operated as a merchant of record for 13 years and serves 6,000+ customers.

The feature set is broad for a single integration: automated tax calculation, collection, and remittance across 100+ jurisdictions, subscription management with proration and dunning, fraud prevention, smart routing, chargeback handling, localized checkout in 17+ languages, and built-in revenue analytics via the ProfitWell acquisition.

However, the most important context to know is that in April 2025, Stripe launched Stripe Managed Payments - its own MoR product - in private preview. As of January 2026, it's live in 35+ countries with public access imminent. This is a direct competitive response to Paddle. Paddle's counter-argument is that Stripe Managed Payments is a new product from a company whose core competency is payments processing, not MoR operations - Paddle has 13 years of accumulated compliance infrastructure, tax authority relationships, and dispute resolution experience that a newer Stripe product won't immediately replicate.

Pros

- Handles tax, VAT, chargebacks, fraud, and compliance entirely - zero operational overhead for international SaaS

- 13 years as merchant of record

- Expanding local payment method coverage: BLIK, MB Way, Pix, UPI, Kakao Pay now live or in rollout

- ProfitWell Metrics included free: MRR, churn, LTV reporting without additional tooling

- Retain (dunning/failed payment recovery) included as an add-on

Cons

- Stripe Managed Payments is now a direct competitor with Stripe's brand, distribution, and infrastructure behind it

- Less customization than Stripe for complex billing logic or bespoke checkout flows

- Paddle's name appears on customer invoices and bank statements, not yours (relevant if brand consistency matters)

- Not suited to marketplaces, physical goods, or any platform where paying out multiple sellers is the primary use case

Lemon Squeezy

We're including Lemon Squeezy because it still appears widely in searches and comparisons, many SaaS founders are currently using it, and understanding where it's headed is useful information if you're evaluating it today.

Lemon Squeezy is a merchant of record platform that became popular with indie founders and early-stage SaaS teams for its simplicity: clean UI, fast onboarding, and a single 5% + $0.50 rate that covers tax, fraud, compliance, license key delivery, and affiliate management. For solo developers who just want to sell globally without thinking about VAT, it was the easiest option on the market.

That has changed significantly. Stripe acquired Lemon Squeezy in July 2024, and the team has since been building Stripe Managed Payments - Stripe's own native MoR product - directly from within Stripe's infrastructure.

Pros

- 5% + $0.50 all-in; tax, fraud, chargebacks, license key delivery, and affiliates all included

- Global tax remittance handled as MoR

- Clear migration path to Stripe Managed Payments for existing users

Cons

- Standalone roadmap is converging with Stripe Managed Payments - long-term direction is Stripe-native

- Post-acquisition onboarding has been slower than it used to be

- High take rate compounds quickly at volume

Stripe Connect alternatives compared

| Alternative | Best use case |

|---|---|

| Whop Payments Network | Platforms & marketplaces wanting full-stack infrastructure without building a payments stack |

| Stripe Connect | Developer-first platform & marketplace payment infrastructure |

| Adyen for Platforms | Enterprise platforms needing best-in-class acquiring infrastructure |

| Checkout.com | Platforms needing granular split payment configuration |

| Mollie Connect | European platforms needing local payment method coverage |

| Rainforest | Vertical SaaS platforms replacing Stripe Connect |

| Payoneer | Mass payouts to global freelancer & seller networks |

| PayPal / Hyperwallet | Mass payouts with broad consumer wallet reach |

| Trolley | Disbursement-only infrastructure for global payee networks |

| Routable | AP automation + outbound disbursements under one system |

| Tipalti | Complex global payee networks with dedicated finance teams |

| GoCardless | Recurring payment collection, Europe & Australia |

| Paddle | SaaS & digital products selling globally |

| Lemon Squeezy | Early-stage SaaS & indie founders |

How to choose the right Stripe Connect alternative for your business

The alternatives in this guide solve different problems, and the right one depends entirely on what's actually breaking down for your platform.

Most switching decisions come down to one of three things: cost at volume, geographic gaps, or the operational burden of managing compliance in-house. Understanding which of those is your primary problem will cut the shortlist significantly.

What to evaluate

Coverage is the most common reason platforms and marketplaces start looking elsewhere. Stripe Connect reaches 46+ countries, which is enough for many businesses, but leaves meaningful gaps in Southeast Asia, Latin America, and parts of Africa.

Before you evaluate alternatives, map where your payees actually are today - not where you're projecting to be - and check rail-level support, not just country-level headlines. A provider listing 150+ countries doesn't help if it can't deliver to local bank accounts in the specific markets you need.

Then, there's the cost. Published rates are a starting point, not a conclusion. The real number includes FX conversion markups, instant payout premiums, dispute fees, platform fees, and the cost of compliance or tax tooling you'd need to add alongside.

For context, Stripe's modular pricing - base processing plus Stripe Billing, Stripe Tax, and international card fees - can reach 7–10% all-in for a typical international SaaS business, compared to a flat rate of 5% + $0.50 which bundles all of that. The comparison that matters is total cost at your actual volume, not rate card vs. rate card.

The most important decision in this evaluation is your compliance model. MoR platforms absorb tax, fraud, and chargeback liability entirely in exchange for a higher fee: so if you don't want to build that capability in-house, the fee is worth it. On the other hand, if you have the team to manage it and want the control, PSPs and payout specialists hand that responsibility back to you.

And never ignore integration complexity and time to market - these matter more than they're usually given credit for.

Some solutions in this guide can be live in days with minimal engineering. Others assume a dedicated payments engineering resource and a multi-month implementation. The configurability tends to scale with the complexity, so this is really a question of what your team can absorb not just at launch, but on an ongoing basis.

Before you start a vendor conversation

The single most underestimated part of switching is connected account migration. Moving active connected accounts - particularly those with saved payment methods or live subscriptions - is the hardest and most disruptive part of any infrastructure change. Before entering a sales process with any vendor, ask specifically how they handle it and get the answer in writing.

Payments is strategy, not a default

Default infrastructure choices tend to hold until they don't - and by the time volume, geography, or compliance complexity makes the cost visible, switching is harder than it needed to be. The platforms growing fastest treat payments as strategy, not necessity. Multi-PSP routing, optimized authorization rates, and owned payment infrastructure turn what most businesses treat as overhead into a driver of revenue.

The right alternative depends on your volume, geography, vertical, and compliance appetite. There's no universal answer - only the right fit for your specific profile, evaluated against total cost of ownership rather than headline rates. Migration is not easy by any means, but it's a decision worth making deliberately rather than by default.

For founders and operators building businesses that want payments, routing, payouts, and compliance handled natively under one integration - without assembling a multi-vendor stack - Whop Payments Network is the answer.

FAQs

What's the main reason platforms switch away from Stripe Connect?

The most common trigger is cost at volume. Stripe Connect's modular pricing - base processing plus Connect account fees, instant payout fees, FX conversion fees, and dispute fees - is manageable early on, but the all-in rate tends to expand significantly as transaction volume grows. Geographic gaps are the second most common driver: platforms expanding into Southeast Asia, Latin America, or parts of Africa often find that Stripe's payout network can't deliver to local bank accounts in the specific markets they need.

Is switching from Stripe Connect to an alternative difficult?

The integration work is usually straightforward. The hard part is connected account migration: moving active sub-merchants, particularly those with saved payment methods or live subscriptions, is the most disruptive element of any infrastructure change. Before entering a vendor sales process, get explicit written confirmation of how the provider handles connected account migration.

What's the difference between a full Stripe Connect replacement and a payout specialist?

A full replacement - Whop Payments Network, Adyen for Platforms, Checkout.com - handles the entire money movement stack: pay-ins, fund routing, compliance, and payouts under one integration. A payout specialist like Trolley, Tipalti, or Routable sits downstream of your existing PSP and handles disbursements only.

When does a Merchant of Record model make more sense than a standard PSP?

When the cost of managing tax, compliance, and chargeback liability in-house exceeds the MoR's fee premium. For SaaS and digital product businesses selling globally, the MoR model absorbs VAT registration across jurisdictions, sales tax remittance, fraud liability, and dispute handling entirely, in exchange for a higher all-in rate.

Does using multiple payment providers actually reduce risk, or just add complexity?

Both, if done without a clear architecture. The risk reduction is substantial: single-provider dependency means a compliance event, policy change, or risk review at your PSP can freeze funds or interrupt processing at exactly the moment you can least afford it, as the Flipcause case demonstrated. But the complexity cost of maintaining multiple direct integrations is also to be considered. The cleaner path for most platforms is multi-provider orchestration through a single integration layer, which distributes processing across providers while keeping the operational overhead manageable.