Learn what a PayFac is, how PayFacs compare to processors, ISOs, and MoRs, and why a Merchant of Record may be the better way to monetize payments.

Key takeaways

- PayFac-as-a-Service lets platforms embed payments and onboard sub-merchants in minutes without building infrastructure or assuming full regulatory risk.

- The PayFac model replaces slow, per-user merchant account setups with a single master merchant account that scales onboarding instantly.

- A Merchant of Record goes further than a PayFac by assuming full transaction liability, including tax, compliance, and chargebacks.

When you're running a platform, SaaS, or marketplace, getting your users set up to accept payments shouldn't take weeks.

But with traditional acquiring, it usually does.

Platforms like Stripe, Adyen, and PayPal changed that by making onboarding faster, handling underwriting, and keeping payments native to the product experience

That’s known as the PayFac model.

Not only do they allow marketplaces to keep payments native to their product, but they introduce opportunities for monetization through embedded finance tools.

In this guide, we’ll break down how PayFacs work, how they compare to processors and ISOs, and when it makes sense to use a PayFac-as-a-Service, or become one yourself.

What is a PayFac?

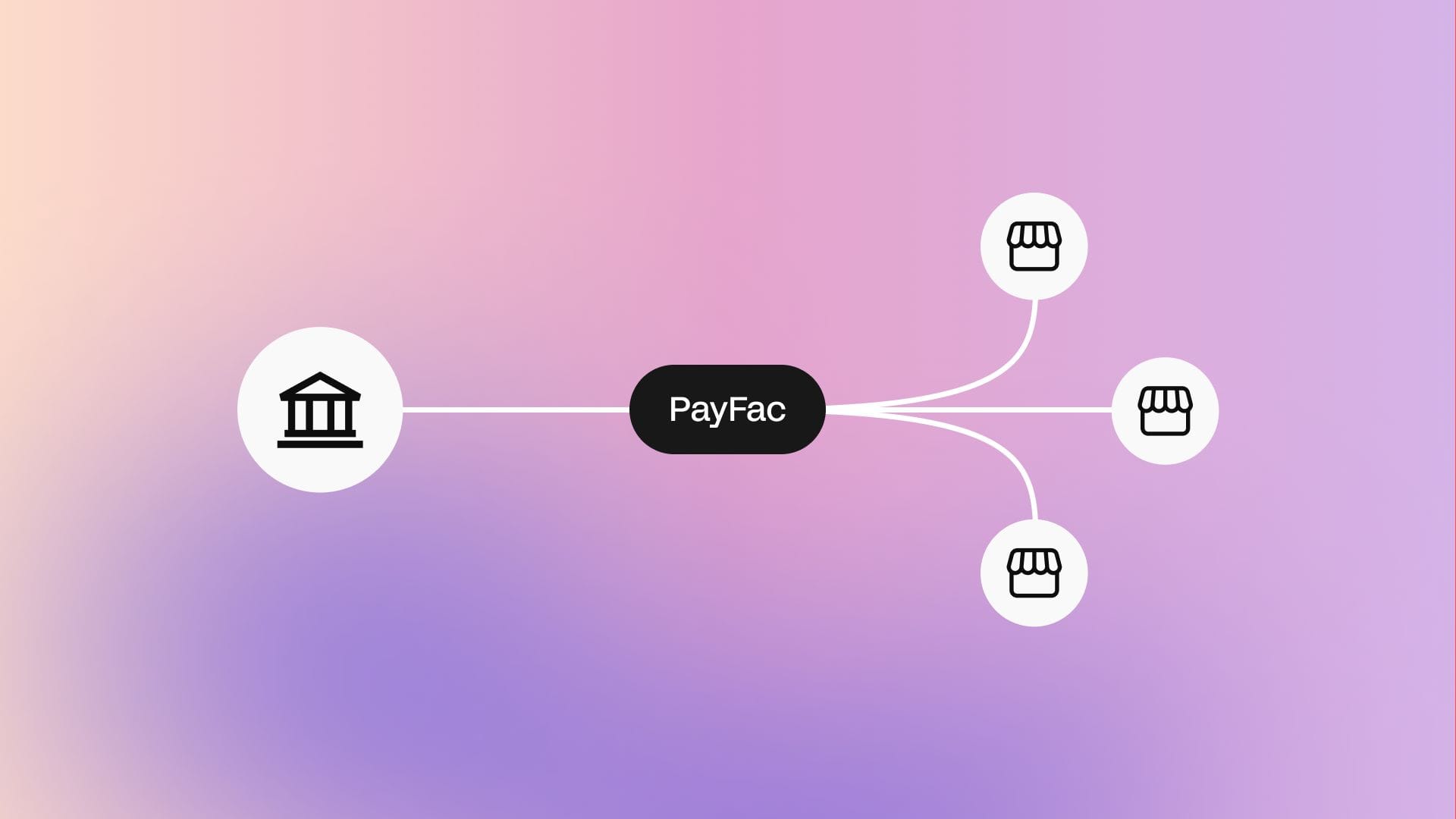

A PayFac (payment facilitator) is a company that enables other businesses to accept payments without needing their own merchant account.

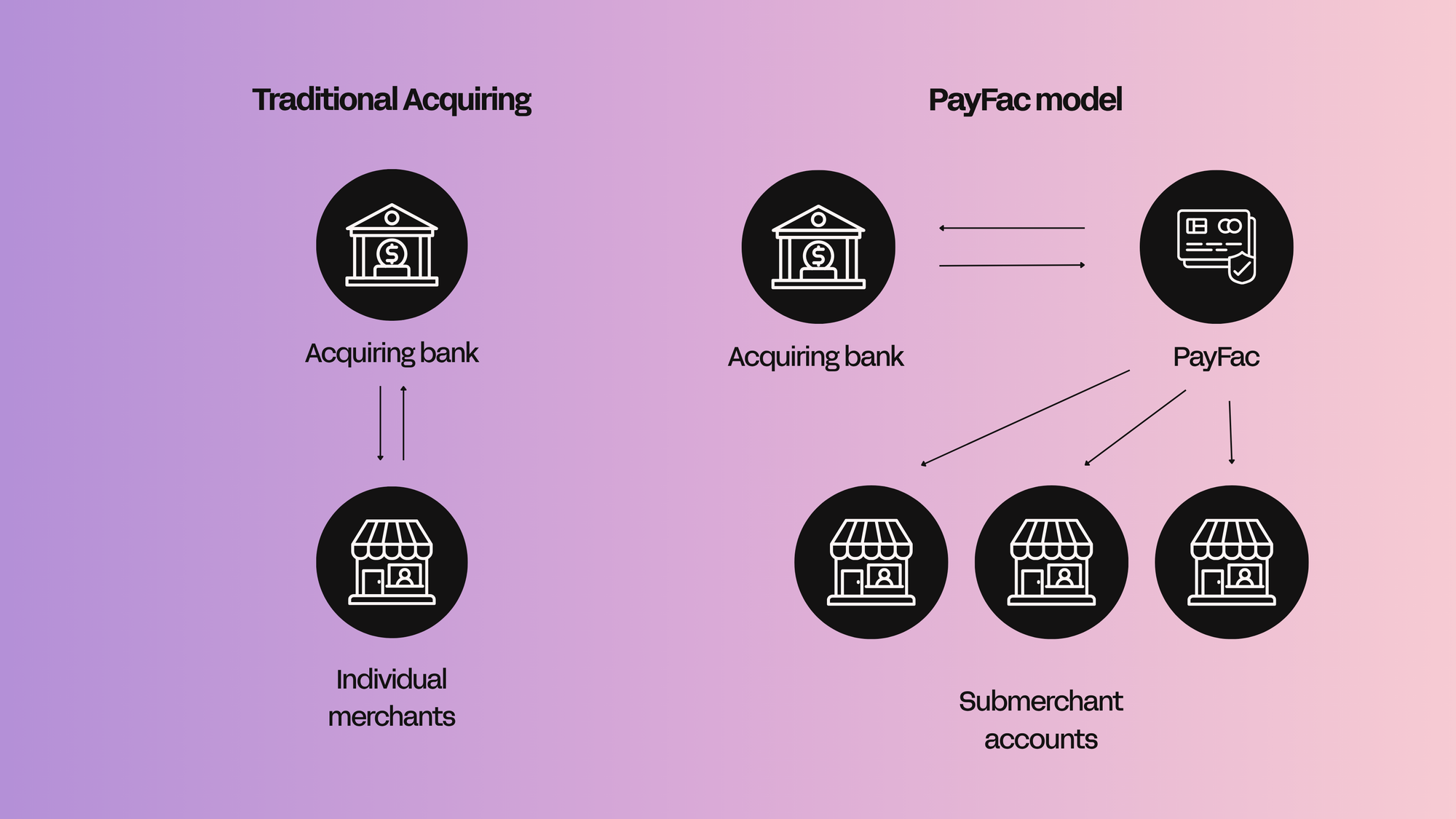

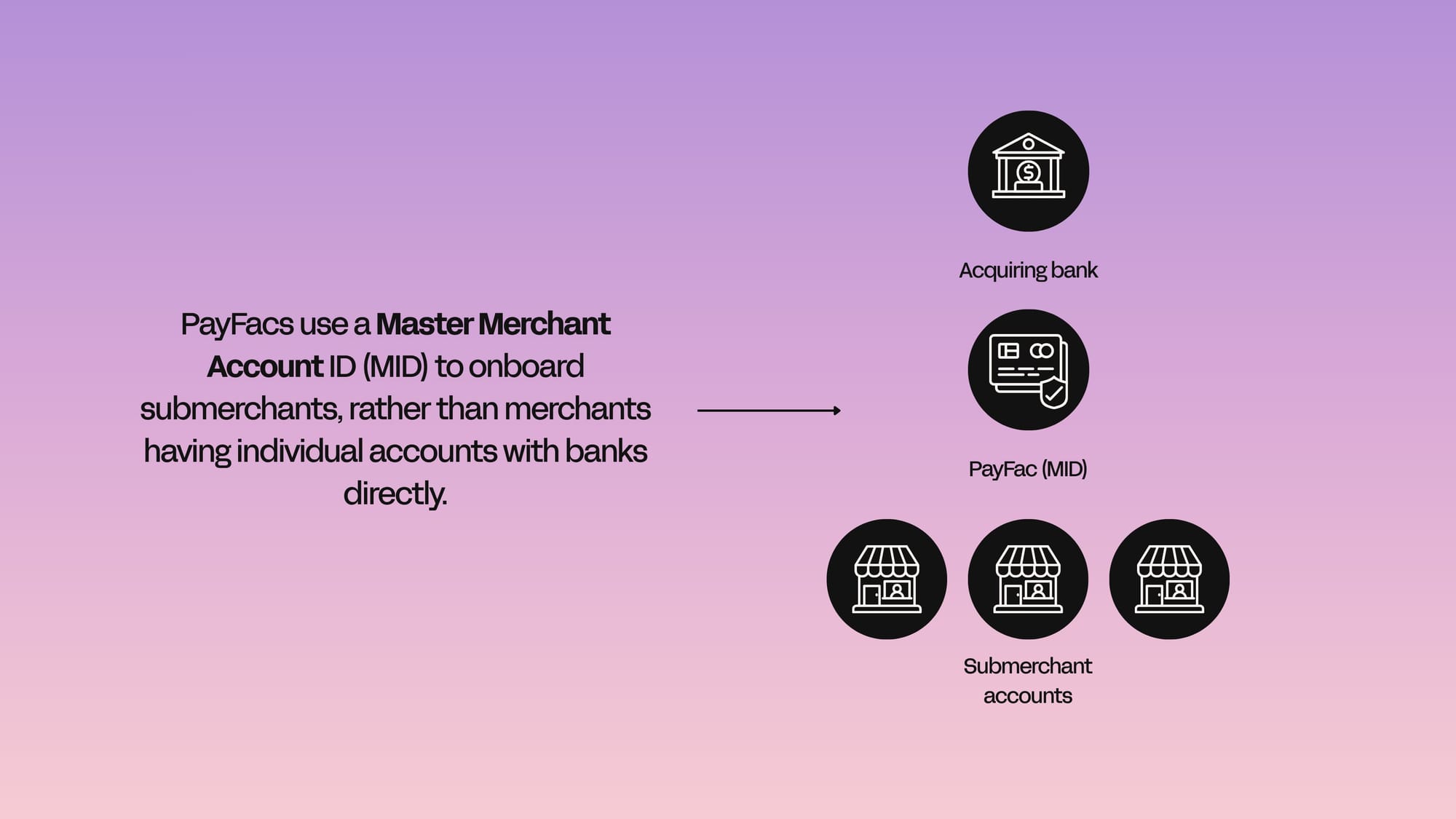

Instead of every seller, creator, or business on your platform going through a bank individually, the PayFac creates a single master merchant account (MID) with an acquiring bank, and onboards your users as sub-merchants under it.

It’s one of the key models behind embedded payments, and it’s become a huge part of how modern platforms monetize.

BTW: Embedded finance isn’t slowing down, either. The market is projected to pass $7 trillion in global transaction volume by 2030, with PayFac-as-a-Service playing a major role.

Why PayFacs hold one Master Merchant Account (MID)

Each PayFac holds one master merchant ID (MID) with an acquiring bank. When you sign up with a PayFac, every user on your platform operates under that umbrella, rather than needing their own direct merchant account.

So instead of:

- Every seller opens their own merchant account

You get:

- The PayFac holds one master merchant account

- Your users are onboarded as sub-merchants under it

Payments still go to the right sellers, but everything runs through that shared setup.

That’s what makes onboarding faster and lets you keep payments fully inside your platform.

Understanding PayFac-as-a-Service (PFaaS)

PayFac-as-a-Service (PFaaS) is a model where you get the benefits of being a PayFac, without actually becoming one.

Basically, instead of setting up your own PayFac from scratch (which would require personally registering with card networks, building compliance systems, managing risk, and partnering with an acquiring bank), you plug into a provider that already has all of that in place.

They handle the infrastructure. You build the product on top.

Easy.

Why platforms choose a Payfac-as-a-Service

Becoming a full PayFac is heavy. Sure, you get total control over your platform, how money moves, fees, and security. But the trade off is pretty huge.

You’re also taking on compliance (KYC, AML, PCI DSS), underwriting and risk monitoring, and managing relationships with acquirers and card networks. Not to mention the ongoing reporting and regulatory obligations.

The risk economics of PayFacs are often misunderstood. You're not just taking a bigger revenue share, you're taking on the credit exposure of every single sub-merchant in your portfolio.

— George Peabody, Founder 'Payments on Fire' Podcast

All of this makes becoming your own PayFac expensive, slow, and operationally complex. PFaaS removes that barrier.

Trust me, this is legit. Mastercard’s 2025 white paper found that using a PFaaS can reduce time to market from months to weeks! It can even collapse merchant onboarding from weeks to minutes.

Platforms want (scratch, need) embedded payments, fast onboarding, and control over monetization. What they don’t need is to spend 6 to 12 months building payments infrastructure or taking on full regulatory risk.

"Five years ago the question was 'What is a PayFac?' ," says Karen Webster, CEO of Market Platform Dynamics. "Today, the question is 'Which PayFac-as-a-Service provider should we use?'"

PFaaS gives you a shortcut. You get PayFac-level capabilities (like onboarding sub-merchants, managing payouts, and embedding payments) without owning the entire stack.

How does a PayFac actually work?

As PayFacs sit between your platform and the payments infrastructure, they typically handle everything needed to let your users accept payments.

Traditional merchant account vs PayFac model

| Feature | Traditional merchant account | PayFac model |

| Setup | Each user applies separately | Users onboarded under one PayFac |

| Onboarding speed | Days–weeks | Minutes–hours |

| Experience | Off-platform | Built into your product |

| Compliance | Per business | Handled by PayFac |

| Scalability | Manual + slow | Fast + repeatable |

Here’s what that looks like step by step.

Step 1: The PayFac sets up the infrastructure

Like I explained earlier, PayFacs partner with acquiring banks to get master merchant accounts (MIDs). That’s the foundation.

This connects the PayFac to payment processors and gateways, so it can actually move money (via payment rails) between buyers and sellers on your platform, and external banks.

Step 2: You onboard users as sub-merchants

When someone joins your platform and wants to get paid, they don’t apply for their own merchant account. They’re onboarded under the PayFac.

It usually happens through a simple sign-up flow, where the PayFac provider collects key info (business details, identity, etc.) and runs automated checks. This simplifies sub-merchant onboarding and drastically reduces time spent.

This is where KYC (Know Your Customer) and AML (anti-money laundering) checks come in, but they’re usually handled behind the scenes.

Step 3: Payments flow through the PayFac

When a customer pays, it looks like this:

- The payment is processed through the PayFac’s infrastructure

- Funds are routed through the PayFac’s master merchant account

- The correct amount is allocated to the sub-merchant

- Payouts are sent to your user’s bank account (or crypto wallet, etc)

From the user’s perspective, it’s seamless. They can accept payments without leaving your platform.

From your perspective, the entire flow becomes embedded finance, giving you more control over monetization, fees, and the overall user experience.

Step 4: The PayFac handles submerchant compliance

Because everything runs through your PayFac’s merchant account, it takes on responsibility for underwriting sub-merchants, monitoring transactions, and handling fraud and chargebacks.

The PayFac also manages compliance requirements like KYC, AML, and PCI DSS (either directly or through underlying partners).

Your platform doesn’t need to deal with banks directly, but someone still has to own that risk.

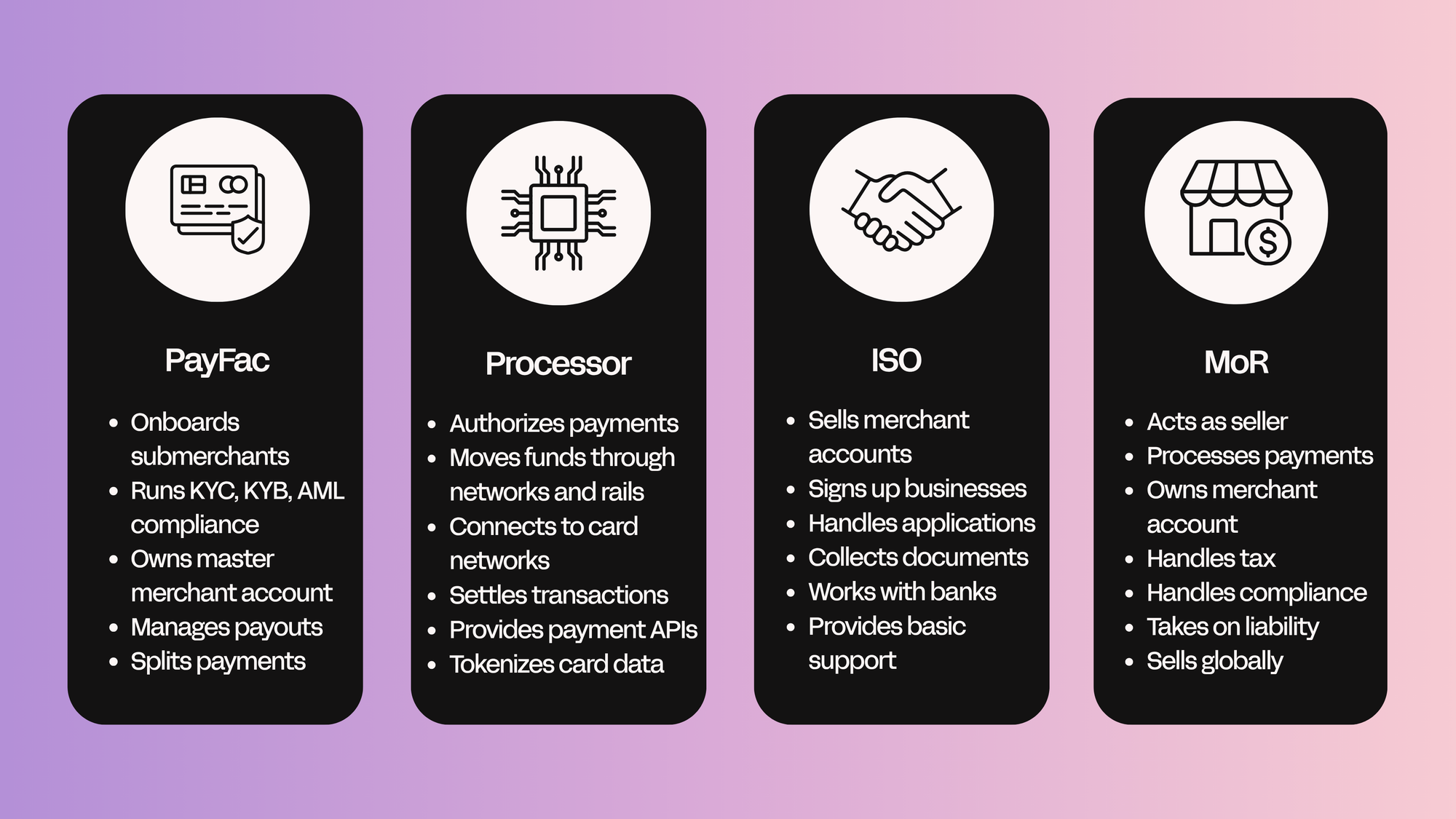

PayFac vs. other payment models

When you’re setting up payments for a platform, SaaS product, or marketplace, you’ll come across a few different models pretty quickly: PayFacs, payment processors, ISOs (Independent Sales Organizations), and Merchants of Record (MoRs).

They all help you accept payments, but they operate at completely different layers. The model you choose affects everything from onboarding to liability.

The easiest way to understand it is this: who is the merchant, and who actually takes the payment?

| Model | What it does | Who gets paid | Best for |

| PayFac | manages sellers | sub-merchant | platforms |

| Processor | moves money | merchant | payments infra |

| ISO | sets up accounts | business | SMBs |

| MoR | sells + handles | MoR | global selling |

Here’s the breakdown.

Payment processor

Payment processors are the infrastructure layer that moves money.

It connects your platform (via a payment gateway) to card networks and the acquiring bank, handling transaction authorisation, routing, and settlement.

But that’s where its role ends.

A processor doesn’t onboard your users as sub-merchants, provide a master merchant account, or handle KYC/AML compliance for your users. It also doesn’t manage payouts, or platform-level monetization

So if you’re only using a processor, you’re still relying on either:

- Each user having their own merchant account, or

- A PayFac layer on top

That’s why processors are best thought of as rails. You still need something on top to actually run payments for your users.

ISO

An ISO (Independent Sales Organization) helps businesses open merchant accounts with an acquiring bank. But unlike a PayFac, there’s no shared model.

Every user on your platform still needs to:

- Apply for their own merchant account

- Go through underwriting

- Complete KYC/AML checks

- Maintain PCI DSS compliance

The ISO just facilitates that process, it doesn’t remove it. For platforms onboarding users at scale, this creates a lot of friction, and fast.

You’re repeating the same setup process for every single seller. 500 sellers? That's 500 individual merchant account sign ups. It's time consuming, and competitors using PayFacs can do it in a fraction of the time.

Merchant of Record (MoR)

A Merchant of Record (MoR) goes one step further than a PayFac.

Instead of just facilitating payments, the MoR becomes the legal seller of the transaction. That means it takes on responsibility for things like tax, compliance, and chargebacks (not the platform, or the seller).

With a PayFac, your users are still the merchant. The PayFac handles payments and compliance infrastructure, but liability ultimately sits with the sub-merchant.

With an MoR, that liability shifts. This can simplify things like tax and regulatory compliance big time.

The Merchant of Record model gives you a different lever entirely. Instead of optimizing on top of a payment stack, you're re-architecting who owns the transaction. That changes what's possible in terms of recovery, retry logic, and authorization.

— Rehman Baig, Chief Product Officer, FlexFactor

Can I become my platform's own PayFac?

Technically, yes – but it isn't easy. To become a registered PayFac, you need approval from an acquiring bank and to register with card networks like Visa and Mastercard.

On top of all that, you’re taking on full liability for everybody on your platform (and you know what they say about one bad apple).

If something goes wrong (fraud, chargebacks, regulatory issues) it’s on you, and can affect your entire platform and user-base until it's resolved.

So, instead of building a full payments operation from the ground up? Most platforms, SaaS companies and marketplaces often turn to using a PFaaS (PayFac-as-a-Service) or a Merchant of Record (MoR).

These models still give you PayFac benefits (onboarding merchants, controlling the payment experience, monetizing payments), without actually building any infrastructure yourself, and with a lot less risk.

The difference is how much responsibility is on you: PFaaS still leaves you as the merchant, while an MoR takes on that role (and the liability) for you.

Why marketplaces, platforms and SaaS use a Merchant of Record

Running your own payments stack sounds great, until you realize you’re now responsible for tax, compliance, fraud, and liability across every market you sell into.

Headaches, am I right?

An MoR removes that, handling transactions and taking on liability. It even deals with the messy parts (like tax, chargebacks, and compliance), so you don’t have to.

And you don't have to give anything up. MoRs like Whop still allow you to take a cut of transactions, manage pricing, run subscriptions, offer financing, and pay out users globally.

With Whop Treasury, your business can even earn yield on idle balances.

Which payments model should your platform choose?

We’ve explored how PayFacs work, how to become one (and whether it’s worth it), why platforms use PayFac-as-a-Service, and how you can go one step beyond that again by using an MoR.

So what’s the right choice? Truth is, it comes down to how much control (and responsibility) you’re willing to take on.

- Want full control and have the resources to manage compliance, risk, and operations? Then becoming a PayFac can make sense. But that’s lowkey rare, especially for startup platforms and SaaS products.

- If you want PayFac-level capabilities without building infrastructure, PayFac-as-a-Service is the middle ground. You still operate as the merchant, but you offload a lot of the heavy lifting.

But if you’re chasing the simplest path to global monetization? You need a Merchant of Record. You won’t have to deal with tax, compliance, or liability, but you still control how you make money.

As Todd Ablowitz, CEO of Infinicept, says, "A payment facilitator enables you to accept payments, but you are still the merchant. You still own the tax registrations, the filings, the exposure. A Merchant of Record flips that. They step in front of you legally. That's a fundamentally different risk transfer."

Get an MoR-backed payments stack with Whop

Whop gives you a complete, MoR-backed payments stack straight out the box, so you can start accepting payments, onboarding users, monetizing money flows, and paying out globally from day one.

If you want more control? We also have an API to customize how everything works inside your product. Refine onboarding flows, control pricing, manage payouts, and build your own monetization logic on top.

If something breaks (or you need help), you get 24/7 support from a team who actually knows what they're doing.

Forget bundling together compliance tools, tax solutions, processors, and payout systems. Whop gives you all of it, in one place, with low fees and maximum profit potential.