Learn how 3DS authentication works on Whop to increase successful sales and reduce chargebacks and fraudulent activity.

Key takeaways

- Whop 3D Secure verifies cardholders through their banks, reducing fraud and shifting chargeback liability from merchants to issuers.

- Challenge-based 3DS boosts approval rates on high-ticket purchases by bringing buyers directly into the verification process.

- Merchants can enable 3DS per product in seconds, with challenges automatically required on transactions over $1,000.

Reducing fraudulent payments and increasing successful conversions is the name of the game.

With chargeback volume increasing by 40% in the last few years; and global fraud losses expected to reach $107 billion by 2029, tighter security is becoming a top priority.

One of the simplest ways to reduce fraud and maximize successful charges is by implementing 3DS, or 3D Secure.

This extra technical layer requires cardholders to verify their identity with their bank, and shifts liability for fraudulent charges onto issuers rather than merchants.

Here’s a closer look at how 3DS works on Whop.

What is 3D Secure?

3D Secure (3DS) is a security protocol for online card payments that helps verify that the person making a purchase is the cardholder.

Rather than relying solely on card details, which is pretty high-risk today (details can be easily scraped or stolen), 3DS allows banks to assess the risk of a transaction and request additional verification when necessary.

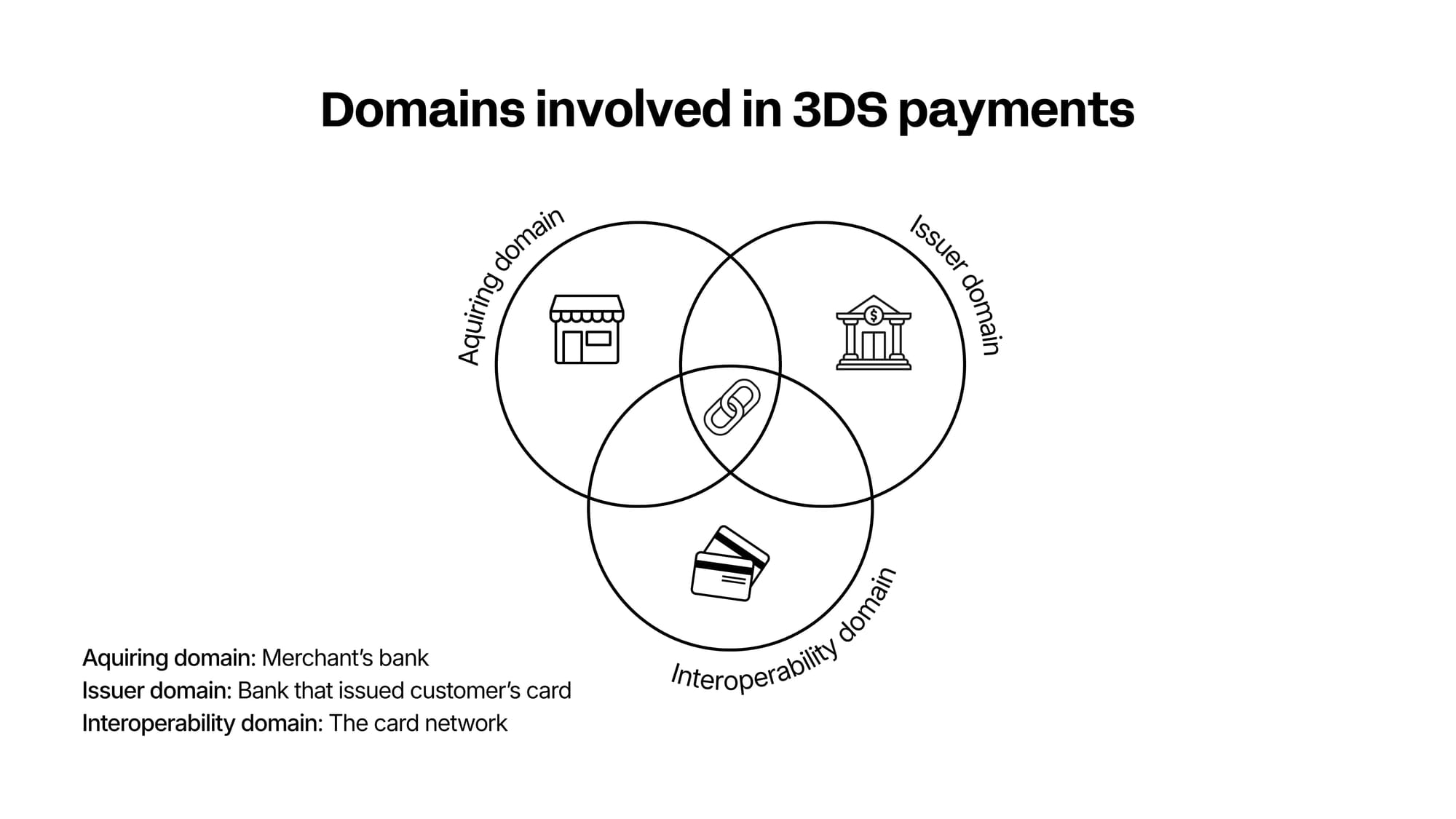

Originally developed by Visa, 3D Secure has since become the global standard for cardholder authentication across major card networks.

The name comes from the three domains involved in the process: the merchant's bank (acquirer), the cardholder's bank (issuer), and the card network itself.

Together, these parties exchange encrypted information to verify payments and reduce fraud.

The two main types of 3DS

Not all 3DS transactions look the same, as they fall into two categories: frictionless and challenge.

1. Frictionless 3DS

With frictionless 3DS, the customer doesn't need to do anything extra.

Instead, information about the transaction is sent to the issuing bank, which uses its own risk models to determine whether the payment is legitimate. If the bank is satisfied, the transaction is approved without interrupting the checkout flow.

2. Challenge 3DS

With challenge 3DS, the cardholder is asked to verify the transaction before it can be approved.

Depending on the bank, this may involve:

- Entering a one-time passcode (OTP)

- Approving the transaction through their banking app

- Using biometric authentication such as Face ID or fingerprint verification

Think of challenge 3DS as two-factor authentication, helping confirm that it’s genuinely the cardholder making the purchase.

Key benefits of selling with 3DS security

3DS isn’t only about security. In reality, it can also help merchants increase successful payments, protect revenue, and reduce operational risk, all at the same time.

Improve approval rates on high-ticket purchases

Large online purchases often trigger additional scrutiny from banks. Without strong authentication, genuine transactions can be declined simply because the issuer isn't confident the cardholder is making the purchase.

By requiring the buyer to verify high-value transactions, 3DS gives banks greater confidence to approve payments.

According to Whop Payments Engineer Ritvik Gudlavalleti:

"Merchants who were normally doing transactions over $10K, $15K saw a lot of declines just because of this issue. Thanks to challenge 3DS, customers are now in the loop of the transaction fully and it helps ensure conversions overall go up."

Reduce fraud risk

3DS adds an additional layer of authentication beyond card details alone.

Even if a fraudster has access to a card number, they may still be unable to complete the purchase if they can't pass the issuer's verification process.

TL;DR: It allows us to confirm that this is a valid transaction and gives banks or issuers the ability to understand that this is also a valid transaction (not fraud).

Protect high-risk and high-value products

Not every product requires the same level of protection.

Whop allows merchants to enable 3DS on specific products, plans, checkout links, invoices, or across their entire company. This makes it simple to apply additional security only where it's needed most.

For purchases above $1,000 USD, Whop automatically requires a 3DS challenge to help protect both buyers and sellers.

Increase buyer confidence

Customers are increasingly aware of online fraud and payment scams. Seeing authentication come directly from their bank can reassure buyers that a transaction is legitimate, particularly when making a large purchase.

Rather than creating friction for the sake of it, challenge-based authentication gives buyers a clear opportunity to confirm they're comfortable proceeding with the payment.

Meet PSD2 and SCA requirements

Strong customer authentication isn't always optional. If you sell to customers in Europe or the UK, 3DS can help you comply with important regulations.

Under the European Union's Revised Payment Services Directive (PSD2), many online card payments require Strong Customer Authentication (SCA). In practice, 3DS has become the most common way for businesses to meet these authentication requirements and reduce the risk of payments being declined by issuing banks.

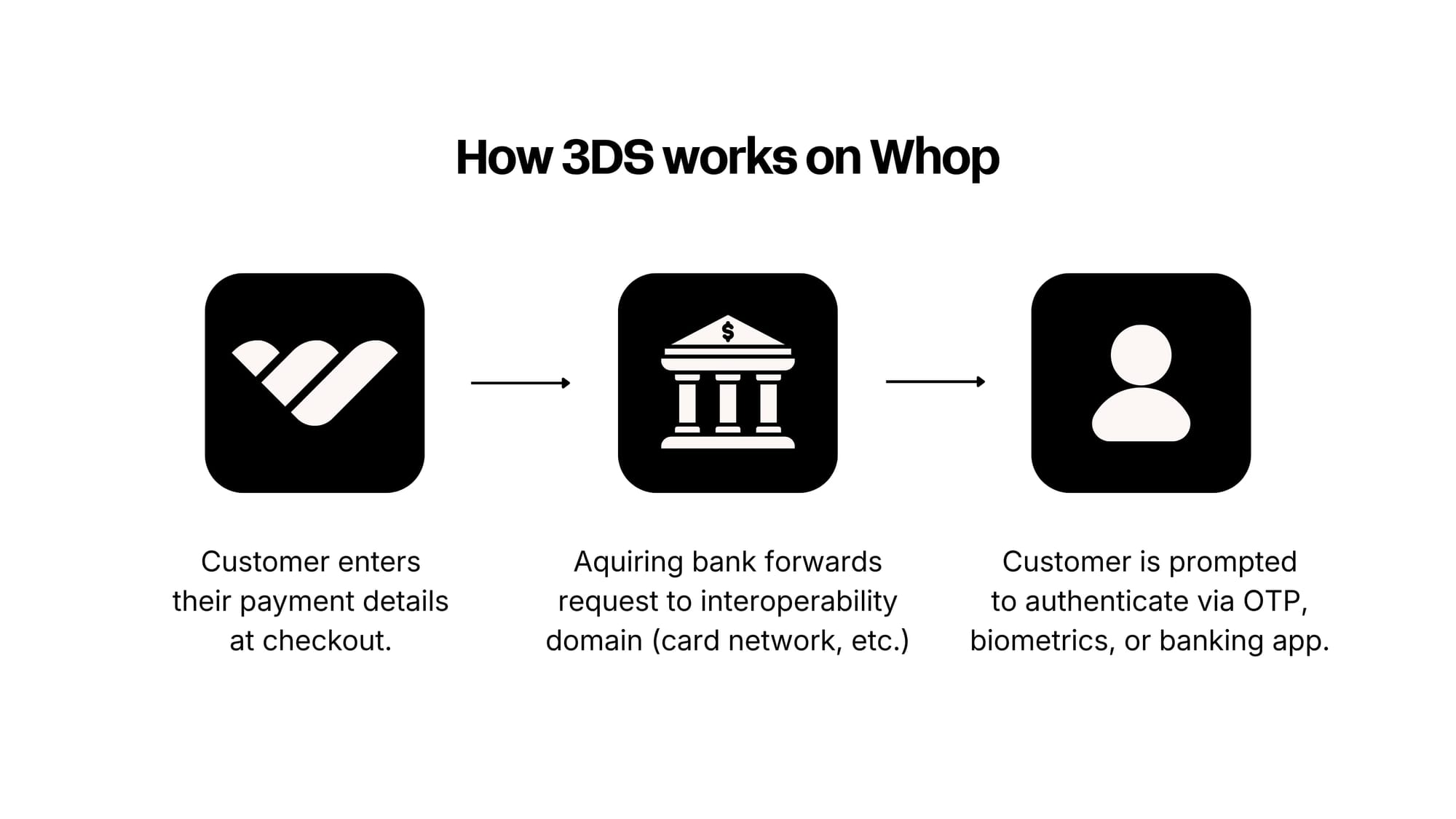

How 3DS works on Whop

Whop's approach to 3DS is built around a simple idea: involve the right people at the right time.

Low-risk purchases can often move through checkout with minimal interruption.

But when transaction values increase, additional verification can give both buyers and banks more confidence that the payment is legit.

For products, plans, and services under $1,000, sellers have two 3DS options:

Challenge when needed

This setting allows the issuing bank to determine whether additional verification is required.

In many cases, transactions will pass through a frictionless 3DS flow with no action required from the buyer.

However, if the bank identifies additional risk, it can trigger a challenge and ask the cardholder to verify the payment before approval.

"In frictionless 3DS, there's not really an option for a customer to approve the transaction. Instead, it goes straight to the bank and the bank gets to decide based on their own internal risk model whether or not they should accept."

– Whop Payments Engineer Ritvik Gudlavalleti

Require challenge

For higher-risk or higher-value transactions, merchants can require every buyer to complete a challenge before payment is approved.

This brings the customer directly into the verification process through methods such as one-time passcodes, banking app approvals, or biometric authentication.

How to enable 3DS on Whop

Enabling 3DS takes less than a minute and can be configured on a per-product basis.

1. Open the product you want to protect

From your Whop dashboard, navigate to 'Products', select the product you want to enable 3DS for, and head to the pricing settings.

2. Scroll to 3DS toggle

Within the Pricing section, locate the 3DS toggle and dropdown underneath the pricing and billing options.

3. Choose your authentication preference

Here, you’ll see a dropdown with three options:

- Disabled: No 3DS authentication is required.

- Challenge when needed: The issuing bank decides whether to run a frictionless flow or prompt the customer for additional verification.

- Require challenge: Requires the buyer to complete a 3DS challenge before the payment is approved.

Reminder: This will be greyed out and ‘Require challenge’ will be automatically selected for high-ticket products valued at $1K or above.

4. Save your changes

Click save to apply the new authentication settings. 3DS can be configured differently across products depending on transaction value, risk profile, or customer type.

Protect your income and minimize failed payments with Whop 3D Secure

Whop 3DS is just part of the way we help you protect your income, meet compliance requirements, and increase conversions at checkout.

As fraud becomes more sophisticated, card details alone aren’t always enough to verify payments. 3DS helps verify legitimate buyers, reduce fraudulent transactions, and give issuing banks more confidence to approve payments.

Whop allows you to enable 3DS in seconds, apply it to individual products or your entire company, and automatically protect high-ticket transactions over $1,000.

Sell with Whop and reduce payment fraud while maximizing successful charges.