Payment orchestration routes transactions across multiple PSPs in real time to maximize authorization rates, reduce failed payments, and recover lost revenue. Here's how it works and what to look for in a platform.

Key takeaways

- Single-PSP dependency silently destroys more revenue through failed payments and false declines than fraud itself.

- Payment orchestration dynamically routes each transaction to the optimal processor, recovering 6–10% in otherwise lost revenue.

- Failed payments redirect ready-to-buy customers to competitors, turning your acquisition spend into their conversions.

Commerce has become omnichannel and borderless. Payment infrastructure, by and large, has not.

Many businesses still rely on PSP integrations built market by market, fraud controls added reactively, and limited visibility across checkout flows. It's infrastructure that was never designed to scale - and it bleeds revenue every day it runs.

And the numbers are clear: eleven percent of transactions processed by the average ecommerce business failed last year, and, according to PYMNTS Intelligence, more than 80% of merchants had no clear insight into why.

The systems designed to protect revenue are, in many cases, the ones eroding it.

Payment orchestration addresses this at the infrastructure level - a single integration layer that connects PSPs, acquirers, and payment methods, with routing logic applied to each transaction in real time.

This article explains how orchestration works, the cost of operating without it, and the key factors to consider when evaluating platforms.

What is payment orchestration?

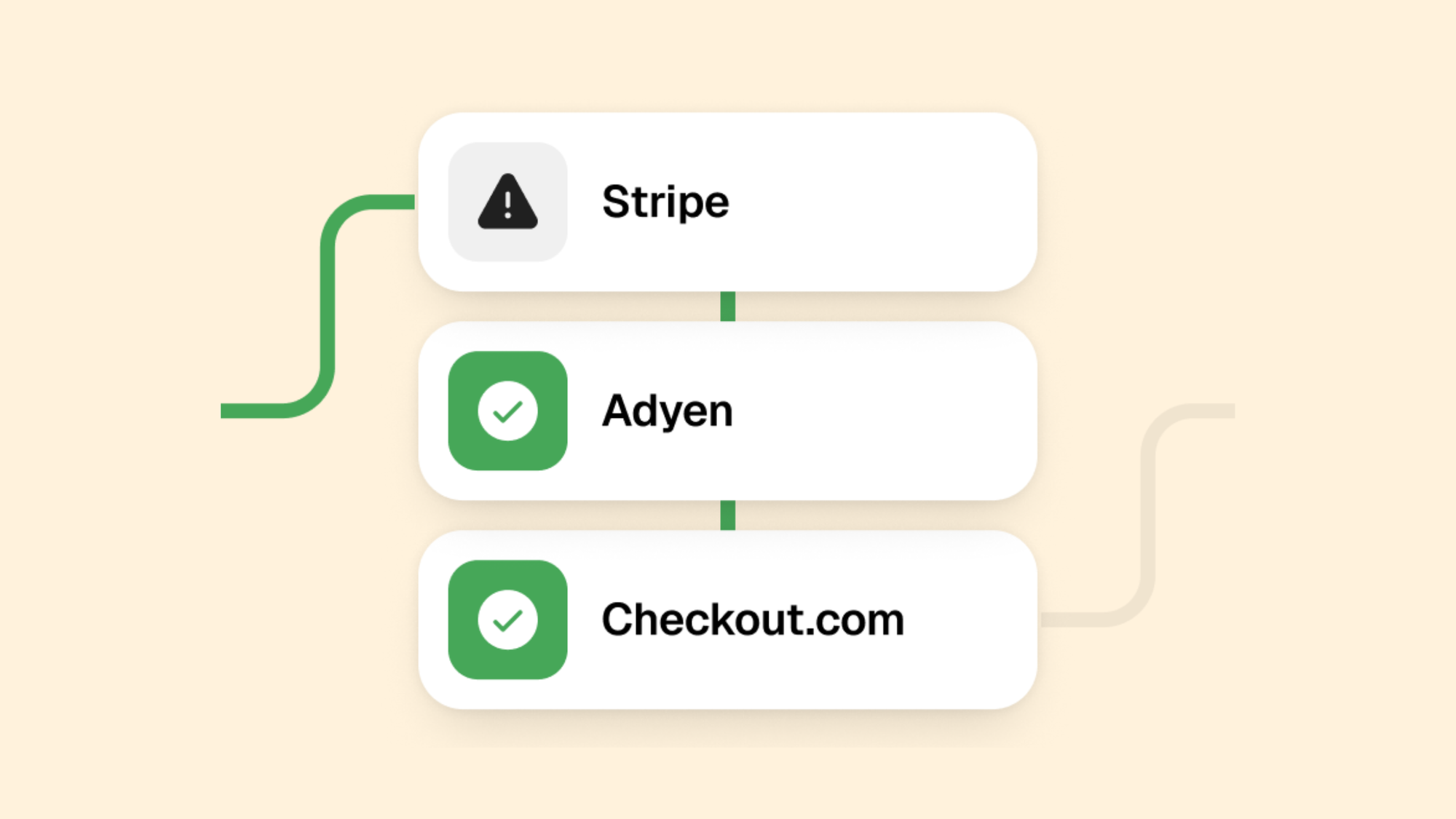

Payment orchestration connects all of your payment processors, acquirers, and payment methods in one place, and automatically decides which one to use for each transaction.

Think of it like Google Maps for your payments. When you open Maps, it doesn't just pick one route, it looks at every road available and sends you down the one most likely to get you there fastest. If there's an accident ahead, it reroutes automatically.

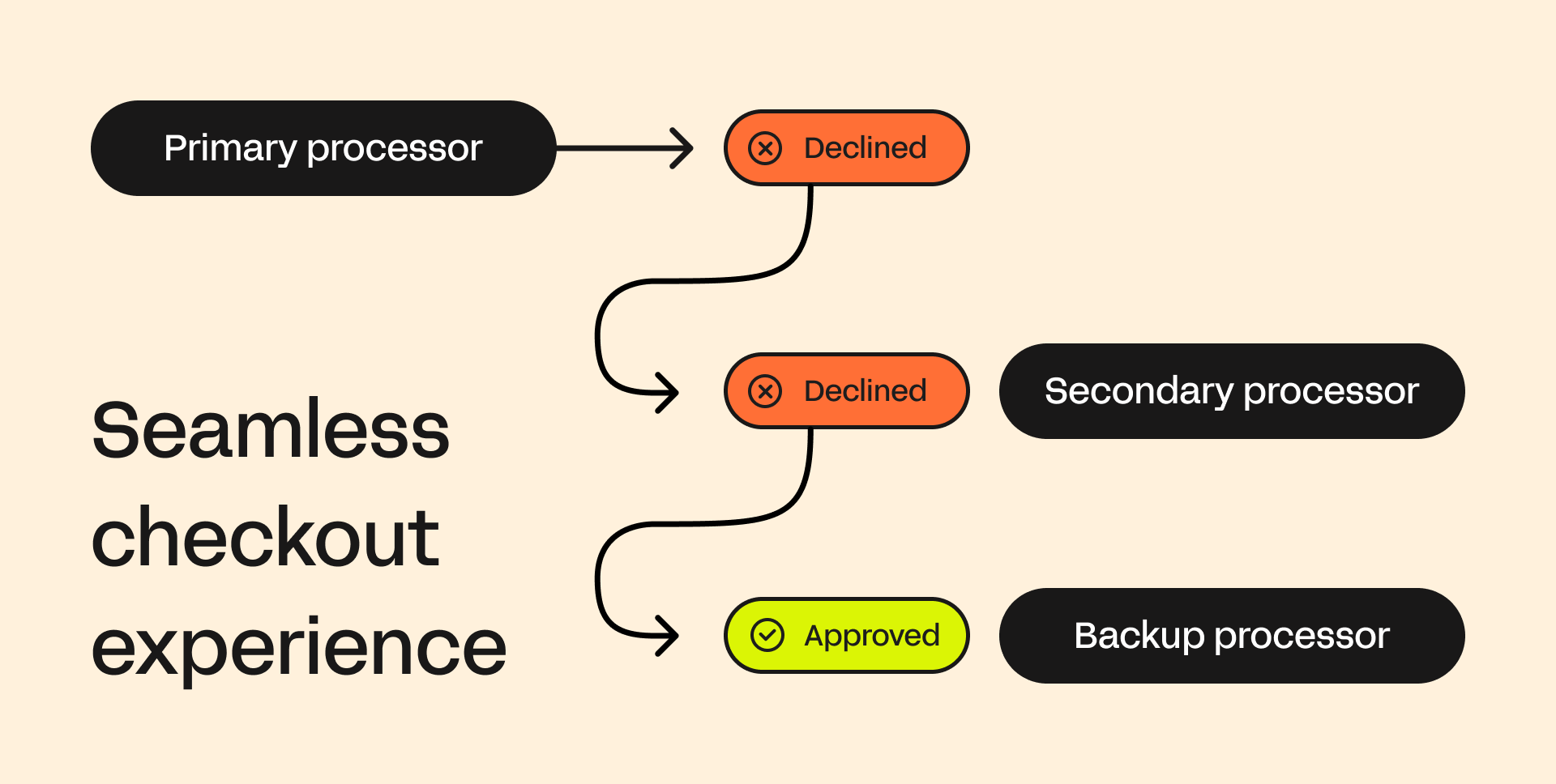

Payment orchestration works the same way. Every transaction is evaluated in real time and routed to the processor most likely to approve it. If that processor declines or goes down, the platform instantly tries another path. For customers, checkout is seamless, while behind the scenes, a different route was already taken.

That automatic retry through a different processor is called cascading, and it's one of the most direct ways orchestration recovers revenue that would otherwise be lost.

Payment orchestration vs. a payment gateway

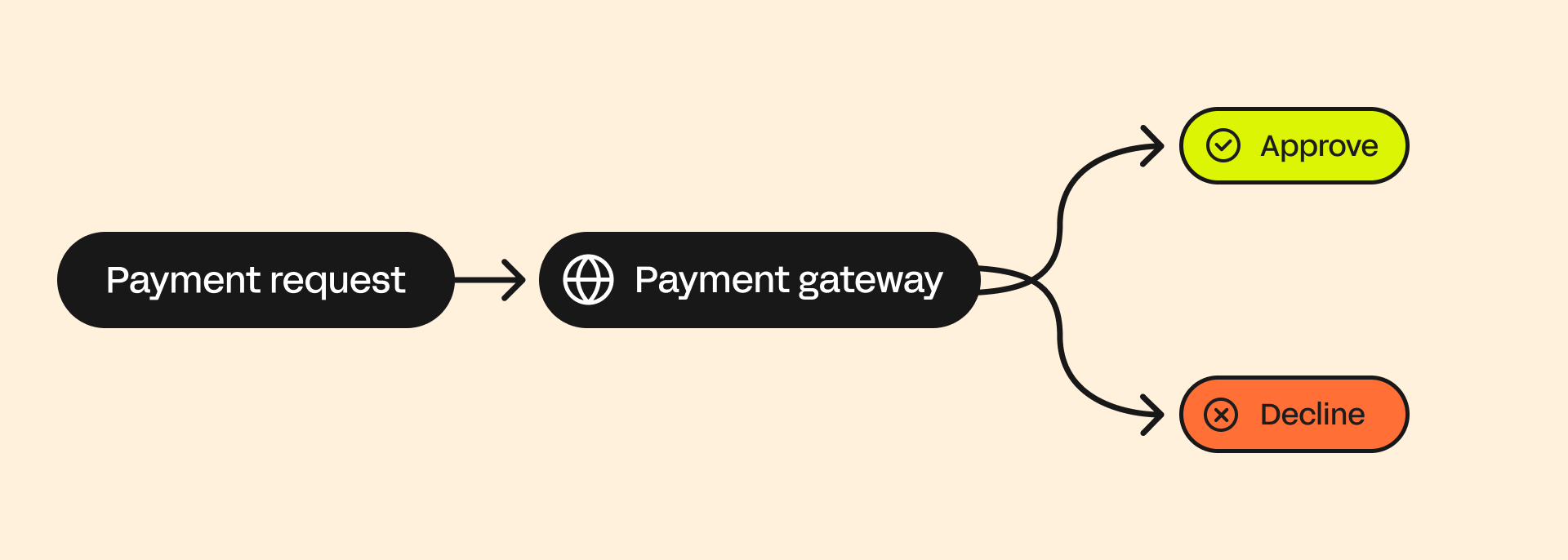

A payment gateway routes a transaction. That's its job - take a payment request, send it to a processor, return an approval or a decline. It does one thing, for one processor, in one direction.

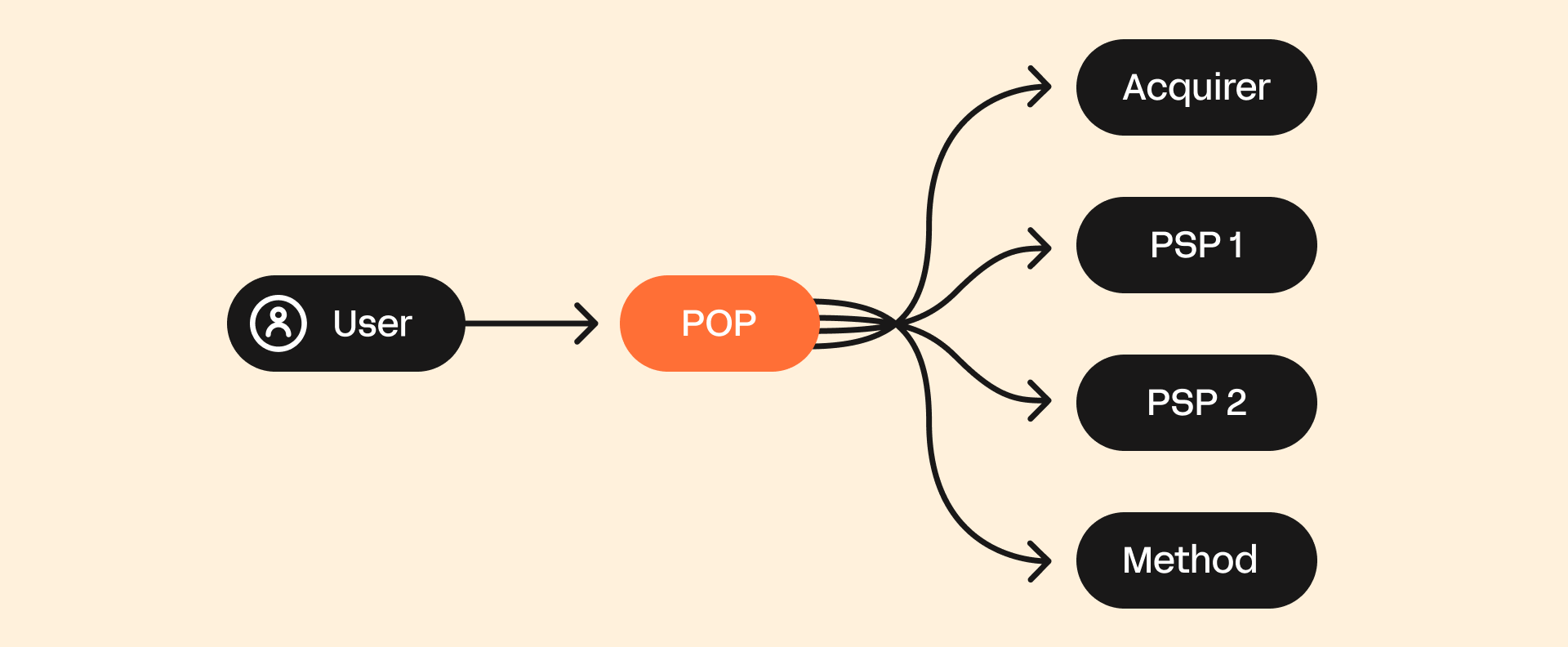

A Payment Orchestration Platform (POP) takes a fundamentally different approach. Instead of routing transactions through a single processor, it introduces an abstraction layer above your PSPs, acquirers, and payment methods - connecting them through a single integration and applying routing logic to each transaction in real time.

Even a 1% increase in authorization rates can translate into millions of dollars in additional revenue.

At that scale, can you afford to leave money on the table?

The cost of single-PSP dependency

You might be surprised to hear this next one: the average merchant loses more revenue to payment failure than to fraud.

Here's why single-PSP architecture is usually the root cause.

You're losing more revenue than you realize

The 11% transaction failure rate cited above isn't a worst-case scenario, it's an average. A merchant processing 100,000 transactions monthly, with an 18% failure rate against a $75 average order value, is losing $1.35M every month. That's $16.2M a year, gone.

But even that number understates the true cost. Authorization fees, typically ranging from $0.01 to $0.10 per attempt, are charged on failed transactions as well as successful ones, which means every declined customer interaction carries both a lost sale and a direct processing cost. Your business actually pays to lose the customer.

Cross-border transactions stack on top of this. International payment failure rates run significantly higher than domestic ones, and failed cross-border payments cost U.S. merchants an estimated $3.8B in 2023 alone.

Fraud filters generate their own revenue losses

The fraud tooling most merchants rely on was built to minimize loss, but for far too many businesses, it actually creates more of it.

Merchants reject 6% of all ecommerce orders, and between 2% and 10% of those rejections are legitimate customers being incorrectly blocked. Essentially, you're handing sales directly to your competitors. And once you've lost that sale, you've likely lost the customer, with 47% of retailers saying false declines have a severely negative impact on customer satisfaction.

I asked Maddie Cohen, Head of Trust at Whop, how often merchants underestimate the revenue they're losing to false declines compared to actual fraud. Here's what she had to say:

"You don't even realize how much money you're losing to false declines, because you never see that revenue. Every processor has its own fraud rules: some overextend blocks that another processor wouldn't flag at all." — Maddie Cohen, Head of Trust at Whop

The math doesn't hold up. A fraud tool preventing $500K in annual losses may simultaneously be generating $8M or more in false decline costs.

The problem is not that fraud prevention is unnecessary, it is that blunt-instrument implementations make no distinction between a suspicious transaction and a good customer on a bad day, and the collateral damage falls entirely on legitimate revenue.

Single-processor dependency is a business risk, not just a tech problem

Concentration risk in payments runs deeper than authorization rates. It touches operational continuity, commercial leverage, and the cost of growth.

The most direct example of this risk is downtime. A merchant operating through a single PSP with no fallback has, in the event of a processor outage, no revenue. Not reduced revenue - none.

"A lot can happen in the world of payment processing. If anything does happen to one of your PSPs or payout partners, you want to make sure you have something to fall back on." — Maddie Cohen

Without a credible alternative processor, you have a dependency on one provider. There's nothing to negotiate with on rates, nothing to point to when authorization performance slips, and no lower-cost routing path to shift volume toward when margins compress. Your provider knows it, and prices accordingly.

And every new payment method or market requires a discrete engineering engagement, with the full cost of integration repeating at every expansion.

What a failed payment does to customer retention

Most businesses treat a failed payment as a process problem - something a retry sequence will catch before the customer notices. For the majority of customers, that assumption is wrong.

The behavioral response to a declined transaction

The customer who was declined does not, in most cases, file a complaint or contact support. They leave without a word, and they complete the purchase with a competitor whose checkout worked. The relationship ends without a signal, which is precisely why the damage is so consistently underestimated.

Think about seeing an Instagram ad for a tshirt and you go to the ad and try to buy it. If you go to 'buy 'and it doesn't work and throws up an error, the likelihood of you returning to that store is very low.

- Derek Wilmer, Whop

Competitive displacement

Payment failure has a CAC problem that most finance leaders haven't priced in. Every failed payment represents acquisition spend that generated no return - a customer who was found, targeted, and brought to checkout, only to be lost at the final step.

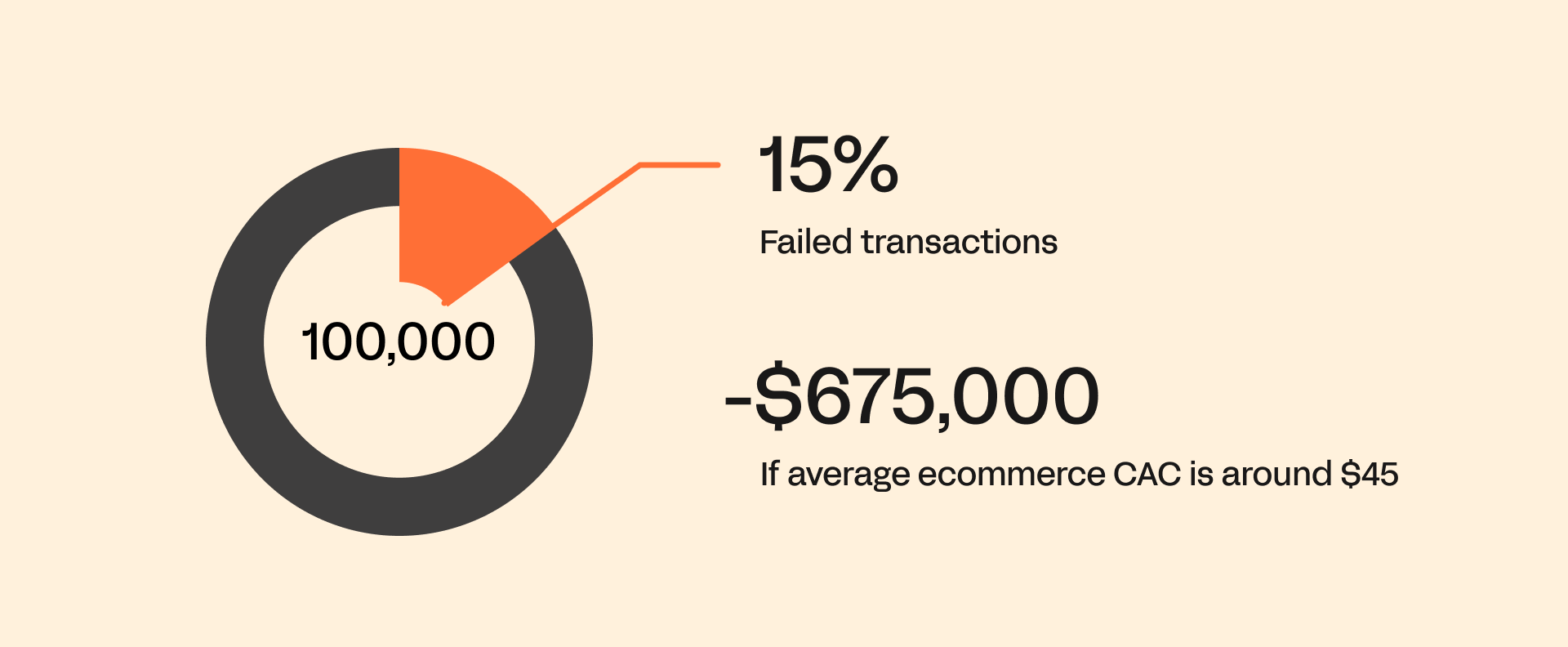

If average ecommerce CAC is around $45, and 15% of transactions are failing at 100,000 monthly volume, a significant portion of that budget is producing nothing.

And a failed payment doesn't suppress purchase intent, it redirects it. That customer still wants what they came to buy - but they can't buy it with you. They complete the transaction with whoever accepts their payment method, in their currency, through a checkout that works. The acquisition spend that brought them to your checkout effectively funded a competitor's conversion.

The same logic extends to payment method coverage. According to Primer's UK survey, 69% of consumers abandon checkout if their preferred payment method isn't available. A competitor offering local payment methods and familiar checkout experiences is not simply converting better in those moments, they are systematically capturing customers that your infrastructure is turning away.

How payment orchestration works: under the hood

Smart / dynamic routing

At the moment of a transaction, an orchestration platform evaluates a set of real-time variables - card type, issuing bank, geography, transaction size, time of day, historical authorization data by BIN range - and routes to the processor most likely to authorize.

Rather than sending every transaction to the same PSP by default, the platform is making a probabilistic optimization at the individual transaction level, informed by live and historical performance data.

And it works. Businesses on Whop see a 6–10% increase in revenue as a direct result of smart orchestration. For a merchant processing $1M monthly, that's up to $60,000-$110,000 in recovered revenue, without touching the product, the pricing, or the acquisition funnel.

Cascading / fallback logic

When a primary processor declines or becomes unavailable, the platform automatically retries through a secondary - before the customer encounters any visible friction. What appears to the customer as a seamless checkout experience is, behind the scenes, a second or third attempt routed through an entirely different path.

This is the mechanism that converts what would otherwise be a permanent decline into a recovered transaction. Stripe's Adaptive Acceptance - their AI-powered retry and cascade layer - recovered $6B in falsely declined transactions in 2024, representing a 60% year-over-year improvement in retry success rate.

Tokenization & network tokenization

A centralized vault stores customer payment credentials once and makes them portable across all connected processors, enabling seamless retries and recurring billing without requiring re-authentication at any point in the flow.

Network tokenization goes further still. Tokens issued directly by the major card networks auto-update when a card is refreshed, lost, or reissued - meaning a card that's been cancelled, expired, or replaced is updated automatically, rather than failing silently at the next billing attempt.

According to Slicker, up to 12% of card-on-file transactions fail due to card expirations and related credential issues. Most merchants never see it as a payment problem, as by the time it registers, it's already churn. For subscription businesses, network tokenization removes this category of failure entirely, and the revenue it protects recurs with every billing cycle.

Unified analytics & observability

Most payment problems go undiagnosed because the data that would explain them is scattered across providers with no common view. A unified analytics layer solves this directly: a single dashboard spanning all payment processors, acquirers, and payment methods, with full visibility into authorization rates, decline reason codes, cost-per-transaction, and chargeback rates - segmented by PSP, region, card type, and BIN range.

With that visibility in place, the problems that were previously invisible become actionable.

The top 3 payment orchestration providers

The orchestration market has matured quickly. Dedicated platforms now compete alongside PSPs that have built orchestration features into their existing stacks. Here's how the leading options compare.

1. Whop Payments Network

Best for: enterprise businesses, platforms, and marketplaces

Whop Payments Network is a multi-PSP orchestration layer - it does not process payments itself, but dynamically routes each transaction across a network of partner processors to maximize authorization rates. When a payment is declined, automatic retry logic reroutes it through an alternative processor instantly, recovering approximately 6–10% more revenue across transaction volume.

The infrastructure covers 187+ countries, 135+ currencies, and 100+ local payment methods, surfaced automatically at checkout based on the buyer's location. Local acquiring in the US, EU, Canada, Australia, and the UK means transactions from those markets route domestically, improving authorization rates and eliminating cross-border fees for those customers.

For platforms specifically, Whop handles KYC, tax compliance via Numeral, and global payouts. Connected accounts onboard and operate independently, with payment splits, commissions, and refunds managed via API.

See what your failure rate is actually costing you. Read more about Whop Payments Network.

2. Stripe Orchestration

Best for: developer-led teams already on Stripe

Stripe previewed its orchestration product in 2025, allowing merchants to route transactions to third-party processors from within the familiar Stripe interface. The integration requires just a one-line code change for existing Stripe API users, and performance analytics are available across all connected processors.

The product is live but gated: access requires onboarding through a Stripe representative rather than self-serve signup. Merchants who want to route outside Stripe's ecosystem while retaining Stripe as their primary processor will find this a practical entry point. Those looking for full multi-PSP flexibility may find it limiting.

3. Spreedly

Best for: merchants who want full provider flexibility with no PSP lock-in

Spreedly operates as a pure orchestration layer - it does not process payments itself, which means routing decisions are made entirely on performance and cost rather than internal commercial incentives. A centralized vault stores payment credentials once and makes them usable across all connected processors, and the platform's smart routing routes transactions to the right provider at the right time.

For merchants who want maximum flexibility to add, remove, or switch PSPs without rebuilding their payments stack, Spreedly's provider-agnostic model is a strong fit.

What to look for in a payment orchestration platform

By now, you've counted the cost. Now the question is which platform is actually worth the switch.

Start with the connector library: how many processors, acquirers, and payment methods are available out of the box, and how quickly can you add more. The value of orchestration compounds with every processor you can route across, so a platform that requires custom development for each new connection loses the speed advantage that makes it worth using in the first place.

From there, ask hard questions about cascading. There's a critical difference between soft declines (a bank timeout, a temporary hold), and hard declines, which are permanent. Retrying a hard decline doesn't recover the transaction, but it triggers fraud signals that damage your standing with the issuing bank. To avoid this happening, ask specifically how the platform handles each, and what the retry logic looks like in practice.

Finally, look past the headline coverage numbers on global support. A platform quoting 150 countries while offering card-only acceptance in most of them is not the same as genuine local market presence. As Bill Noonan, founder of 4Scale, puts it: "Merchants entering new markets assume cards are king everywhere: they're not. Pairing local payment rails with card acceptance is where you win. The presence of a recognised local method builds the trust that lifts conversion across every payment type at checkout."

Can your business afford to wait?

The merchants already using payment orchestration are recovering revenue they would have lost, and entering markets their competitors are still scoping. Every month on a single PSP is a month of that gap widening.

The math is in your own transaction data, so pull your failure rate and see what you're working with.

Start recovering that revenue today with Whop Payments Network.

Payment orchestration FAQs

1. Does payment orchestration require rebuilding my existing checkout?

Not with most modern orchestration layers. Solutions like Whop Payments Network have ready-to-use checkout links, embedded finance tools, and API keys; so your existing checkout flow stays intact.

2. How does orchestration handle stored customer payment methods?

This is one of the most practically important questions for businesses with existing subscriber bases. A true orchestration layer uses a centralized vault to store payment credentials once, then makes them portable across all connected processors. That means a card saved during checkout can be retried through a different processor if the primary one declines, without asking the customer to re-enter their details.

3. How does routing logic actually decide which processor to use?

Routing decisions are typically based on a combination of factors: the card type and issuing country, the processor's recent performance on similar transactions, transaction value, and cost. More sophisticated layers apply machine learning to refine routing over time as they accumulate data on what works in which corridors. Some platforms also allow merchants to configure custom rules: for example, always routing transactions above a certain value through a preferred processor.

4. What happens to in-flight transactions during a processor outage?

This is the redundancy use case, and it's one of the clearest arguments for orchestration. When a processor goes down or begins degrading, an orchestration layer detects the failure and reroutes transactions automatically - typically in milliseconds. For businesses processing at volume, even a short outage on a single PSP can represent significant lost revenue; orchestration eliminates that single point of failure.

5. Is payment orchestration only relevant above a certain transaction volume?

Volume is a factor, but it's not the only one. Businesses selling internationally often benefit from orchestration earlier than high-volume domestic merchants, because cross-border transactions have structurally lower authorization rates and local acquiring makes a meaningful difference. Similarly, platforms and marketplaces tend to need orchestration infrastructure earlier than single-merchant businesses, because the compliance, routing, and payout complexity scales with the number of connected accounts rather than just transaction count.

Sources

- PYMNTS Intelligence / Nuvei: Fraud Management, False Declines and Improved Profitability Covers: 80%+ of merchants lacking visibility into transaction failures; merchant false decline behavior

- PYMNTS Intelligence / Spreedly: Into the Vault: Optimizing Payments Covers: Transaction failure rates; single-PSP dependency costs

- PYMNTS Intelligence / Nuvei: Cross-Border Sales and the Challenge of Failed Payments Covers: $3.8B cost of failed cross-border payments to U.S. merchants in 2023

- Fiserv Carat: Covers: 6% merchant rejection rate; 2–10% of rejections being legitimate customers

- Stripe: AI Enhancements to Adaptive Acceptance (blog) Covers: $6B in recovered falsely declined transactions in 2024; 60% YoY improvement in retry success rate

- Primer: A Nightmare on E-Street Covers: 69% of consumers abandoning checkout when preferred payment method unavailable; 47% of retailers citing negative customer satisfaction impact from false declines

- Slicker: 2025 Failed-Payment Benchmarks Covers: Up to 12% of card-on-file transactions failing due to card expiration/credential issues