Embedded payments allow platforms to have tighter control over how money moves through their product, increasing revenue and reducing friction at checkout. Learn what embedded payments are, how they work, and what to look for in a partner.

Key takeaways

- Embedded payments turn transactions into a native platform feature that unlocks new revenue streams beyond subscription fees.

- Platforms gain full control over transaction data, user experience, and fund routing by embedding payments instead of integrating third-party providers.

- PayFac-as-a-Service lets platforms offer embedded payments without taking on the regulatory burden of becoming a registered payment facilitator.

The line between software, platforms, and payment rails is starting to blur, with embedded payments part of a much broader shift toward embedded finance.

Platforms are integrating banking, lending, and more directly into their products, managing the transaction flow themselves; from checkout and payment methods to settlement and payouts.

For marketplaces and SaaS, this turns payments into part of your product, not just a backend service. It affects revenue models, compliance scope, and how your platform handles transactions for users.

Switch on embedded payments, and you can monetize transactions, control the payment flow, and keep the entire experience inside your product.

This guide covers the fundamentals of embedding payments. You’ll learn how they work, why platforms embed payments into their product, and what to evaluate when choosing a payments partner.

What are embedded payments, who are they for, and how do they work?

Embedded payments allow marketplaces, SaaS, and platforms to accept and manage online payments directly inside their product.

Basically, embedded payments are primarily used by platforms that facilitate transactions between users. Buyers can pay, sellers can get paid, and both subscriptions and one-off transactions can be processed without leaving the platform.

Rather than each seller or creator running their own payment setup, transactions flow through the platform’s payments system.

That means users don’t need to integrate a separate gateway, open a standalone merchant account, or manage multiple payment providers. Everything happens within the same interface. Under the hood, though, the platform is connected to payment partners that actually move the money.

Most embedded payment systems follow a platform payments model, where the platform connects to payment infrastructure and allows other businesses (often called sub-merchants) to accept payments through it.

Platforms typically implement this model in one of three ways:

- Payment facilitator (PayFac): The platform registers as a PayFac and directly manages merchant onboarding, underwriting, and compliance for the businesses using its payment system.

- PayFac-as-a-Service: A third-party provider supplies the core payment structure, while the platform still offers native payments inside its product.

- Direct acquiring: Some platforms connect directly to acquiring banks and payment processors to run their own payments.

Regardless of which model is used, multiple parties are involved each time a payment occurs.

When a customer makes a payment, the transaction is authorized by the issuing bank, routed through the card network and acquirer, and processed by the payment provider. It’s then settled so the platform can distribute funds to the appropriate seller or business.

Embedded payments hide this complexity.

For users, accepting payments just becomes another feature of the platform they already rely on.

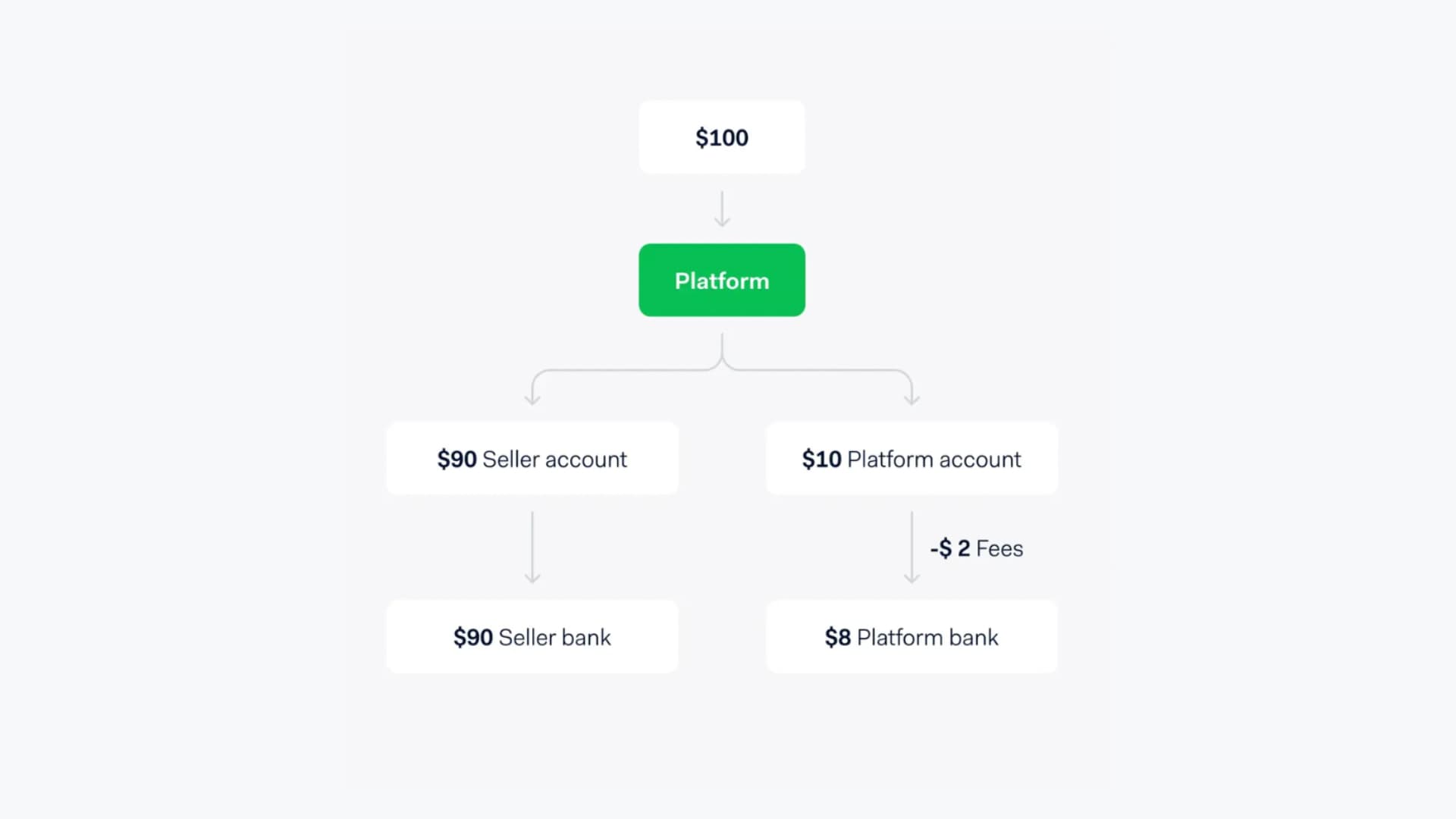

Split payments 101

Most platforms and marketplaces have to split payments between multiple parties. That's called split-routing, and it's how sellers get paid while you ensure revenue is automatically accrued.

Example:

A customer pays $100 on a marketplace.

→ $90 can be routed to the seller

→ $10 goes to the platform as a commission

Embedded payments systems automate this process.

The provider handles fund routing, fee collection, and payouts so the platform doesn’t need to manually move money between accounts. Slick.

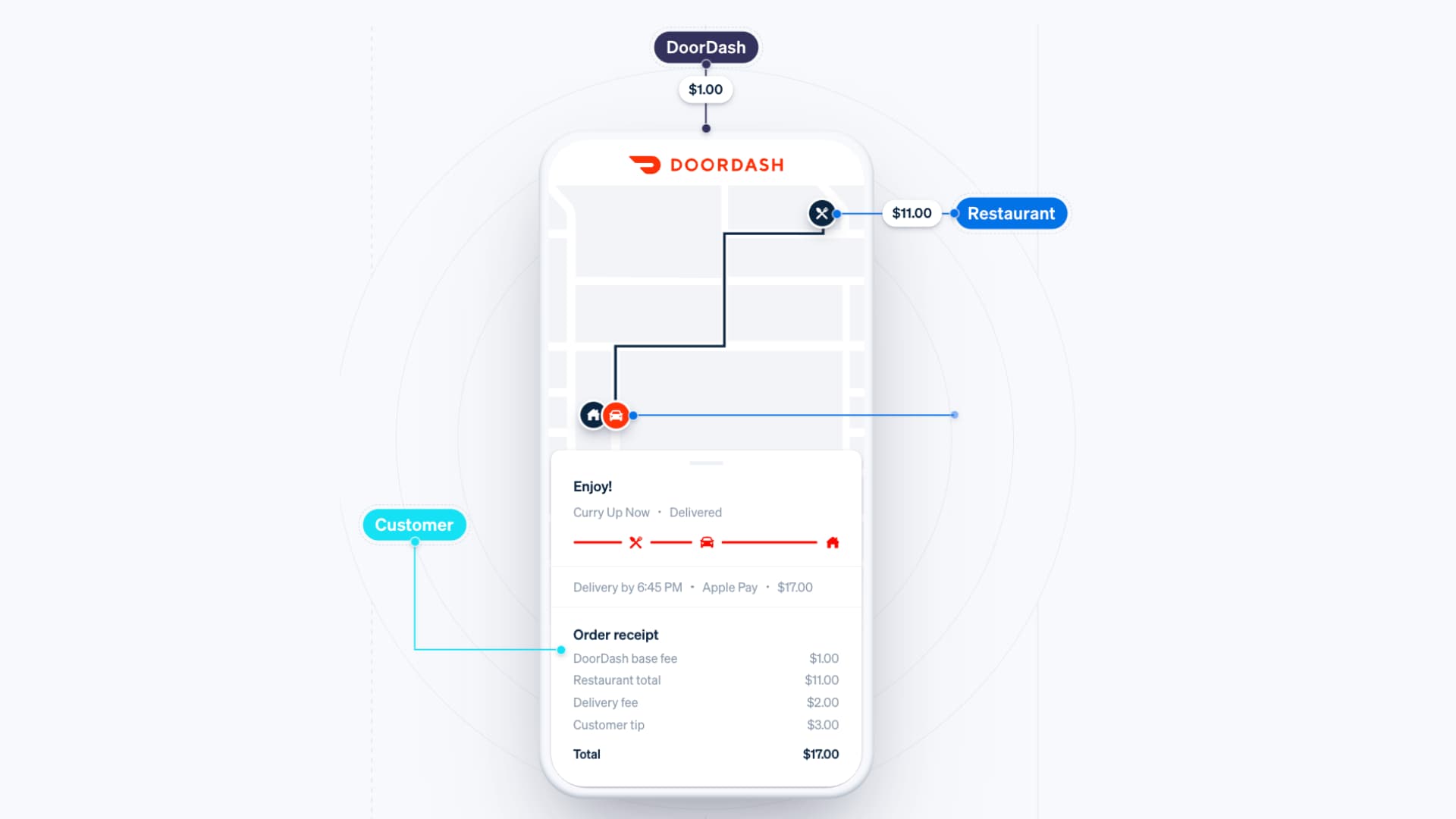

How embedded payments work through Whop

When a business embeds Whop checkout into their own site or product, the payment experience lives inside their own domain - customers complete purchases without being redirected to a separate page or third-party checkout flow.

Under the hood, Whop sits between the seller and the payment infrastructure. Payment processing runs through Whop's bank and payment service provider partners, while Whop manages chargebacks, tax compliance, and payouts.

For the seller, this means no gateway integrations, no merchant account, and no compliance obligations to manage directly. The embedded checkout is the visible surface - Whop's partner network is what powers it.

For more information on embedding checkouts with Whop, check out our documentation.

Payment integration vs. embedded payments: what’s the difference?

Platforms can support payments in two distinctly different ways: by integrating a payment provider, or by embedding payments directly into their product.

At a glance, both approaches allow users to accept payments. So, what’s the difference? It comes down to who controls the experience and where the underlying payment framework lives.

Payment integration

Payment integration is the traditional approach; platforms connect to third-party payment gateways such as standard Stripe or PayPal checkouts, and let users link their own merchant accounts. This means the payment provider owns most of the experience.

Users typically authenticate separately with the payment provider, payments settle into their own external accounts, and the platform acts mainly as a connector between the user and the processor.

The platform may facilitate transactions through its product, but it doesn’t control the full payment flow.

The result? Streamlined ops, but limited visibility into transaction data, less control over onboarding or payouts, and little ability to monetize payment volume.

Embedded payments

Embedded payments move the above structure inside your platform. Instead of each user connecting their own payment provider, the platform operates a unified payments system that sellers, creators, or businesses use directly within the product.

Sub-merchants are onboarded through the platform, payments happen inside the platform interface, and the platform manages how funds move between buyers and sellers.

Because the platform sits directly in the payment flow, it can access full transaction data, control onboarding and payouts, and generate revenue from payment processing.

From the user’s perspective, payments feel like a native feature of the platform rather than a separate integration.

Understanding the PayFac spectrum

Earlier, I briefly explained the difference between PayFac and PayFac-as-a-Service. Let’s dig a little deeper into the responsibilities and outcomes of each.

Embedded payments are usually implemented through a PayFac model, but platforms can take on different levels of responsibility depending on how they structure it.

Full PayFac registration

Platforms can opt for full PayFac registration, where it becomes a registered payment facilitator with the card networks and acquiring banks.

This means the platform itself directly underwrites and manages sub-merchants, takes on compliance obligations such as KYC and anti-money laundering checks, and handles risk monitoring.

You get maximum control, but a whole lot of regulatory and operational complexity alongside it.

One of the first big bottlenecks that you'll see is commonly in that onboarding and KYC delays. As your platform scales, manual underwriting and manual compliance can really slow things down and make for a pretty frustrating experience, both for you and your customers.

– Philip Gorick, Chief Technology Officer at NMI

PayFac-as-a-Service

When platforms choose PayFac-as-a-Service, a payments provider supplies the facilitator systems while the platform embeds payments into its product.

This means it’s the provider that manages licensing, compliance, underwriting, and much of the regulatory overhead. Platforms can still onboard sub-merchants, control the product experience, and earn a share of processing revenue without becoming a regulated payment facilitator themselves.

For SaaS, marketplaces and platforms, this model offers the benefits of embedded payments without the burden of becoming your own registered payment facilitator.

Why do platforms embed payments?

For a lot of platforms, embedded payments start as checkout improvement. But the final impact ends up being much greater.

Payments change how platforms generate revenue, understand their users, and manage transactions between buyers and sellers. So, the most successful platforms are building payments directly into their products.

Shopify generates billions from built-in payment processing alone. Uber, Airbnb, and Etsy all capture a percentage of the transactions flowing through their platforms.

Instead of only charging a monthly user or account fee, embedded payments let platforms participate in the financial activity happening on their network, and make more revenue.

And that's just the beginning.

Generate new revenue streams

Embedded payments allow platforms to earn more revenue directly from the transactions they facilitate:

- Interchange revenue share from card payments

- Margins on processing

- Sub-merchant onboarding or platform fees

- Premium financial features (faster payouts, global payments, advanced reporting, you get the idea)

Think about it: a platform processing $50M annually could scale revenue in a big way just from a small percentage of each transaction. Payment volume grows; revenue does too.

Own your transaction data

When platforms rely entirely on third-party payments, most transaction data lives outside the product. Embedded payments bring that data back inside your own platform.

This provides a first-party view of how money moves through the ecosystem, including purchase frequency, early indicators of churn, average order value, and customer lifetime.

Being able to access accurate data helps platforms build better products, improve their support, and personalize offers. It also enables accurate GMV reporting (critical for investor reporting and fundraising).

Gross Merchandise Value (GMV): The total value of all goods or services sold through a platform over a specific period, before any fees or commissions are deducted.

This sort of transaction data can support new financial products such as lending, underwriting, or insurance.

Reduce checkout friction and increase conversion

This one goes without saying, but sending users to an external checkout page introduces friction.

Customers are redirected away from the product, trust signals disappear, and the purchase experience becomes… fragmented.

As Ciaran O'Malley, Enterprise Commercial Director for Airwallex (UK) explains, "Modern consumers are less likely to wait, as they expect instant and simple-to-use transactions. They have little tolerance for convoluted processes or fragmented user journeys that require several steps to complete a financial task."

With embedded payments, customers can check out using saved payment methods and local payment options, all within a checkout experience that matches the platform’s brand.

Less drop offs, less hesitation, higher conversion.

Manage risk on your own terms

While embedding payments introduces additional responsibilities, it also gives platforms more control over how transactions are monitored and protected.

This can include identity verification during onboarding (KYC/KYB), transaction monitoring, chargeback management, and payout holds that help prevent fraudulent activity before funds leave the system.

Platforms using Whop benefit from these controls through Whop's partner network, without needing to build their own compliance or risk frameworks.

Reduce vendor dependency

When platforms rely entirely on external payment providers, they are continually exposed to policy changes, fee adjustments, or operational issues outside their control.

Embedded payments allow platforms to own the payment experience and the relationships within it. As transaction volume grows, platforms can negotiate directly with acquiring partners, expand payment methods, and introduce additional financial services under their own brand.

How Ohana uses embedded payments to power rent collection

Ohana built a platform where tenants can sublease their apartments and collect rent through one system. Sounds simple, right?

Truth is, there’s a lot to handle. Rent needs to be collected from tenants every month. Landlords need reliable payouts. Identity checks and compliance have to work for both sides of the transaction.

As the official payments network for Ohana, Whop handles pay-ins and payouts within the same platform. Tenants pay, landlords earn, and the entire payment flow runs through a single system.

How to choose the right embedded payments partner

Choosing the wrong embedded payments partner can introduce compliance risk, hidden costs, and poor onboarding experiences for sellers.

As with any core partner, your payments vendor should be evaluated carefully before choosing them for integration.

Follow this guide to ensure you’re getting the best stack possible:

Look for flexibility for your payment flows

Platforms rarely move money simply. You’ll likely require features such as multi-party payouts, revenue splits, and delayed settlement. Maybe you need support for reverse marketplace flows (where the platform pays suppliers).

Your payments provider should support the scenarios you’re dealing with without requiring any major custom work.

"Embedded finance has conditioned users to expect speed, simplicity, and relevance." – Papuna Lezhava, Co-founder and CEO of KEEPZ

If global growth is part of your roadmap, also look for support across international payment methods and cross-border payments.

Calculate the real cost of payments

Advertised processing rates are rarely the full cost. Providers often promote a headline fee, but the true cost of processing usually includes additional charges buried in the pricing structure.

Look for monthly minimums, per-payout fees, foreign exchange margins, reserve requirements, and chargeback fees.

The best way to evaluate pricing is to calculate your expected transaction mix, including average order value, payment methods used, and expected dispute rates. This gives you a more accurate picture of what payments will actually cost as your platform grows.

Demand developer experience

Poor APIs, unreliable webhooks, or weak documentation creates integration issues that limit how your platform evolves over time.

When evaluating providers, assess their API clarity, documentation quality, SDK availability, and webhook reliability.

Check out our guide to using the Whop Rest API to embed checkouts.

Confirm strong compliance

Embedded payments introduce regulatory and security requirements that platforms must manage carefully.

Look for tokenization and hosted payment fields, so your platform isn’t directly handling sensitive card data. If your platform operates internationally, you may need to consider regional regulations.

It’s also important to understand how the provider manages identity verification and compliance obligations such as KYC and/or KYB.

Some platforms must handle these processes themselves, while others rely on providers that offer fully managed onboarding and regulatory frameworks.

Whop provides built-in compliance tools and orchestrates payment workflows so platforms don’t need to build their own compliance stack for things like identity verification or AML processes.

Smooth seller onboarding

If payment setup or identity verification is slow or confusing, sellers may abandon the process before completing onboarding. This directly impacts supply-side growth.

The best embedded payments providers optimize their onboarding flows so sellers can start accepting payments quickly (while still meeting compliance requirements).

Top embedded payments providers for platforms, SaaS and marketplaces

If you want to embed payments directly into your platform, you'll need a provider that supports multi-party payment flows and seller onboarding.

Here are the top choices for platforms and marketplaces looking to embed payments - from PayFac infrastructure providers to full-service technology platforms.

Whop Payments Network

Whop Payments Network is built for internet marketplaces, SaaS platforms, and creator ecosystems.

Businesses get access to payment tools through Whop's partner network - including checkout links, embedded checkout, and global payouts without needing to build or manage a payments stack themselves. Whop acts as the Merchant of Record, taking on chargebacks, tax compliance, and regulatory obligations so businesses can focus on growth.

Stripe Connect

Stripe Connect is Stripe's embedded payments product, aimed toward SaaS platforms, marketplaces, and gig-economy products that want deep developer control over payment flows.

Stripe provides APIs that let platforms build their own onboarding, payout logic, and payment experiences around Stripe’s infrastructure, making Stripe Connect popular with dev-friendly companies. However, it often means platforms often need to build more of the payments experience themselves.

Adyen for Platforms

Adyen for Platforms is Adyen's embedded solution for platforms and marketplaces. Businesses can onboard sellers or service providers, accept payments on their behalf, and control when and how funds are paid out.

Adyen merges processing, acquiring, risk monitoring, and compliance into a single system, making it a popular choice with large international platforms looking for enterprise-grade tools.

Mollie Connect

Mollie also offers a payments product built for SaaS platforms and online marketplaces called Mollie Connect.

Through its APIs and hosted onboarding, platforms can sign on merchants, process payments on their behalf, and distribute funds using split payments or allocation fees.

Mollie also manages KYC verification, compliance, and payouts behind the scenes, so platforms can easily embed payments without running their own ops.

Platforms using Mollie must generally be registered in the European Economic Area (EEA), the United Kingdom, or Switzerland.

Bolt Connect

Bolt Connect powers embedded checkout and marketplace payments through Bolt's commerce network.

It's heavily focused on checkout conversion, combining a one-click checkout network, payment processing, and seller management tools into a single stack.

Marketplaces can onboard sellers with compliance checks and automatically route payments and payouts.

Get started with Whop Payments Network

Once payments run through your platform, you have the foundation to build additional financial features over time, from faster payouts and revenue insights to more advanced tools.

Platforms like Ohana use Whop Payments Network to power their payments. Rent flows in from tenants, payouts flow out to landlords, and compliance is managed through Whop's partner network.

This model is key for platforms processing meaningful transaction volume, that want payments to move beyond a checkout feature and become a real part of their revenue model.

Whop provides the tools to make that possible.

Instead of building payment acceptance, compliance tooling, and payout systems from scratch, platforms can access all of it through Whop Payments Network.

Access embedded payments, global payouts, and more through Whop Payments Network.