Both integrated and embedded payments allow platforms to accept transactions and move money through their network, but embedded payments offer opportunity for revenue growth and custom control.

Key takeaways

- Embedded payments transform transactions from basic infrastructure into a scalable revenue stream for growing platforms.

- Platforms using embedded payments gain full control over checkout, onboarding, payouts, and transaction fee monetization.

- PayFac-as-a-Service and Merchant of Record models let platforms embed payments without building complex compliance infrastructure themselves.

For platforms, SaaS products, and online marketplaces, payments can become more than infrastructure. They can be a main revenue driver, allowing companies to gain control over (and profit from) financial activity within the product.

That's why we're seeing a big shift from integrated payments toward embedded payments, where transactions happen directly within the platform.

Embedded finance transaction volume is projected to exceed $7 trillion in the US alone by 2026. That's because how users pay and how sellers get paid directly affects platform growth, retention, and revenue.

In this guide, I'll break down how both integrated payments and embedded payments work, how platforms can monetize payments, and which approach makes sense for your product.

What are integrated payments?

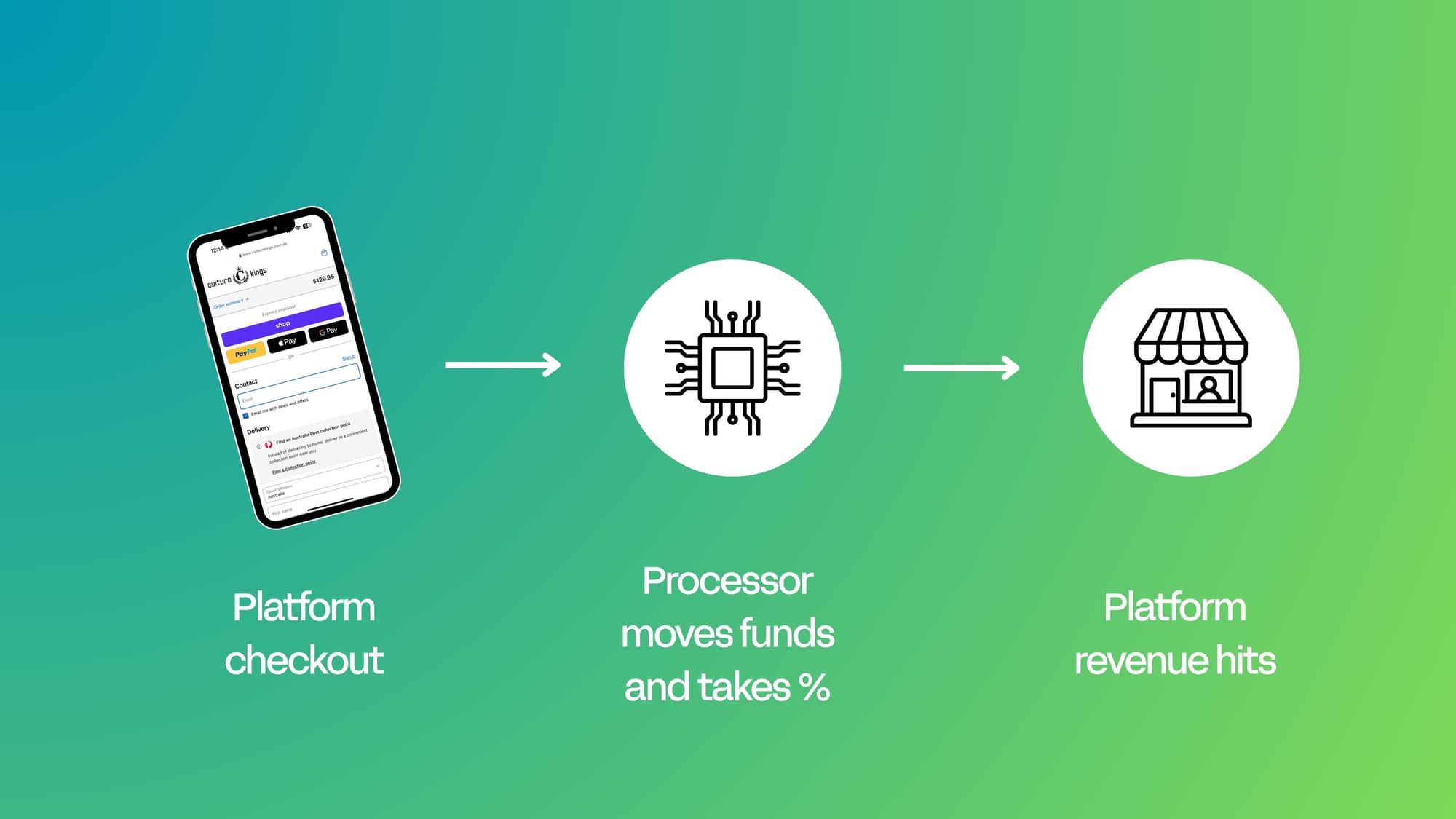

Integrated payments simply connect a payment processor directly to your platform or software through a payment API, plugin, or pre-built integration. Your product then connects to a third-party provider that handles the core payment processing.

Common integrated payment providers include Stripe, Square, and Worldpay, which offer APIs that allow software products to connect checkout flows to external payment infrastructure.

When a customer makes a purchase, the transaction moves through the processor’s acquiring banks and card networks, and the processor typically manages merchant onboarding, compliance, settlement, and much of the payment experience.

For startup SaaS companies and early-stage platforms, integrated payments can be the fastest way to start making money. Connect to a payment processor’s API, add your checkout functionality, and begin processing payments.

But there’s a trade-off: The payment provider owns most of the checkout experience, and most of the potential revenue.

And that's not the only con.

Pros and cons of integrated payments

| Pros | Cons |

|---|---|

| Fast to implement (often within days or weeks) | Limited control over the payment experience |

| Lower technical complexity | Revenue typically shared with the provider |

| Built-in compliance and risk management | Merchant onboarding controlled by processor |

| Access to established payment infrastructure | Harder to customize pricing and flows |

| Reliable support and documentation | Platform captures less value from transactions |

The larger your platform's user base gets, the more revenue you're missing out on.

Embedded payments flip that on its head, giving your platform a way to increase revenue simply from transactions flowing through your product.

Let's go deeper.

What are embedded payments?

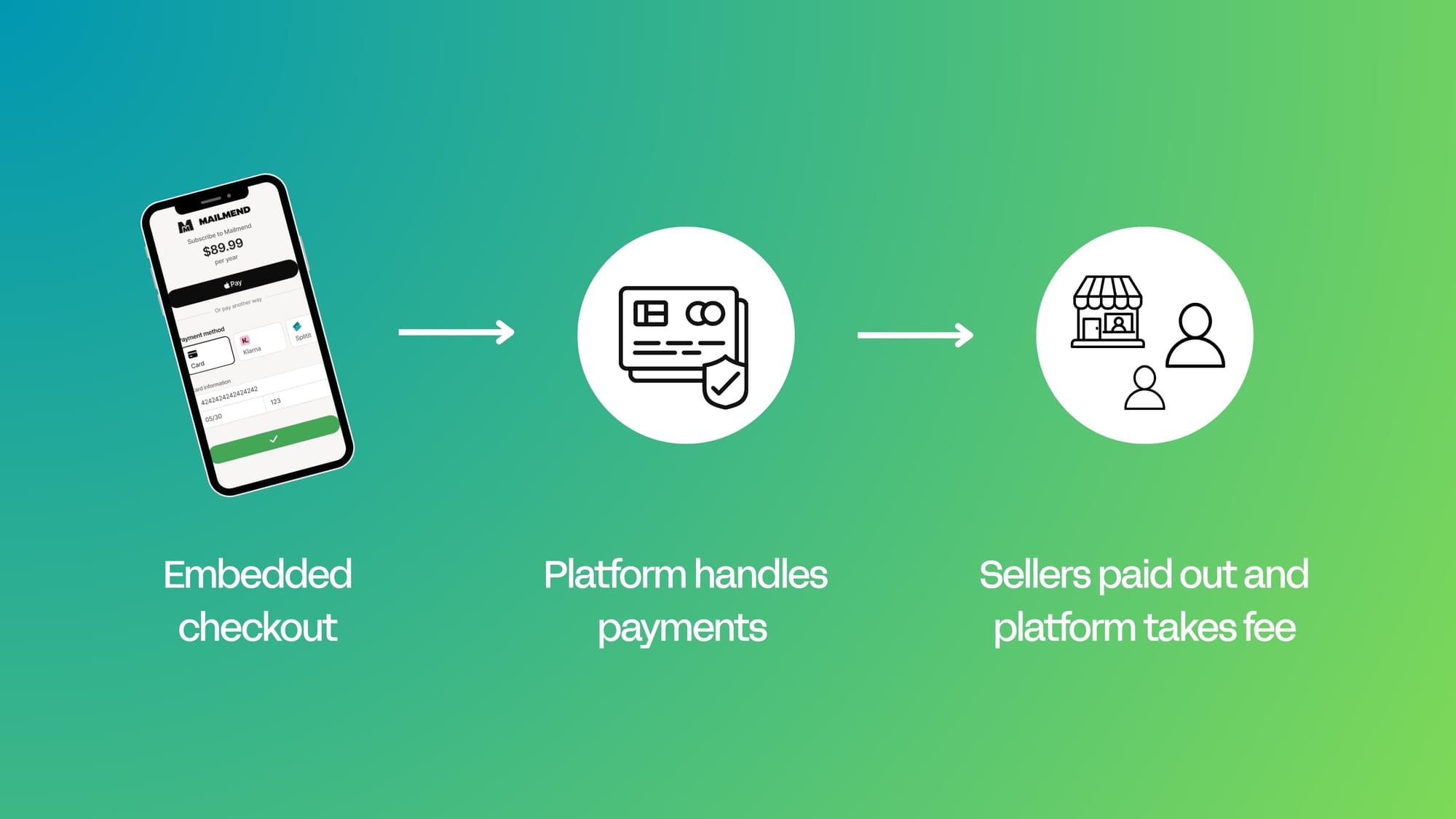

Embedded payments take things a step further than simple integrations. Instead of connecting to an external processor, payments become a built-in part of your platform.

That means your sellers can onboard, accept payments, and receive payouts directly inside the platform.

Think about platforms like Uber or Airbnb. Riders and guests pay through the app, and individual merchants aren’t connecting their own payment providers.

You can design your own onboarding flows, control pricing and transaction fees, manage payouts, and build a payment experience that fits your product.

But (arguably most importantly), embedded payments also create a new revenue stream. A recent industry survey found over 90% of independent software vendors (ISVs) expect embedded payments to significantly increase platform revenue.

Mindbody makes more than half their revenue from embedded finance products, FYI. So yeah, the opportunity is huge.

Angela Strange, General Partner at a16z, believes the revenue boost platforms see from embedded finance will become a no-brainer. "In the not-too-distant future, I believe nearly every company will derive a significant portion of its revenue from financial services."

TL;DR: Instead of just moving money, embedded payments let you capture a share of fees from financial activity happening on your network.

Embedded pay-ins vs. embedded payouts

When we think about payments, we're often thinking about checkout (i.e., pay-ins).

Pay-in features include customer payment methods, currency handling, subscriptions, and recurring billing all happening natively in-platform.

But platforms also need to split funds between multiple parties, route payouts to different sellers, schedule disbursements, and support instant withdrawals.

When both pay-ins and payouts are embedded, platforms get full control over the flow of money across the ecosystem. That means smarter fraud monitoring, more flexible pricing models, and additional embedded finance features (like instant payouts or seller advances, which you can charge for, too).

Pros and cons of embedded payments

| Pros | Cons |

|---|---|

| Full control over the payment and checkout experience | More complex to implement than simple integrations |

| Ability to capture revenue from transaction volume | Additional compliance responsibilities (KYC, AML, risk monitoring) |

| Control over merchant onboarding and payouts | Longer implementation timeline |

| Access to full transaction data within the platform | Requires payments infrastructure or a PayFac provider |

| Stronger platform stickiness and monetization opportunities | More operational oversight of payment flows |

How do embedded payments work?

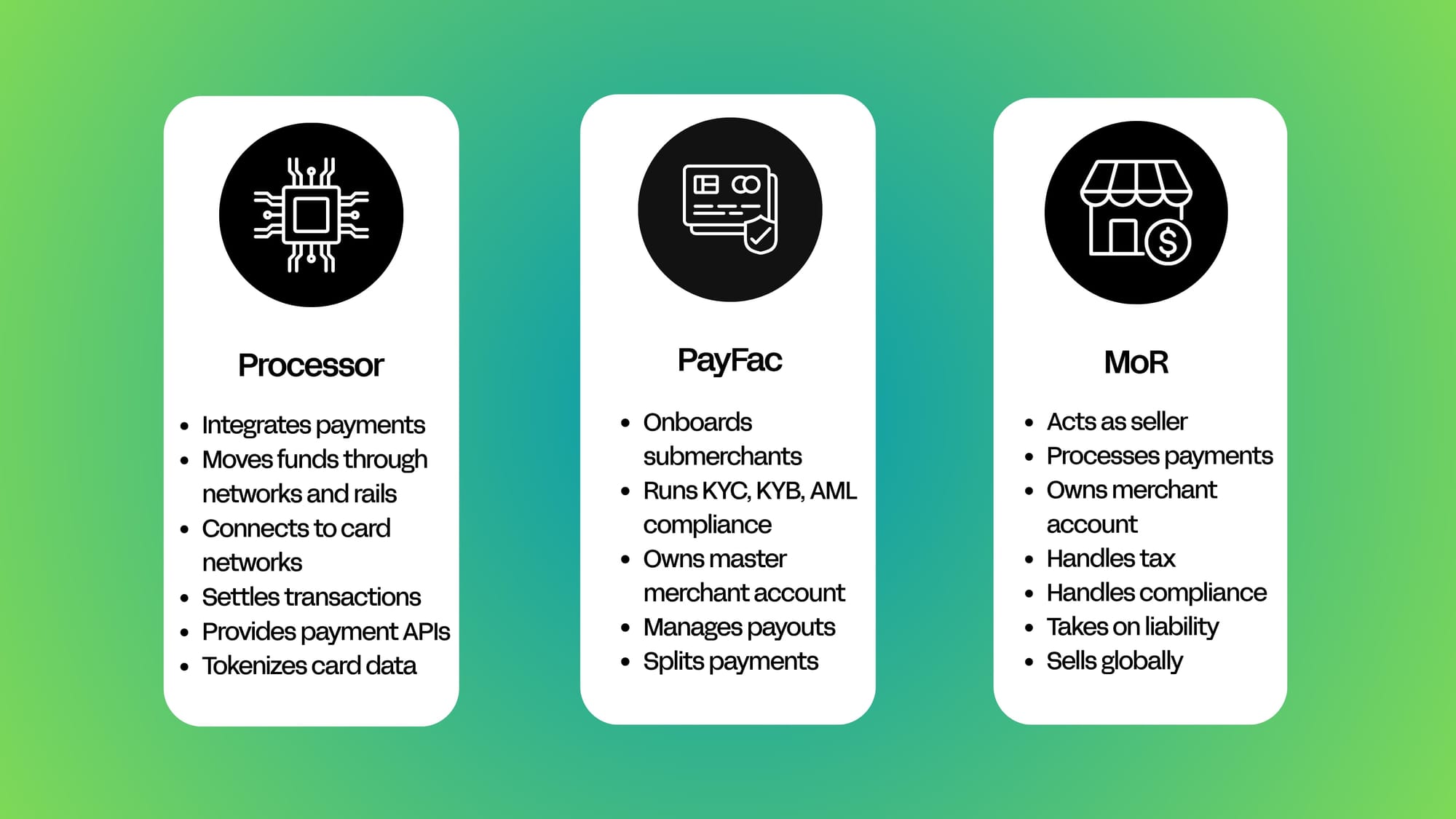

Embedded finance tools (like payments) are possible for platforms through what's called a Payment Facilitator (PayFac) or Merchant of Record (MoR).

Let's run through how each model operates, especially from a platform's POV.

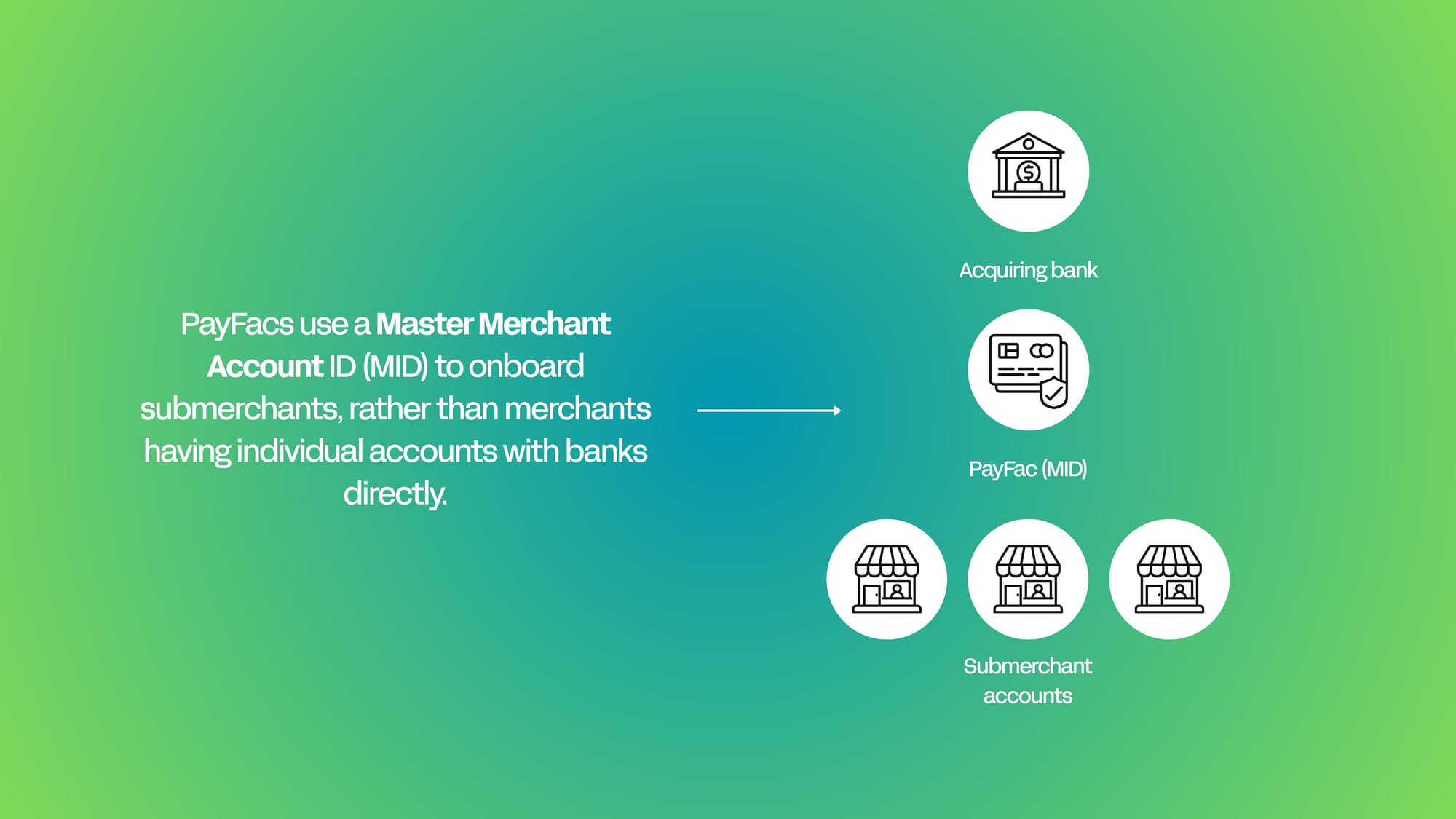

PayFacs

A Payment Facilitator (PayFac) allows a platform to onboard sellers as sub-merchants under a master merchant account, instead of requiring every seller to open their own merchant account with a bank.

This is why onboarding can happen in minutes instead of days.

Sellers start accepting payments through the platform almost immediately, while the PayFac manages the infrastructure connecting the platform to payment processors and acquiring banks.

But becoming a registered PayFac comes with serious responsibilities.

You'd have to handle your own identity verification (KYC/KYB), underwriting, transaction monitoring, and ongoing compliance with card network rules.

PayFac-as-a-Service

That sounds like a headache, am I right? It's that complexity that drives platforms to choose a PayFac-as-a-Service (PFaaS) instead.

With PFaaS, a payments provider supplies the facilitator infrastructure while the platform embeds payments directly into its product.

The provider looks after the annoying parts: licensing, compliance frameworks, and risk systems. Your platform still controls the user experience and transaction flow, though.

This means you can embed payments, onboard sellers quickly, and monetize transactions without building a full payments operation yourself.

Mastercard's white paper found that using a PFaaS can reduce time to market from months to weeks, if not less (compared to platforms becoming their own PayFac).

Merchant of Record (MoR): One step beyond a PayFac

A Merchant of Record (MoR) model goes a step further than a PayFac. The MoR becomes the legal seller for the transaction, handling payment processing, tax calculation and remittance, chargebacks, fraud monitoring, and regulatory compliance.

For platforms, this removes a huge amount of operational overhead.

You can still embed payments directly into your product, onboard sellers, and route payouts across your platform. But the MoR manages the regulatory and financial side of the transaction behind the scenes.

When you sell on Whop or through Whop Payments, Whop acts as Merchant of Record for the purpose of card network rules and payment settlement only.

Integrated vs embedded payments: A side-by-side comparison

Both integrated and embedded payments allow you to accept transactions inside your product, but the difference is between who controls the experience and who captures the value from payment flows.

But if you're running your own marketplace, SaaS, or user platform? You most likely care about revenue potential, control, and compliance.

While it's true that integrated payments offer the fastest path to accepting payments, it doesn't mean it's necessarily what's best for platforms long-term.

Here's how the two options stack up with those concerns in mind:

| Feature | Integrated payments | Embedded payments |

|---|---|---|

| Control | Provider controls most flows | Platform controls checkout & payouts |

| Revenue | Processor keeps most fees | Platform captures transaction share |

| Implementation | Fast to launch | More setup required |

| Onboarding | Handled by processor | Handled by platform |

| Compliance | Mostly provider responsibility | Shared or platform responsibility |

| User experience | External or provider-branded flows | Native platform checkout |

Integrated payments are ideal for early-stage platforms prioritizing speed. Embedded payments make more sense when payments become a core part of the platform’s business model.

Richie Serna, Co-Founder of Finix, says the biggest payments companies of the next decade will be software platforms that monetize payments within their products:

"The next generation of billion-dollar payments companies won’t look like Stripe or Square. Instead, they’ll be vertically specific software companies who monetize payments.”

Platforms that integrate financial services are valued about 23% higher on average, according to investment firm William Blair.

How to choose between integrated and embedded payments

Integrated payments may be the better choice if your platform:

- Needs to launch payments quickly

- Has limited engineering resources

- Doesn't want to make revenue from payments (interesting call)

Embedded payments may make more sense if your platform:

- Processes large transaction volumes

- Wants to monetize payments

- Needs full control over checkout, onboarding, and payouts

- Is building a marketplace, creator platform, or SaaS ecosystem

And remember, embedded payments don't necessarily take weeks with modern providers. Whop provides a simple, out-the-box, full-stack payments solution for platforms, SaaS, and marketplaces with embedded finance built in.

Why platforms are moving from integrated payments to embedded payments and finance

For years, the goal with platform payments was simple: connect a processor, enable transactions, and move on.

But as platforms scale, integrated payments start to leave a lot of cash on the table.

When marketplaces, SaaS platforms, and creator ecosystems process large volumes of transactions? Payments become one of the most scalable revenue opportunities you have.

So, instead of relying purely on subscriptions or platform fees, companies can capture a small share of all the financial activity happening across their network.

Over 60% of vertical SaaS platforms have embedded payments into their products, increasing both revenue and platform stickiness (when vendors rely on you to get paid, access funds, or manage money, switching becomes much harder).

Payments revenue scales directly with platform activity. As more buyers and sellers transact through the product, financial services revenue grows automatically alongside it.

Case study: Ohana uses Whop for embedded payments

Ohana built a platform for tenants to sublease their apartments and collect rent through a single system.

In reality, that's a lot going on behind the scenes: rent has to be collected from tenants each month, landlords need reliable payouts, and identity checks and compliance have to work smoothly for both sides of the transaction.

With payments embedded directly into the platform, Ohana's entire payment flow happens inside the product. Tenants pay rent, landlords receive payouts, and everything (onboarding, payments, and payouts) runs through a single system.

Embed payments and boost your platform's revenue with Whop

Integrated payments help platforms start accepting transactions quickly. But as platforms grow, payments usually evolve to become a core part of the product itself.

By merging checkout, onboarding, and payouts directly into the platform experience, you gain more control over how transactions happen and how you can monetize them.

Whop makes it simple, with an MoR-backed payments stack built for platforms, SaaS products, and marketplaces. Embed payments, orchestrate payments, onboard sellers, and route payouts inside your product without building any infrastructure yourself.

Accept buyer payments, pay out sellers instantly, and handle compliance automatically with Whop.

Integrated vs. embedded payments FAQs

Is embedding payments the same as becoming a PayFac?

No, embedding payments just means payments are built directly into your platform’s user experience. Some platforms do this by becoming a payment facilitator (PayFac), but many use PayFac-as-a-Service or a Merchant of Record (MoR) provider instead.

These models let you embed payments without taking on the full regulatory and operational burden yourself.

Can I start with integrated payments and switch later?

Yes, lots of platforms start with integrated payments because they’re quick to launch. As the product grows, switching to embedded payments can provide more control over the checkout experience and allow the platform to capture a share of payment revenue.

What are the biggest compliance risks with embedded payments?

The main risks include KYC and merchant onboarding requirements, fraud and chargeback management, tax compliance, and card network rules. Platforms that operate their own PayFac model are responsible for these obligations.