Embedded finance can uplift platform revenue by 2–5x. Here's how the top providers compare in 2026, and how to determine which fit your platform's needs.

Key takeaways

- Embedded finance lets platforms monetize every transaction flowing through them, boosting revenue 2–5x over subscriptions alone.

- A single dollar generates revenue multiple times—at checkout, during holding, at payout, and through lending or card spend.

- Platforms with embedded financial tools reduce churn by up to 64% because users depend on them to manage money.

In 2024, the total market value of embedded finance sat at $185 billion USD. By 2034, it’s projected to grow at a CAGR of 31.53%.

That kind of growth isn’t happening by accident. SaaS platforms and marketplaces are rolling out embedded finance fast, driven by benefits like higher revenue (average uplifts of 2–5x), more control over their user experience, and the ability to offer financial services natively.

So what do these benefits actually look like in practice? Who are the top embedded finance providers in 2026? And more importantly, do their products fit your platform’s needs?

Let’s find out.

By the end of this article, you’ll walk away knowing exactly which embedded finance provider to choose.

What is embedded finance?

Embedded finance is the integration of financial services (like payments, financing, or banking) directly into non-financial platforms.

So, instead of sending users to a bank or third-party provider, the platform itself offers these services natively within its own product or checkout flow.

Paying with Apple Pay at checkout? That’s embedded finance. Uber drivers accessing earnings instantly in-app? Embedded finance. Even Amazon offering Buy Now, Pay Later – you guessed it.

With embedded finance, the financial service or product is built into the experience, not bolted on after.

This is what separates embedded finance from traditional banking partnerships.

In the past, platforms would redirect users to external financial institutions to complete transactions. Now, the experience can stay entirely on-platform, giving businesses more control over the user journey, data, and revenue.

Under the hood, it’s all powered by APIs that connect platforms to regulated financial infrastructure. Meanwhile, users just get a seamless experience within one platform.

Hang on... Is embedded finance the same as BaaS?

Not quite. In many cases, embedded finance infrastructure is provided by Banking-as-a-Service (BaaS) providers, which handle compliance, licensing, and fund movement behind the scenes. This means platforms can offer financial products without becoming banks themselves.

But not every embedded finance provider is a BaaS solution.

Some providers (like Whop) sit at the product layer. Payments, monetization, and financial tools are packaged together into one platform, using underlying partners for the regulated infrastructure.

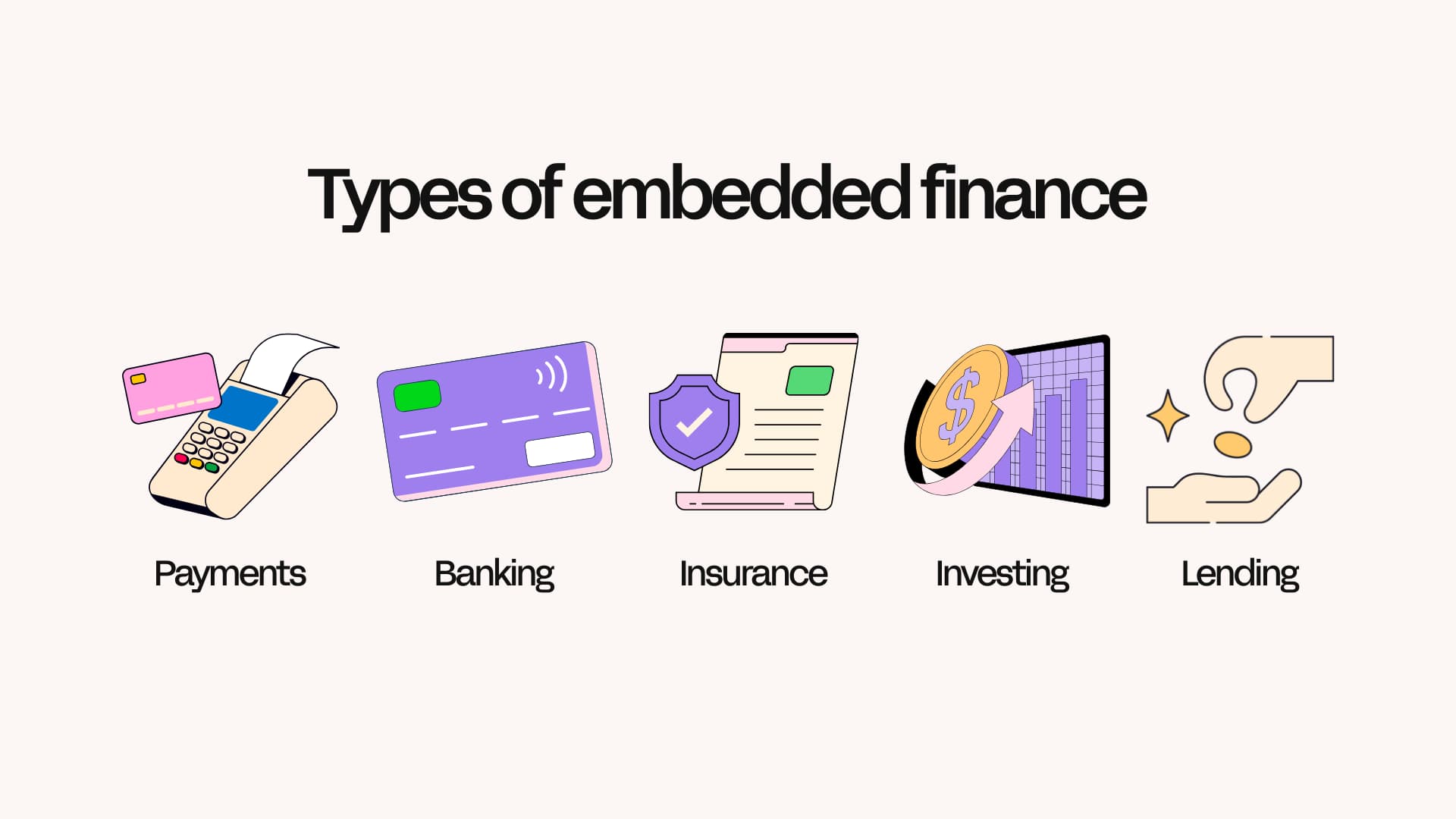

Types of embedded finance

Embedded finance isn't a product; it's a category. Most platforms implement one (or more) of the following types of embedded finance products, depending on how they want to monetize and serve their users.

Embedded payments

Embedded payments are the most common use of embedded finance, where platforms process and accept payments directly within their ecosystem. The entire checkout experience happens natively, instead of sending users to a third-party gateway or external browser.

Example: Shopify Checkout or Apple pay integrated into apps. Embedded payments allow users to pay without leaving the platform.

Embedded banking

Embedded banking gives users access to financial accounts and banking services like cards, wallets, or stored balances directly in a platform.

This can include holding funds, managing balances, earning yield, and accessing payouts.

These experiences can be powered by traditional BaaS providers, but increasingly also by alternative infrastructure, like payment networks or block-chain based systems. Looks like even embedded banking is moving away from centralization.

Example: Stripe Financial Accounts, which lets businesses hold, send, and manage money directly within Stripe.

Embedded lending

Embedded lending includes offering credit, advances, or BNPL financing options to users within an embedded checkout flow.

This allows platforms to finance users or businesses directly, often based on activity and revenue data.

Example: Shopify Capital, which provides merchants with funding, or Whop Payments, which allows platforms and businesses to offer financing through multiple providers under one roof.

Embedded insurance

Embedded insurance allows platforms to offer insurance products when users need coverage. This could be anything from travel insurance at checkout to protection for fragile goods during shipping and handling.

Example: Booking.com offers travel insurance directly through their checkout flow.

Embedded investing

Some platforms also enable users to invest directly within their system, removing the need to use a separate brokerage. This could include stocks, crypto, or managed portfolios.

Example: Cash App, where users can buy stocks or Bitcoin directly within the app. Or Acorns, which uses embedded investing features to automatically round up purchases and invest on a user's behalf.

Why platform builders are embedding finance now

Embedded finance isn’t just a trend, but an advanced way for software platforms and marketplaces to increase profit.

You can think of it in three waves: SaaS 1.0, 2.0, and 3.0.

- SaaS 1.0 was subscriptions: Software moved to the cloud, and companies charged subscription fees for usage. Simple.

- SaaS 2.0 added data, collaboration, and integrations: Products became more interactive, supported real-time workflows, and increasingly embedded payments to monetize activity happening on-platform.

- Now, we’re in SaaS 3.0: Typically defined by AI and deep customization. Platforms are becoming more intelligent, modular, and tailored to each user (and so are their financial capabilities).

I mentioned earlier that introducing embedded finance can uplift platform revenue by 2–5x, through unlocking new streams like payment fees, lending margins, and float on held funds.

That's because instead of charging users once, platforms can now monetize every single transaction that flows through them. In turn? Embedded finance makes your platform significantly stickier.

When your users rely on your platform not just to operate, but to get paid, access funds, or manage money? Switching becomes much harder.

Platforms with embedded financial tools have been shown to reduce churn by up to 64%. That’s huge.

Even at its most basic level, the logic is simple. Money is already moving through your platform, why let someone else capture that value?

Real world examples of embedded finance

Take Mindbody, for example. They started as a booking SaaS for fitness and wellness, and evolved into a platform that monetizes payments, lending, and financial services.

Today? More than half of their total revenue comes from embedded financial products.

Or, check out AI-powered subleasing platform Ohana, which recently partnered with Whop to embed payments into their platform, helping people earn $1B/yr subleasing.

That’s a lot of revenue flowing through their platform, and a no-brainer to capitalize on.

How do platforms make money from embedded finance?

Most platforms are already sitting on top of financial activity, they just don’t monetize it properly.

If your users are transacting, getting paid, holding balances, or moving money through your product, there’s already revenue there. Embedded finance is what lets you capture it.

The shift is simple: instead of charging for access (subscriptions), you start monetizing what users do with money inside your platform.

This is why embedded finance becoming standard for marketplaces and SaaS is pretty much inevitable. If you’re already facilitating transactions, not owning that layer means you’re leaving a lot of revenue on the table (or handing it over to payment processors, banks, and third-party providers).

By embedding your own financial capabilities, products, and services, you can make money in different ways.

| Revenue stream | How it works | Example |

Transaction take rate |

You take a cut every time money moves. This is the foundation, and it compounds fast with volume. |

Marketplace takes 5% on every sale |

Interchange (card spend) |

Issue cards and earn whenever users spend, even off-platform. Extends monetization beyond your product. |

Platform-issued debit card used for everyday purchases |

Float / yield on balances |

User balances don’t just sit there, they can generate yield. At scale, this becomes a major revenue driver. |

Holding funds that earn yield before payout |

Lending & advances |

Offer capital and earn through fees or interest. Your data gives you an underwriting advantage traditional lenders don’t have. |

Shopify Capital funding merchants |

Financial tooling (SaaS layer) |

Charge for premium financial features like instant payouts, treasury, analytics. Adds a second monetization layer. |

Charging for instant withdrawals |

These revenue streams don’t operate in isolation either, they stack.

The same dollar can generate revenue multiple times: when it’s paid, when it’s held, when it’s spent, and when it’s borrowed against.

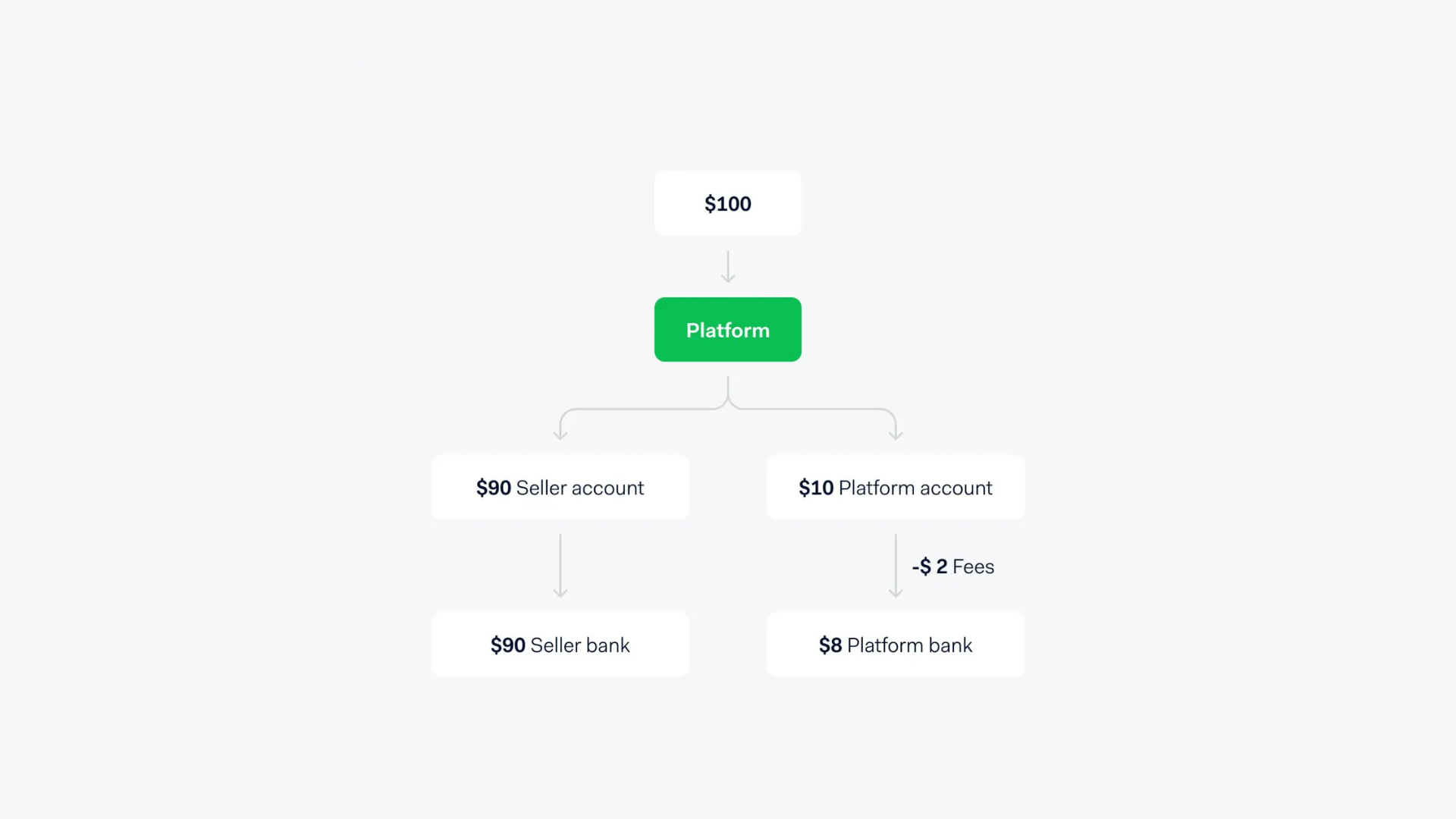

Example: how $100 flows through a platform

Let’s say a customer spends $100 on your platform. Like I said above, that same $100 can generate revenue multiple times, not just at checkout.

- At checkout: You take a cut of the transaction (e.g. $5)

- Before payout: The money sits in your system briefly and can generate yield

- At payout: Users may pay for faster withdrawals

- After payout: If users spend via your card, you earn interchange

- Later on: You can offer loans or advances based on their activity

Instead of just monetizing the transaction, you’re monetizing the payment, balance, payout, and the reuse of funds.

Top embedded finance platforms for 2026

Not all embedded finance providers are built for the same things.

Some are raw infrastructure (BaaS), while some focus on payment acceptance. Others might specialize in lending (like BNPL providers), or company card issuing.

Others provide a full-stack of embedded finance products under one hood, like Stripe, Airwallex, and Whop.

“SaaS companies are increasingly seeking partners that are more consultative in nature, ones that can really understand unique user flows and ensure the financial experiences match the desired user experience.”

— Matt Downs, President, Worldpay for Platforms

When you're embedding finance into a marketplace or SaaS, your provider determines how much of the financial stack you can actually monetize on.

Here are the top embedded finance platforms and providers for 2026.

Quick embedded finance platform comparison

| Platform | Type | Best for | Global? | Pricing model |

|---|---|---|---|---|

| Whop | Full-stack (orchestration layer) | Platforms wanting end-to-end monetization + embedded finance without building | Yes | Revenue share + processing fees |

| Stripe | Payments infrastructure | SaaS + marketplaces needing flexibility and control | Yes | Per-transaction + add-on product fees |

| Adyen for Platforms | Enterprise payments infrastructure | Large platforms optimizing global payment performance | Yes | Custom enterprise pricing (volume-based) |

| Marqeta | Card issuing infrastructure | Platforms building card-based spend or payout experiences | Yes | Usage-based (per card, transaction, program) |

| Unit | BaaS + managed layer | SaaS embedding accounts, cards, and banking features | Primarily US | Usage-based + partner banking fees |

| Airwallex | Global payments + FX infrastructure | Platforms managing cross-border payments and multi-currency flows | Yes | FX margin + transaction fees |

| Plaid | Data infrastructure | Apps needing bank connectivity and financial data | US + limited global | Per API call / per connected account |

| OpenPayd | BaaS + payments + FX | Platforms handling global money movement + crypto flows | Primarily EU/UK | Usage-based + FX + transaction fees |

| Parafin | Embedded lending + spend | Platforms monetizing via seller financing | Primarily US | Revenue share on loans / financing |

| Affirm | BNPL / consumer lending | Platforms boosting checkout conversion | US + select markets | Merchant fee per transaction |

The above table gives a quick side-by-side comparison. Full breakdowns of each provider's capabilities below.

Whop

Best for: Creator platforms, marketplaces, and SaaS that want end-to-end embedded finance without building it themselves.

Whop isn't a PSP, BaaS provider, or PayFac. It's a tech platform that gives you access to payments, payouts, financing, and other embedded finance products and tools through a trusted network of partners.

This means (unlike with infrastructure-first platforms), you don't start with raw building blocks and figure it out yourself. Instead, you get a fully workable stack right out of the box (which you can layer custom logic on top of, via APIs, SDKs, and integrations – if you want to).

If your platform cares about strong monetization, security, and flexibility? Whop lets you get embedded finance up and running faster.

Under the hood, Whop partners with providers like Stripe, Adyen, Klarna, Affirm, and more. It doesn't process payments or hold funds itself; it routes transactions through partner networks, retrying failed payments across providers.

Authorization rates? Up. Lost revenue? Recovered.

On top of that, you get a built-in distribution funnel (marketplace), affiliates, subscriptions, MoR, and billing tools.

When we say full-stack, we mean it.

Stripe

Best for: SaaS and marketplaces that want flexibility and control.

Stripe gives you everything at the infrastructure level: payments, marketplace tooling (via Stripe Connect), subscriptions, card issuing (via Stripe Issuing), tax (via Stripe Tax), and more.

But Stripe isn’t a finished, full-stack product; it’s a toolkit. You’ll need to build your own flows, manage edge cases, and optimize performance yourself.

That’s fine if you have engineering resources, but it sure adds complexity fast. Plus, at a large scale? You’re managing multiple Stripe products, fees, and systems.

Adyen for Platforms

Best for: Large companies optimizing payment performance across markets.

Adyen supports online, in-app, and in-person transactions, along with additional marketplace, SaaS, and platform capabilities through Adyen for Platforms.

This includes onboarding users, handling compliance and verification, processing payments on behalf of sellers, splitting transactions, and managing payouts within a single system.

Adyen’s network supports a wide range of currencies and local payment methods, which makes it particularly handy for companies operating internationally or expanding into new markets. It also offers tools for risk management, reporting, and reconciliation

However, implementation is pretty hands-on, so Adyen is generally better suited to companies with existing scale (rather than those looking to launch quickly).

Marqeta

Best for: Platforms adding card-based spend or payout experiences.

Marqeta is an embedded finance provider focused on card issuing, enabling platforms to create and manage virtual and physical cards for their users.

So, instead of pushing money out to a bank account, platforms can keep funds inside their ecosystem and let users spend directly via a card.

Platforms can decide how and when funds are available, set spending limits, restrict purchases, and tie transactions directly to a user’s balance in real time.

Marqueta typically sits alongside payment processors and other embedded finance providers in a wider stack.

Unit

Best for: SaaS platforms embedding accounts, cards, and financial features.

Unit is an embedded finance platform combining BaaS infrastructure with a managed product layer.

Platforms can launch accounts, cards, payments, and capital quickly using Unit’s pre-built setup, or drop down into APIs to build fully custom financial flows.

Unit provides direct access to core financial systems including ledgering, payment rails, and multi-bank architecture for companies that want to run more complex programs.

It doesn’t provide loans itself, but integrates underwriting, funding, and servicing into a single platform, making it easier to embed banking-style products.

Airwallex

Best for: Marketplaces and SaaS that need global payments, FX, and financial operations at large.

Airwallex is a global payments and financial infrastructure provider that platforms use to accept payments, move money internationally, and manage multi-currency payouts.

Through APIs, platforms can onboard users, process payments, split funds, and handle global payouts, with Airwallex providing the underlying rails, licensing, and compliance.

However, Airwallex is still infrastructure. It handles payments and money movement, but it doesn’t give you a built-in product or revenue model. You still need to decide how you charge users and integrate those flows into your platform.

Plaid

Best for: SaaS and fintech products that need access to user financial data.

Plaid is an embedded finance platform focused on secure bank connectivity and financial data access, not payments or money movement.

For SaaS and platforms, (including with clients like Robinhood, Venom, and Chime), Plaid is typically used at the data layer. It powers things like onboarding (link your bank), income verification, spending insights, and ACH payments. Pretty cool, but it doesn’t handle the full financial workflow on its own.

It’s often paired with payment processors or other providers to actually move money.

OpenPayd

Best for: Platforms handling cross-border payments, FX, or crypto-based flows.

OpenPayd provides BaaS, payments, and FX infrastructure through a single API. Platforms can create accounts, issue virtual IBANs (vIBANs), and move money across borders in multiple currencies.

It’s built for complex money movement, with a strong focus on fiat–crypto interoperability, including stablecoin on/off-ramps. But it’s infrastructure-first.

There’s no packaged product layer; platforms need to design the user experience, define pricing, and decide how they’ll monetize money flows. It’s also primarily focused on the UK and Europe.

Parafin

Best for: Marketplaces wanting to offer capital to sellers.

Parafin provides a fully packaged embedded finance product focused on lending and spend. Platforms can offer sellers working capital, branded cards, and pay-over-time options directly inside their product.

Underwriting, compliance, funding, and servicing are handled by Parafin. Unlike infrastructure providers, Parafin gives platforms the financial products as well as the operating layer (including pre-qualified offers, ongoing risk management, and a white-labelled UI).

Still, Parafin is tightly focused on financing and spend, not broader embedded finance.

Affirm

Best for: Platforms adding BNPL at checkout to increase conversion.

Affirm provides buy now, pay later (BNPL) and installment financing that platforms can embed directly into checkouts.

Customers can split purchases into fixed payments, while the platform gets paid upfront. For SaaS and marketplaces, Affirm is a conversion and AOV lever, not a financial layer. It’s designed to sit at checkout, giving customers more flexibility to pay; increasing sales and reducing drop-offs (especially on higher-priced offers).

Affirm handles underwriting, compliance, and funding, so platforms don’t take on lending risk or need to build anything themselves.

Choosing the right embedded finance provider/s

As you've learned from this list above, not all embedded finance platforms solve the same problem. Some give you infrastructure. Some give you products. Some give you both.

If you’re running a SaaS product or platform, embedded finance isn’t just a feature, it’s part of your business model.

The provider/s you choose affects how you onboard users, move money, and generate revenue.

Provider selection is really a question of strategic alignment. The infrastructure you pick today shapes what you can build tomorrow, so the partner's direction matters as much as their current feature set.

The best way to assess that: look at their recent product releases and who else they are serving.

- Lars Markull, Founder, Embedded Finance Review

Here are the criteria that actually matter.

API quality and developer experience

API quality is usually what determines how painful (or not) your integration is.

Infrastructure-first providers give you powerful APIs, but then you’re responsible for stitching everything together. Handling edge cases, retries, and failures yourself? It’s a lot.

Strong documentation, reliable webhooks, and good SDK support matter more than anything here. More managed platforms reduce that burden, if you’re happy to trade some flexibility for speed.

As payments expert Bill Noonan puts it, the biggest miss is confusing an easy API with a true partnership:

"Teams chase quick integration and early revenue, then get surprised when future margins, flexibility, and support are locked up by the wrong embedded finance partner.”

Compliance coverage and regulatory licensing

Financial services are regulated whether you like it or not, and every provider sits somewhere different on the spectrum.

Some handle KYC, AML, fraud, and licensing for you. Others push more of that responsibility onto your platform. The more your provider covers, the faster you can launch and the less you have to worry about on a day to day basis.

Global reach vs. domestic focus

Global can honestly mean different things depending on the provider. Some platforms offer real international coverage, with local payment methods, FX, and multi-currency support built in.

Others are effectively glorified domestic providers with limited expansion capability. If your users operate across borders, this is really key to pay attention to. Cross-border constraint cuts revenue quickly, especially if you monetize payouts and currency handling.

Revenue model and monetization

Not every embedded finance solution actually helps you make money. Some providers simply move funds and charge transaction or FX fees. Others enable monetization directly through lending, interchange, or embedded financial products.

Embedded finance is meant to drive revenue (not just enable payments), so this is one of the most important distinctions.

Time to launch and integration complexity

Speed vs. control shows up here. Infrastructure providers take longer to implement but give you full flexibility.

Managed platforms and packaged products get you live faster, but with predefined limits. There’s no right answer, really. It’s just about what fits your timeline and engineering resources.

Most SaaS platforms underestimate how much embedded finance can expand their monetization stack and ultimately their valuation, and instead optimize for the slickest API or fastest go-live, not the long term economics. – Bill Noonan, Founder 4Scale

Vendor lock-in and platform risk

Once you’ve onboarded users, issued accounts or cards, and built payment flows around a provider, switching isn’t just a technical change. It means migrating user balances, rebuilding flows, and potentially disrupting how your customers get paid.

The deeper the provider sits in your stack (ledgering, accounts, payouts), the harder it is to unwind later.

Most platforms rely on underlying banks, lenders, or processors behind the scenes. If one of those breaks, it impacts your product directly.

In 2024, the collapse of Synapse (a banking-as-a-service provider) left multiple fintech platforms unable to access or move user funds. Yikes.

Embedded finance on Whop

Building on Whop means you get access to embedded finance tools and products without needing to assemble them solo.

Whop connects platforms, SaaS, and marketplaces with multiple embedded finance providers behind the scenes, so you can accept payments, route transactions, offer financing options like BNPL, and complete global payouts in fiat and crypto right out of the box.

Beyond embedded payments and lending, Whop also acts as the Merchant of Record (MoR) handling billing, subscriptions, tax, and compliance, alongside built-in monetization tools like affiliates and marketplace distribution.

Faster time to launch, built-in monetization, and less operational overhead. That's why platforms choose Whop for embedded finance.

Embedded finance FAQs

What is embedded finance?

Embedded finance is the integration of financial services such as payments, banking accounts, loans, and insurance directly into non-financial platforms and apps.

Rather than redirecting users, the platform delivers financial products inside its own interface, powered by APIs from specialist providers called BaaS (Banking-as-a-Service) platforms.

What is the difference between embedded finance and BaaS?

Embedded finance refers to the end result: financial services built into a non-financial product. Banking-as-a-Service (BaaS) is the underlying infrastructure that makes it possible. BaaS providers supply the APIs, banking licences, and compliance frameworks that platforms use to build those embedded services.

TL;DR: BaaS is the engine; embedded finance is what the customer experiences.

What are the main types of embedded finance?

The five main types of embedded finance are embedded payments, embedded banking, embedded lending, embedded insurance, and embedded investing. Each work to allow platforms and marketplaces to monetize the flow of money.

How do platforms make money from embedded finance?

Platforms earn revenue through several embedded finance streams: interchange fees when users spend on a platform-issued debit card; interest margin on funds held in embedded accounts; loan origination or facilitation fees from embedded lending products; transaction take-rates from payment processing; and subscription fees for premium financial tools.

What are the risks of embedded finance for platforms?

The main risks include regulatory compliance complexity, vendor lock-in, banking partner risk, data security obligations, and fraud risk. The best providers help navigate and handle complex regulatory processes for you.

What is the difference between embedded payments and embedded finance?

Embedded payments is a subset of embedded finance, specifically, the integration of payment processing (checkout, card acceptance, payouts) into a non-financial platform.

Embedded finance also covers financial services such as banking, lending, insurance, and investing. Most platforms start with embedded payments and expand to the full financial stack as they scale.